Kindly sponsored by Aberdeen Standard Investments

Performance data

June’s biggest movers in price terms are shown in the chart below.

In a month when Boris Johnson announced the easing of restrictions would be pushed back as COVID cases rose, only a handful of property companies saw share price gains. Topping the list was Residential Secure Income, which owns a portfolio of affordable housing, after it reported strong half-year results at the back end of May. Berlin residential landlord Phoenix Spree Deutschland continued its mini share price resurgence following the throwing out of rent controls in the German capital city. It’s share price has risen more than 25% in the year-to-date, but it was still trading at a 13% discount to net asset value (NAV) at the end of June.

After reporting a big uplift in its portfolio valuation and NAV, German business parks owner and operator Sirius Real Estate saw its share price rise 9.3%. Generalist real estate investment trusts (REITs) continued their share price recovery from the depths of the pandemic, with Standard Life Investments Property Income Trust and Schroder REIT making the top 10 best performing property companies in June. Both have seen share price gains in 2021 of 16.7% and 25.1% respectively.

The announcement that the last step in the easing of restrictions in the UK was being pushed back from June to July resulted in share price falls for many of the retail and leisure property landlords. Secondary mall owner Capital & Regional headed the list of worst share price performers in June with a 14.8% fall. NewRiver REIT, which owns shopping centres and retail parks, as well as a pub portfolio, also saw a double-digit share price fall in June, but is positive in the year-to-date as it embarks on a renewed strategy. Hammerson, the shopping centre giant, saw its share price come off 6.8% on the restrictions announcement. However, its share price is up nearly 50% in 2021 so far.

West End of London landlords Shaftesbury and Capital & Counties also suffered a slight drop in their share price in June, but again, both are up in 2021 as they gear up for a full reopening of retail and leisure assets. The share price of central London flexible office provider Workspace was down 7.9% after reporting large valuation falls in full year results. Cuban real estate company CEIBA Investments rounds off the list, with its share price falling 16.6% so far this year.

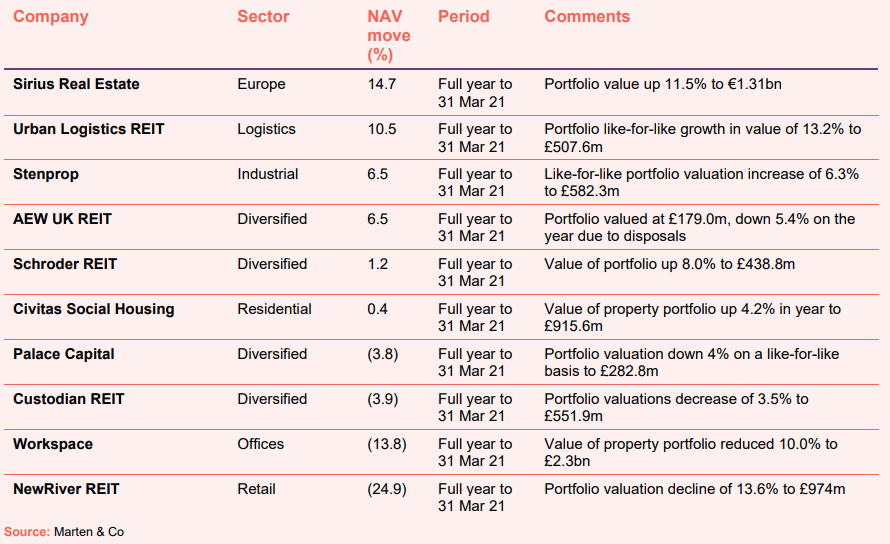

Valuation moves

Corporate activity

The UK Residential REIT announced its intention to float on the London Stock Exchange with the aim of raising £150m to be invested in a portfolio of privately rented residential assets. It is targeting a dividend yield of 5.5% per year once fully invested and a net total shareholder return of 10% per year.

