Thesis

Farfetch (NYSE:FTCH) is a curated, luxury-only global platform that connects roughly 2m consumers with over 1,300 brands and boutiques. Described as the “Amazon of luxury fashion” during its IPO, the company fell out of favor following disappointing 2Q19 earnings, compounded by its misunderstood acquisition of New Guards, a transaction that expanded the company’s capital-light, platform model into private label. Farfetch holds a significant first-mover advantage as the only scaled, luxury platform, and is benefiting from powerful network effects that will help it capture and maintain significant market share and operating profitability as it accelerates the luxury industry’s shift online. It is well placed to take advantage of the strong growth in online luxury which is expected to grow from 12% of industry revenues in 2019 to 32% in 2028. Farfetch’s market share should expand from ~5% to nearly 10%.

Company Overview

Farfetch is the world’s largest third-party marketplace for luxury personal goods. The company was founded in 2007 by José Neves and went public in September 2018, raising $1bn at a price of $20.

Source: Company Filings

Farfetch is a global platform, generating 37% of revenue from EMEA, 36% from Asia-Pacific and 27% from the Americas. Within Asia-Pacific, China is the largest geography. The Middle East is Farfetch’s fastest growing region and it is not unreasonable to expect Asia-Pacific to become a much larger component of its geographic mix now that Farfetch’s online flagship store has become active on JD.com. In 2019 Farfetch purchased JD.com’s (JD) TopLife luxury goods sales platform for $50m and agreed to pay JD.com a share of every transaction. Farfetch officially launched the flagship store in June 2019.

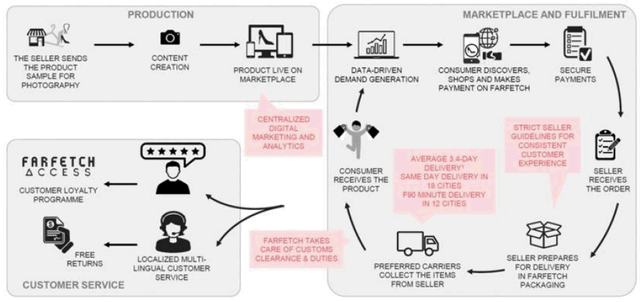

Product

Farfetch operates a marketplace with three types of sellers including boutiques, large brands selling D2C and Farfetch selling goods. There are 450+ brands selling directly to their customers on Farfetch and over 3,200 brands on the platform including those sold by boutiques. For boutiques, Farfetch provides a very compelling value proposition, offering a cutting-edge digital storefront with global reach, backed by a comprehensive suite of inventory management, catalog creation, logistics/fulfillment, payments processing and advantageous shipping rates.

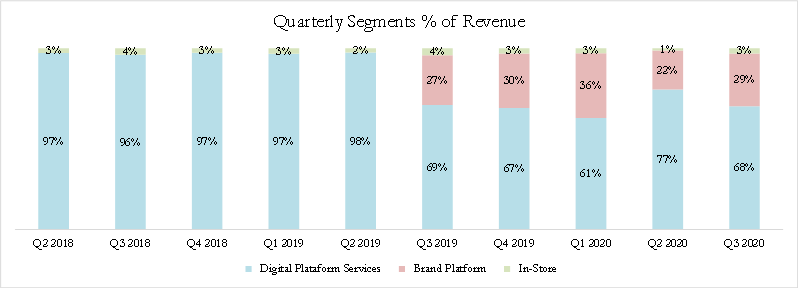

In Q3 2019, the company started reporting revenues from the brand platform as a separate segment, it is gradually expanding as a percentage of total revenues. This segment represents recurring, subscription revenues, much in the same way Shopify (SHOP) provides an eCommerce platform for merchants. This is the most exciting aspect of Farfetch’s business and what investors should watch closely given how SaaS platform businesses command significantly greater revenue multiples vs. pure-play online retailers.

