Investment Thesis

CASI Pharmaceuticals (Casi) (NASDAQ:CASI) is currently rated a “strong buy” by analysts who have set a consensus price target of $3.5. The stock currently trades at $1.67 after shedding 49% of its value since mid-January. Casi’s share price has been volatile in the past (a good sign), but the current price represents a near 2-year low.

Casi Pharmaceuticals 1-year share price performance. Source: TradingView

Casi Pharmaceuticals 1-year share price performance. Source: TradingView

I believe Casi represents an interesting investment proposition. The promise of its portfolio (which focuses on some of the more innovative and breakthrough aspects of oncological treatment) and proven ability to commercialise a treatment in its target market of China add up to more than <$2 per share, in my view. The stock’s volatility also suggests the price will rise again.

There is not much precedent to go on since this is a rare type of business, but I would back Casi to make further progress towards its goals (despite severe COVID-19 disruption) in 2020, and whilst I don’t expect this to be a transformative year for the company (since most of its clinical trials are at an early stage) I don’t see sufficient long-term headwinds to justify the current discounted share price.

Company Overview

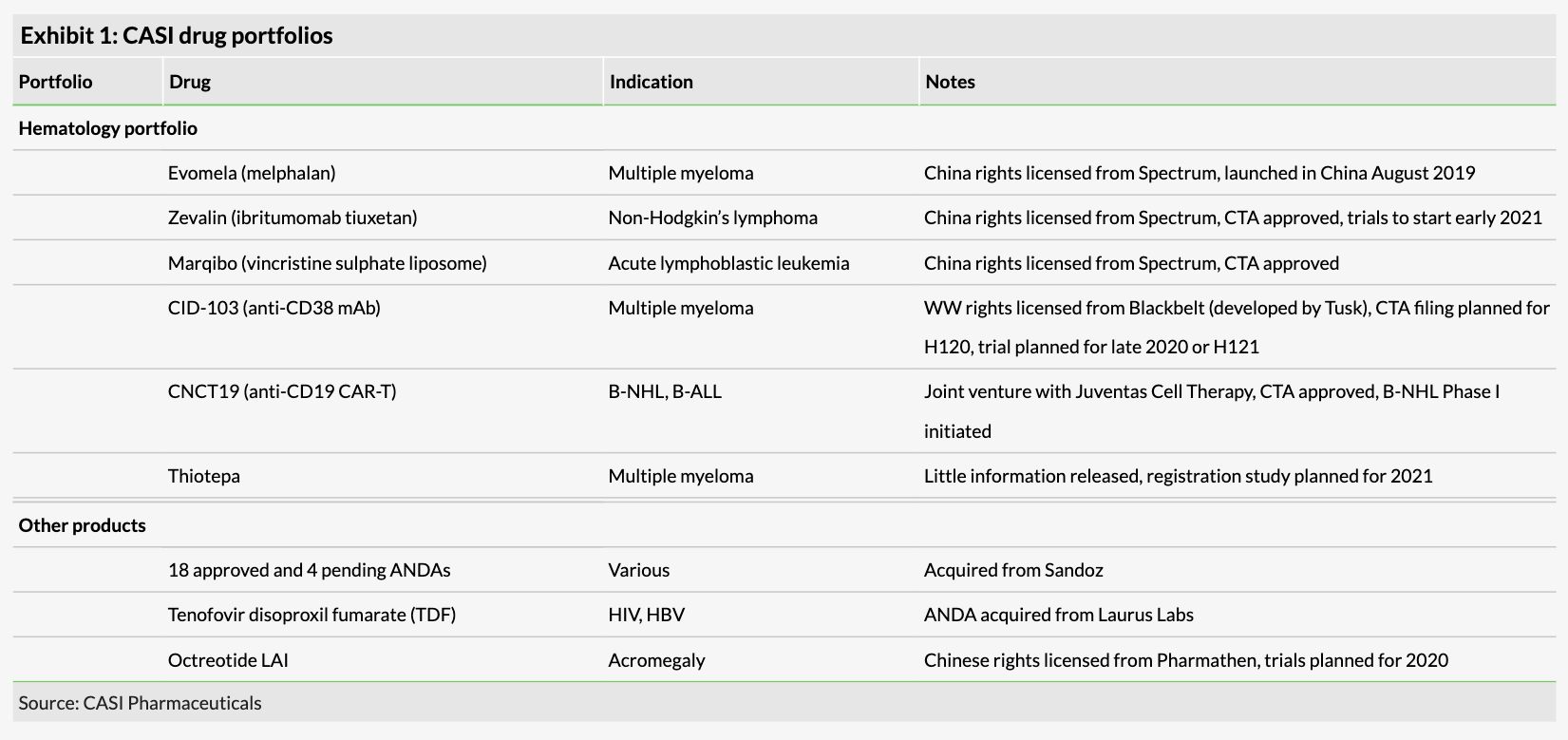

Casi Pharmaceuticals has an unusual business model, being a NASDAQ listed company acquiring licenses in the US, China and globally for approved or promising hematology/oncology treatments for the Chinese market, from a global network of early stage biotech firms including Spectrum Pharmaceuticals (NASDAQ:SPPI), and big pharma Sandoz – from whom the company purchased 25 FDA-approved abbreviated new drug applications (“ANDA”s) in an $18m deal in January 2018.

Casi current treatment portfolio. Source: Edison Group Casi Pharmaceuticals research note.