Blackstone upped its offer for property company St Modwen to 560p per share (from 542p in May 2021), valuing the company at £1.272bn. The final offer has been recommended by the board and represents a 21.1% premium to its EPRA net tangible asset (NTA) value.

LXI REIT raised £104m through an oversubscribed placing. The proceeds will be used to acquire a pipeline of assets including potential sale-and-leaseback deals and forward funding opportunities.

Big Yellow Group raised £100m from a placing of new ordinary shares. The proceeds will fund two strategic acquisitions, which along with its existing development pipeline, has the potential to generate more than £40m of net operating income over the short to medium term.

Urban Logistics REIT announced intentions to raise £108m through the placing of new ordinary shares. The proceeds will be used to acquire a pipeline of assets with an average net initial yield of 6.1%.

Sirius Real Estate raised €400m through the placing of corporate bonds. The senior bonds have a five-year term with a coupon of 1.125%. Net proceeds are to be used to refinance existing debt, with the remainder deployed on potential acquisitions.

Impact Healthcare REIT signed a new revolving credit facility of £26m with National Westminster Bank, with an accordion agreement to increase this facility to £50m. The new facility is for an initial term of three years with an option to extend for up to a further two years. The margin is 190 basis points per annum over SONIA, which is currently equivalent to a total drawn cost of debt of 1.95% per annum.

Town Centre Securities launched a £5m share buy-back programme in a bid to address its wide discount to NAV.

Major news stories

Tritax EuroBox acquired a logistics asset in the Port of Gothenburg, Sweden – its first in the Nordics – for SEK474m (€47m), reflecting a 3.6% net initial yield.

Home REIT bought a further 14 portfolios of properties, totalling 314 beds, located across England for £47.1m. Following the deal, it has invested all of its IPO proceeds plus over 40% of its £120m 12-year debt facility.

- Unite sells London student digs to JV

Unite Group sold two student accommodation assets in London to its 50:50 joint venture with GIC (London Student Accommodation joint venture) for £342m.

Grainger acquired The Forge, a build-to-rent residential asset comprising 283 rental apartments in Newcastle, for £57m.

Target Healthcare REIT acquired a care home in Scotland and forward funded a pre-let development in Buckinghamshire for a total of £33m.

Empiric Student Property sold a non-core asset in Exeter for £11.05m (ahead of the December 2020 book value), in line with the group’s strategy to dispose of around £100m of non-core assets over the short to medium term.

LXI REIT forward funded the acquisition of a 94,000 sq ft garden centre in Reading for £19m, reflecting a 5.3% net initial yield. The property is pre-let to Dobbies on a new 35-year lease, with CPI +1% per annum rental uplifts.

After successfully suing two tenants that had refused to pay rent during the coronavirus pandemic, AEW UK REIT received all unpaid rent due to it amounting to just over £1.2m.

AEW UK REIT acquired a five-unit retail site in Bristol for £10.2m, reflecting a net initial yield of 8%.

Standard Life Investments Property Income Trust sold an industrial asset in Kettering for £9.05m, in line with its strategy of selling industrial assets that are not suitable for logistics.

QuotedData views

Managers’ views

A collation of recent insights on real estate sectors taken from the comments made by chairmen and investment managers of real estate companies – have a read and make your own minds up. Please remember that nothing in this note is designed to encourage you to buy or sell any of the companies mentioned.

Residential

Paul Bridge, chief executive:

As the vaccine roll-out continues and a greater degree of normality returns what is clear is the ongoing need for a significant increase in the supply of all forms of social housing. It is clear that the government recognises the vital role that both the public and private sector can play in meeting the country’s housing need and in particular in the provision of housing with care.

The evidence is overwhelming that housing the most vulnerable individuals in our society in proper homes in the community is of paramount importance and not only transforms people’s lives but also is more cost-effective for the public purse.

Civitas sees compelling opportunities to invest further in this sector. A substantial pipeline of over £200m has been developed with long standing and trusted counterparties and a good start made on deploying recently acquired debt facility. The pipeline leaves open the prospect of future equity raises subject to market conditions and investors’ views.

