Celebrations may be in order for La Jolla Pharmaceutical Company (NASDAQ:LJPC) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with the analysts modelling a real improvement in business performance. The market may be pricing in some blue sky too, with the share price gaining 30% to US$5.35 in the last 7 days. Could this upgrade be enough to drive the stock even higher?

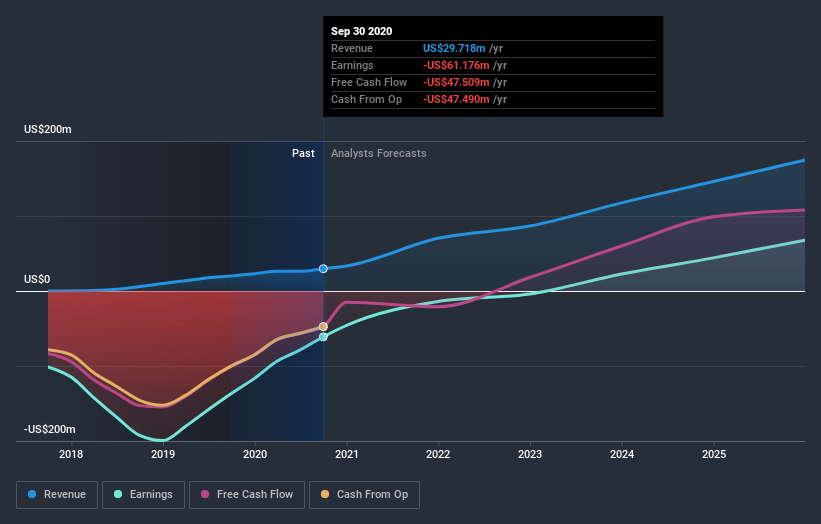

After the upgrade, the two analysts covering La Jolla Pharmaceutical are now predicting revenues of US$70m in 2021. If met, this would reflect a substantial 136% improvement in sales compared to the last 12 months. Losses are predicted to fall substantially, shrinking 72% to US$0.63. However, before this estimates update, the consensus had been expecting revenues of US$60m and US$0.81 per share in losses. So there’s been quite a change-up of views after the recent consensus updates, with the analysts making a sizeable increase to their revenue forecasts while also reducing the estimated loss as the business grows towards breakeven.

Despite these upgrades, the analysts have not made any major changes to their price target of US$10.92, implying that their latest estimates don’t have a long term impact on what they think the stock is worth. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values La Jolla Pharmaceutical at US$20.00 per share, while the most bearish prices it at US$4.75. With such a wide range in price targets, the analysts are almost certainly betting on widely diverse outcomes for the underlying business. With this in mind, we wouldn’t rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. The analysts are definitely expecting La Jolla Pharmaceutical’s growth to accelerate, with the forecast 136% growth ranking favourably alongside historical growth of 66% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 20% next year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect La Jolla Pharmaceutical to grow faster than the wider industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses next year, perhaps suggesting La Jolla Pharmaceutical is moving incrementally towards profitability. They also upgraded their revenue estimates for next year, and sales are expected to grow faster than the wider market. Some investors might be disappointed to see that the price target is unchanged, but we feel that improving fundamentals are usually a positive – assuming these forecasts are met! So La Jolla Pharmaceutical could be a good candidate for more research.

It’s great to see the analysts upgrading their estimates, but the biggest highlight to us is that the business is expected to become profitable in the foreseeable future. You can learn more about these forecasts, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}