Casi current treatment portfolio. Source: Edison Group Casi Pharmaceuticals research note.

Casi’s innovative strategy has several advantages. Acquiring assets that have already been approved and/or commercialised in other markets – usually the US – gives Casi confidence that its drugs have the required efficacy and safety profile to pass clinical trials in markets such as China, theoretically enabling a quicker overall path to approval, and commercial sales.

There is estimated to be a high unmet need in China for the types of advanced-stage treatments that Casi is working on and recent reforms within the Chinese healthcare market are said to have opened the country up to increased international collaboration – however, the current market is small, with the US exporting just $2bn worth of drugs to China in 2015, according to a detailed Edison Research note on Casi that I would highly recommend to readers.

China is, however, slowly becoming more open to fast-tracking innovative drugs, hence Casi’s acquisitive strategy that hopes to match areas of high unmet need and commercial opportunity with effective and, in many cases, already approved drugs, the company explains in its recent investor presentation.

Casi enjoyed a productive 2019, progressing its portfolio by securing approval for and commercialising EVOMELA – a conditioning treatment for multiple myeloma directed stem cell therapy which earned $4.1m of revenues in Q419, as well as acquiring the worldwide rights to CD19 CAR-T therapy treatment CNCT-19, anti-CD38 monoclonal antibody CID-103, and China rights to Octreotide – indicated for neuroendocrine tumors and acromegaly.

Recent Execution in Hematology/Oncology Portfolio. Source: company investor presentation.

Recent Execution in Hematology/Oncology Portfolio. Source: company investor presentation.