Diversified

Mark Burton, chairman:

The lockdown period at the start of 2021 has reversed some of the UK’s economic recovery seen in the second half of 2020. However, the general economic outlook is brighter for the second half of 2021, following the effective rollout of the vaccination programme and further easing of lockdown restrictions. We expect this to be reflected in the real estate market in terms of improved rent collection levels and the recovery of rental values and property valuations. However, many tenants will have benefitted from a range of government support schemes over the past year. As these protective measures are removed, we may yet see a significant surge in the number of corporate insolvencies, and so an element of caution should be retained. The pandemic has accelerated certain structural shifts in the real estate market. We expect that this will present new challenges and opportunities in certain sectors.

Richard Shepherd-Cross, investment manager:

In ordinary times rent collection and asset management are rightly taken for granted by shareholders but the importance of the close relationships between manager and tenant and the manager’s ability to influence the outcome of negotiations has come to the fore this year. From the outside, it may appear that property fund managers have spent the year chasing rent collection and worrying about the pandemic. From our perspective we are largely experiencing business as usual, managing landlord/tenant relationships and engaging in normal levels of activity in terms of new lettings, extending existing leases, acquiring new assets and selling assets that we do not believe will perform over the medium to long-term.

The important consideration for the outlook for commercial property is occupier demand. If commercial property remains in use by occupiers, then it has a bright future. Occupier demand in the industrial and logistics sector is very strong and forecast to remain so, which is supporting rental growth. We are seeing demand from occupiers on retail parks and in prime town centres but on rebased rents. Offices are likely to continue to be an essential feature of most businesses and we are seeing occupiers look beyond the pandemic to secure appropriate space.

Nick Montgomery, fund manager:

The impact of the pandemic has been polarised across the real estate sectors, with an average capital value decline of -2.5% for the MSCI Benchmark over the year to March 2021 masking a historically high divergence between the three main sectors of offices, industrial and retail. This is illustrated by the best performing subsector, south east industrial, enjoying a capital value increase of 10.9%, compared with shopping centres as the worst sub-sector which experienced a -9.8% capital value decline. Whilst polarisation in performance is expected to continue, the divergence is likely to narrow and capital values are starting to recover. By the end of September 2020, overall UK commercial real estate had seen negative capital growth for 23 consecutive months. Since then, the market has seen positive capital growth for seven consecutive months. By the end of April 2021 (the latest available data point) the rolling three-month capital growth of 1.5% was the highest the market had seen since February 2018. All three main sectors of offices, industrial and retail delivered a positive total return during the quarter to March 2021.

Whilst unprecedented government and central bank policy support has kept interest rates low and supported real estate values and asset prices more generally, government intervention has enabled tenants to withhold rental payments and diluted income returns. This has been accompanied by corporate insolvency measures enabling tenants to restructure landlord liabilities. The retail and leisure sectors have been most adversely impacted by the pandemic. It is important that as measures to protect tenants are lifted, any proposals relating to the treatment of historic arrears fairly treats the interests of both landlords and tenants.

Assuming the successful completion of the vaccine rollout programme and a reopening of the economy, UK GDP should return to its pre-virus level in the second half of 2022. The main driver will be consumer spending, with consumers accumulating an extra £150bn in savings during lockdown. In addition, 2021 should see a recovery in business investment and the chancellor has postponed tax rises until 2022. The rebound in energy and food prices means that inflation is likely to accelerate to 2.5% in the next few months, before easing to 1.5% next year. Higher unemployment as the furlough scheme ends should limit inflationary pressures, with base rates remaining at 0.1% until the end of 2022.