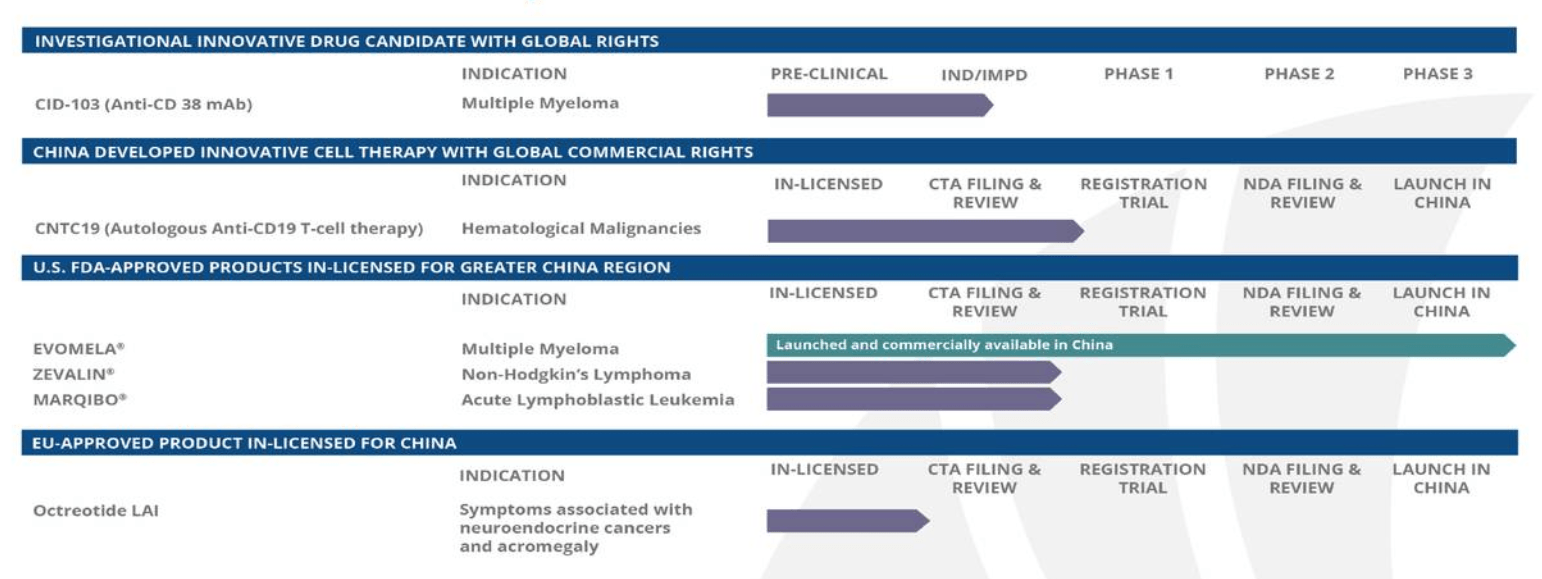

Despite the fast-track processes put in place by the Chinese authorities, EVOMELA aside, Casi’s remaining assets are still some way from approval, however, as we can see from the company’s clinical trial schedule below.

Casi product and pipeline. Source: company investor presentation.

Casi product and pipeline. Source: company investor presentation.

Casi is in the process of designing a planned state-of-the-art manufacturing facility and has completed a land use acquisition for ~17.6 acres of land in the well-connected biotech hub of Wuxi, China. This venture is likely to be a drain on the company’s financial resources, which stood at $54m at the end of 2019, and which the company estimates will last until March 2021.

This makes the possibility of the company seeking further funding from the market likely – Casi has shelf funding arrangements in place with brokerages HC Wainwright and Jefferies. Given the current depressed share price, however, the company is likely to bide its time and wait for expected positive news flow from the 4 clinical trials it has scheduled for 2020 (or better-than-expected EVOMELA sales data) to lift the stock out of its current slump before offering any shares to the market.

Spectrum Portfolio

In 2014, Casi acquired the Chinese rights to 3 drugs – EVOMELA, Zevalin, and Marqibo – commercialised and sold in the US by Spectrum Pharmaceuticals in exchange for 17% of its stock and a $1.5m promissory note. The assets have since been acquired by Acrotech Biopharma which has assumed the supply arrangements.

EVOMELA

In August last year, Casi won approval in China for EVOMELA (Melphalan for Injection) – a conditioning treatment used prior to stem cell transplant in the multiple myeloma setting, which delivered $4.1m of sales in Q419. Whilst sales are likely to suffer this year owing to disruption caused in the Chinese pharmaceutical markets by COVID-19, a year-on-year increase is expected – the drug earned $35.2m of revenues in the US for Spectrum in 2017.

Unlike rival treatments, the EVOMELA formulation of melphalan avoids the use of propylene glycol, normally used as a co-solvent, instead employing the Captisol technology developed by Ligand Pharmaceuticals (LGND) (see my research note on Ligand here) which allows for greater stability and hence longer preparation and infusion times.

EVOMELA is approved in the US for conditioning treatment ahead of hematopoietic stem cell transplantation for multiple myeloma, having improved partial response or better rates in a 61-person clinical trial which took place in 2016 from 79% to 95% after transplant, with a safety profile comparable to other high-dose melphalan treatments.

EVOMELA is currently the only approved melphalan treatment in China and looks to have a promising future; however, it’s anticipated that complex surgery such as stem cell therapy may be delayed or postponed in China in light of the coronavirus. As such, Edison is forecasting sales of just $7.8m for the drug in 2020. It will be interesting to see the Q120 sales figures which will be released within the next couple of weeks.

The second of the three Spectrum treatments, Zevalin, is an antibody targeting CD20 (the same B-cell expressed protein targeted by Roche’s multi-billion selling Rituximab) indicated to treat follicular non-Hodgkin Lymphoma (“NHL”). Zevalin has been available in the US since 2002, having achieved a complete response rate of 38% in a combination trial alongside Rituxan (Rituximab) vs. the 18% achieved by Rituxan as a mono-therapy.

Casi management says it has received approval from the National Medical Products Administration (“NMPA”) for its Clinical Trial Application (“CTA”) for a confirmatory registrational trial to evaluate efficacy and safety and intends to push for the import drug registration and market approval for Zevalin as swiftly as possible. Spectrum earned $11m from sales of Zevalin in 2017, Edison reports, estimating the drug costs $66,000 per treatment.