The pandemic response will change government policy in a number of areas, notably with greater emphasis on ‘levelling up’, which came to prominence after the 2019 general election. In its broadest terms, levelling up is a commitment to address regional inequalities with a focus on visible infrastructure projects such as road-building and high-street regeneration. Whilst this will benefit poorer areas of the UK, the £4.8bn fund will also be targeted at higher multiplier industries which is likely to benefit stronger regional cities such as Manchester and Leeds.

Industrial

Paul Arenson, chief executive:

Notwithstanding COVID-19 and the three UK lockdowns, the structural imbalance in supply and demand for UK multi-let industrial continued to deliver inflation-beating rental growth throughout the year. We hold the view that this imbalance will continue for several years, as it is still not economically feasible to build multi-let industrial units in most locations at current rental levels and yields, and because in and around many conurbations, supply is also being taken out of the market in favour of other uses such as residential. We estimate that replacement build costs are at least £125 per sq ft, which means rents must rise by a further 30-40% in most regions before development of new multi-let industrial units becomes widely viable, assuming suitable development land is available in and around densely populated towns and cities.

On the demand side, we are seeing increasing numbers of new types of businesses, enabled by the internet, needing multi-let industrial space. These are businesses who have not previously occupied multi-let industrial space and are now realising the value of affordable, flexible space close to towns and cities. Whilst COVID-19 has caused immense disruption to the economy, we can see that the response to it by business is paving the way for greater demand for multi-let industrial units. The internet sales and distribution channels for all businesses have taken another big step forward as the population was forced into isolation and had no choice but to embrace new technology, as well as supply and distribution channels. Home working and the explosion of communication technologies have fostered greater ability to work in a decentralised way, further fuelling demand for multi-let industrial space.

Companies have reassessed their globalised ‘just-in-time’ supply chains. It is becoming apparent to many businesses that it is not viable to rely solely on geographically distant supply chains from single undiversified sources. We sense an increasing desire from companies to have greater control over supplies and easier access, even if it means more cost. Similarly, retailers have expanded into online trading through websites, and many restaurants have opted for dark kitchens to facilitate the rapid increase in demand for delivered meals. There has also been a significant increase in demand from new businesses benefiting from COVID-19 seeking multi-let industrial space, such as those that are part of the PPE supply chain and those operating in entirely new industries like 3D printing. We believe that this type of strategic switching of business models will continue to drive the structural shift in demand for multi-let industrial units.

Logistics

Richard Moffitt, chief executive:

The logistics market remains in focus with property investors and logistics operators due to its outperformance and the forecast for the next few years suggests that this positive trend will continue. The UK continues to be one of the fastest-growing adopters of online retail sales and there is a requirement for all tenants to develop their e-fulfilment capability accordingly. As such, key geographic regions across the UK are seeing buoyant leasing activity with a record level of warehouse space under offer at the end of March 2021.

Behavioural changes formed during the pandemic will have a lasting effect. The unstoppable growth of e-commerce concentrated five years of growth into just a few months. Similarly, online penetration for food stores remains above 10% according to ONS, almost doubling the pre-pandemic share and steering investment from all UK supermarkets to improving their online channels.

Retail

Allan Lockhart, chief executive:

The macroeconomic environment is improving; in May the Bank of England upgraded its 2021 growth outlook for the UK economy from 5% to 7.25%, driven by an anticipated sharp rise in consumer spending. Consumer confidence in the UK economy has returned to pre-pandemic levels and we are well placed to benefit from consumers’ growing preference for shopping locally and supporting community assets.

In terms of the investment market, liquidity in retail parks improved during the year and investor demand for regeneration projects also increased over the second half of FY21, especially for assets located in areas with attractive underlying residential values. We are starting to see early signs of an uplift in shopping centre liquidity and we expect the investment market to improve further as we emerge from the COVID-19 crisis.

Real estate research notes

Tritax EuroBox – Full throttle

Civitas Social Housing – On firm footing

Standard Life Investments Property Income Trust – Focus on tomorrow’s world

Grit Real Estate – On the pathway to recovery

Legal

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority). This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access. No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.

-75x75.jpg)

{kind=link}