Finally, although Mariqbo, the third Spectrum drug – approved by the FDA for the treatment of adult patients with Philadelphia chromosome-negative (Ph-) acute lymphoblastic leukemia (“ALL”) – has also received NMPA approval for its clinical trial application, Casi has decided to shelve development plans for the time being, it seems, owing to the rare and niche indication for the product.

CNCT-19 – addressing a high unmet need with CAR-T

The anti-CD19 CAR-T therapy CNCT-19 is in-licensed by Casi from China-based Juventas Cell Therapy, with Juventas handling the bulk of the development process (although Casi owns 80% of the Joint Venture created having invested $116m into Juventas in June 2019) in exchange for future milestone payments and royalties, with Casi responsible for commercialisation. Wei-Wu He, who was appointed CEO of Casi in April 2019, is also Chairman and founder of Juventas.

Juventas has already had 2 Initial New Drug (“IND”) applications accepted by NMPA for non-Hodgkin Lymphoma and acute lymphoblastic leukemia (“ALL”) and phase 1 trials are expected to begin imminently. CD-19 targeting CAR therapies have demonstrated statistically significant antitumor efficacy in children and adults suffering from relapsed B-cell ALL, NHL and chronic lymphocytic leukemia (“CLL”).

CAR-T therapy is an increasingly prominent treatment option for cancer patients but the process is still slow and requires intensive manufacturing and supply chains. DC19 is the most regularly used biomarker in CAR-T cell therapy trials for hematological malignancies, Casi management says, with some treatments already approved.

The prospect of CNCT-19 securing approval in 2019 seems fanciful, and indeed there is no guarantee that the trials will ever be successful (the odds are against it) but should it happen, Casi’s treatment would address an area of high unmet need globally, handing the company a significant first-mover advantage.

CID-103 – anti-CD38 monoclonal antibody for myeloma

CID-103 was also in-licensed from a Chinese biotech firm, Black Belt Therapeutics Limited which had been formed as a spin-off after Roche (OTCQX:RHHBY) completed a merger with Tusk Therapeutics in 2018.

Blackbelt completed initial studies of CID-103, – an anti-CD38 monoclonal antibody – and pre-clinical data has showed CID-103 to have enhanced activity across numerous malignancy types coupled with a superior safety profile when compared with rival CD-38 treatments, Casi management says.

CD38 is expressed by cancerous B-cells which are present in myeloma, and an anti-CD38 antibody – Janssen’s Darzalex – has been approved in the US, having been shown to increase Progression Free Survival (“PFS”) rates alongside a regimen of lenalidomide and dexamethasone, making sales of >$2bn, although the drug has been dogged by concerns about its tolerability profile.

Casi points to data that suggests CID-103’s safety and efficacy profile is superior to Darzalex, demonstrating superior antibody dependent cellular cytotoxicity (“ADCC”) and complement‐dependent cytotoxicity (“CDC”) when compared to Darzalex and other anti-CD38 mAbs.

Still, there is a long way to go before CID-103 can potentially compete for real-world sales – the drug is currently at the submission stage of its IND application, and phase 1 studies are slated to begin sometime in the first half of this year. Doubtless, we will learn more on the company’s next earnings call.

Wildcards Thiotepa, Octreotide and the ANDA Portfolio

Thiotepa, a chemotherapy agent, is another Casi licensing deal that little is currently known about other than that, like EVOMELA, Thiotepa can be used as a conditioning agent ahead of stem-cell therapy, and, according to Casi management, has a long history of established use within the hematology/oncology setting. The clinical program for Thiotepa is expected to begin in earnest this year.

Octreotide – a synthetic form of the hormone somatostatin that is used to treat acromegaly and symptoms associated with certain neuroendocrine tumors, has been in-licensed from another Chinese biotech – Pharmathen Global – in exchange for a $1m upfront payment and $2m of potential milestone payments. In its research note, Edison compares Octreotide to Novartis’ Sandostatin Long Acting Release which earned the company $1.6bn in sales in 2018.

And finally there is the ANDA portfolio acquired from Sandoz. From 25 FDA approved assets, one tentatively approved and 3 pending approval assets were later added before 7 were delisted by Casi. The company believes that recent reforms to the Chinese government’s drug pricing policies will result in broader demand for some of its ANDA assets, and is likely to take its time assessing which represents the best opportunity in terms of speed-of-approval and size of unmet need.

Conclusion

Diversified portfolio and large addressable market help to hedge significant risk created by trial/sales uncertainty + financial concerns

Having reviewed the portfolio, I draw the conclusion that Casi is an intriguing investment case at its current price of $1.66.

I began this piece with a look at the company’s 1-year stock price performance, which has recently been profoundly (negatively) affected by COVID-19. A company whose interests are focused on advanced stage hematological/oncological treatments that are expensive and may raise reimbursement concerns is bound to suffer in the wake of a public health crisis in China that will require time to reset before the drug approval process can return to its faster pace of innovation.

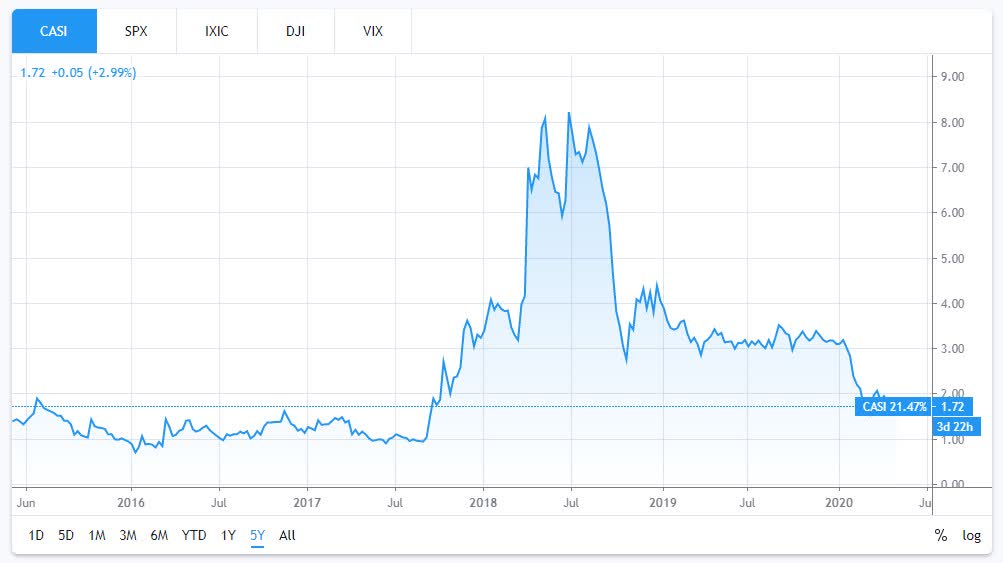

If that helps to explain the low price today, then a glance at the five-year chart helps to illustrate that Casi stock is also capable of sudden volatility (and sudden price gains) when company news-flow (e.g. data readouts, news on trial statuses, new portfolio assets, etc.) is regular and as assets inch their way towards approval for commercialisation.

Casi Pharmaceuticals 5-year share price performance. Source: TradingView

Casi Pharmaceuticals 5-year share price performance. Source: TradingView

Hence, given we know Casi plans to initiate 4 clinical trials in 2020 as well as implement a first full-year sales cycle for EVOMELA and is looking at a host of other opportunities – from chemotherapy to stem-cell therapy – I believe there is sufficient reason to believe Casi’s stock can break out of its current slump.

It may not do so in the near term, given the uncertainty around coronavirus, coupled with the market’s concerns over further fundraising efforts with the company running a little low on cash (Casi’s liabilities are just $9m but costs and expenses exceeded $51m in 2019).

I think a sensible strategy to pursue here may be to acquire some Casi stock now, since there is plenty of downside protection in place (price is at 2-year lows, business model is strong enough to weather the current crisis over the long term, funding is adequate), and plenty of short-term price catalysts (such as the initiation of new clinical trials, evaluation of trial data, and acquisition of further drug candidates) to keep investors hopeful and on the look-out for good news.

Investors should only consider an investment in Casi Pharmaceuticals if their appetite for risk is high since the chances of the company suffering setbacks owing to size, funding, or regulatory matters outside of its control are considerable.

In my view, Casi offers an attractive entry point at $1.7 that we may not see again for some time, and I believe the company has mitigated its risk intelligently by acquiring candidates with strong efficacy profiles, many of which have already secured approval. It is a differentiated yet seemingly well-managed strategy that slightly tips the balance in favour of the company, for me.

Gain access to all of the market research and financial analytics used in the preparation of this article plus exclusive content and pharma, healthcare and biotech investment recommendations and research/analytics by subscribing to my channel, Haggerston BioHealth.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in CASI over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}