Source: Company accounts, author’s calculations

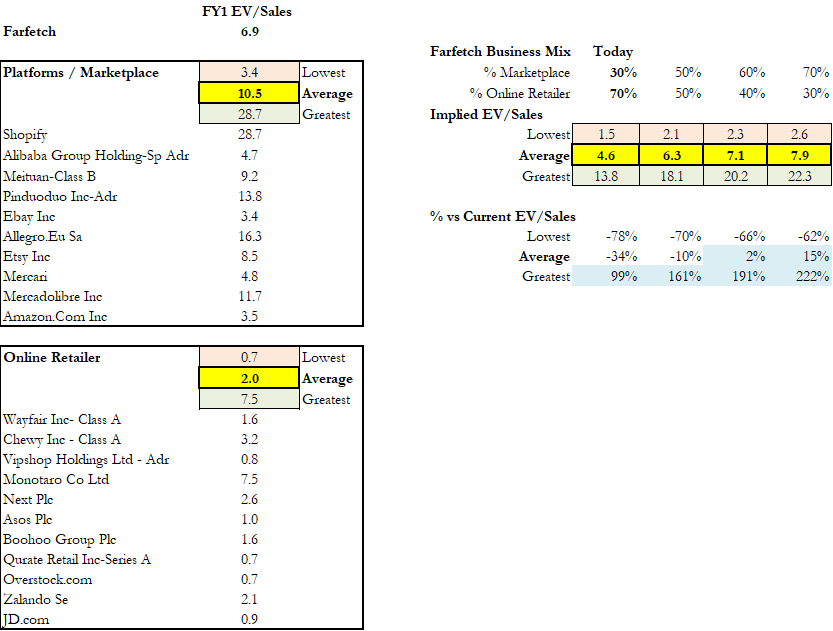

The following tables highlight the FY1 EV/Sales multiples observed on platform/marketplace companies vs. those of pure-play online retailers. We also highlight how Farfetch could be valued as it expands the percentage of Marketplace revenue it earns – these calculations indicate the market expects Farfetch to transition towards 60/40 mix of Marketplace/Online revenues assuming the comps below: Source: Bloomberg estimates, author’s calculations

Source: Bloomberg estimates, author’s calculations

Growth Potential and Competition

According to research by Kemp Little, aggregator platforms like Farfetch will continue to dominate online luxury. The Pandemic has served to accelerate for this trend as customers who would otherwise have not made an online purchase were forced to – many of them will keep buying online. Analysis covering Farfetch expects revenue of $1.636bn FY 20, implying YoY revenue growth of 60%. Farfetch is in a prime position to capitalize on the strong growth in online luxury sales which is expected to rise from 12% of industry revenues in 2019 to over 30% by 2029 – Farfetch should see its market share increase from ~5% in 2019 to ~10% by 2029. This implies a revenue CAGR of at least 25% over the next 10 years.

Farfetch is the leader in luxury eCommerce – it dominates in D2C online luxury retail in addition to being the platform of choice for luxury brands looking for an omnichannel eCommerce solution. It is the most popular online platform with over 2.5m active customers as of June 2020 and over 600,000 SKUs. In Q3 20, Farfetch added Moncler, a top 10 brand to the marketplace and have also recently signed Dolce & Gabbana, Ralph Lauren and RADO. Supply partnerships have expanded to more than 1,300 third-party sellers now participating on the Farfetch marketplace, improving more than 550 brand e-concessions and over 750 retailers.

The nearest marketplace competitor, YOOX Net-a-Porter, owned by Richemont (OTCPK:CFRHF), has not made sufficient investments in its underlying technology and logistics – it lacks the integrated real-time inventory management systems Farfetch has, in addition to cross-border delivery networks and fulfillment. Given Richemont owns YOOX, it competes directly against non-Richemont brands, whilst Farfetch does not, allowing brands to feel comfortable they will not have to compete against the platform as is the case with Amazon marketplace.

Given Farfetch is the preferred platform used by the top 10 luxury brands (including Balenciaga, Hermes, Saint Laurent, Gucci, Dsquared2), it is the preferred service provider to a restricted supply of luxury goods which it can use to continue to expand its penetration – a network effect, which should enable the business to sustain its momentum.

Valuation

Given the stock has soared 4x since March 2020, we need to ask tough questions regarding the valuation. We find the current valuation is not excessive as per a DCF and cross-sectional regression analysis which we explain below.

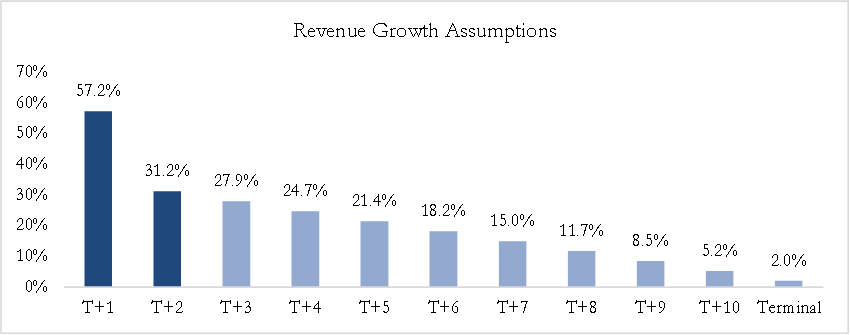

First, ran a 10-year, 2-stage DCF where we assumed consensus revenue growth for the next 2 years, then trailed it down linearly towards 2% in year 10 resulting in the following growth path which implies a 21% 10-year revenue CAGR:

Source: Analyst estimates as per Bloomberg and author’s calculations

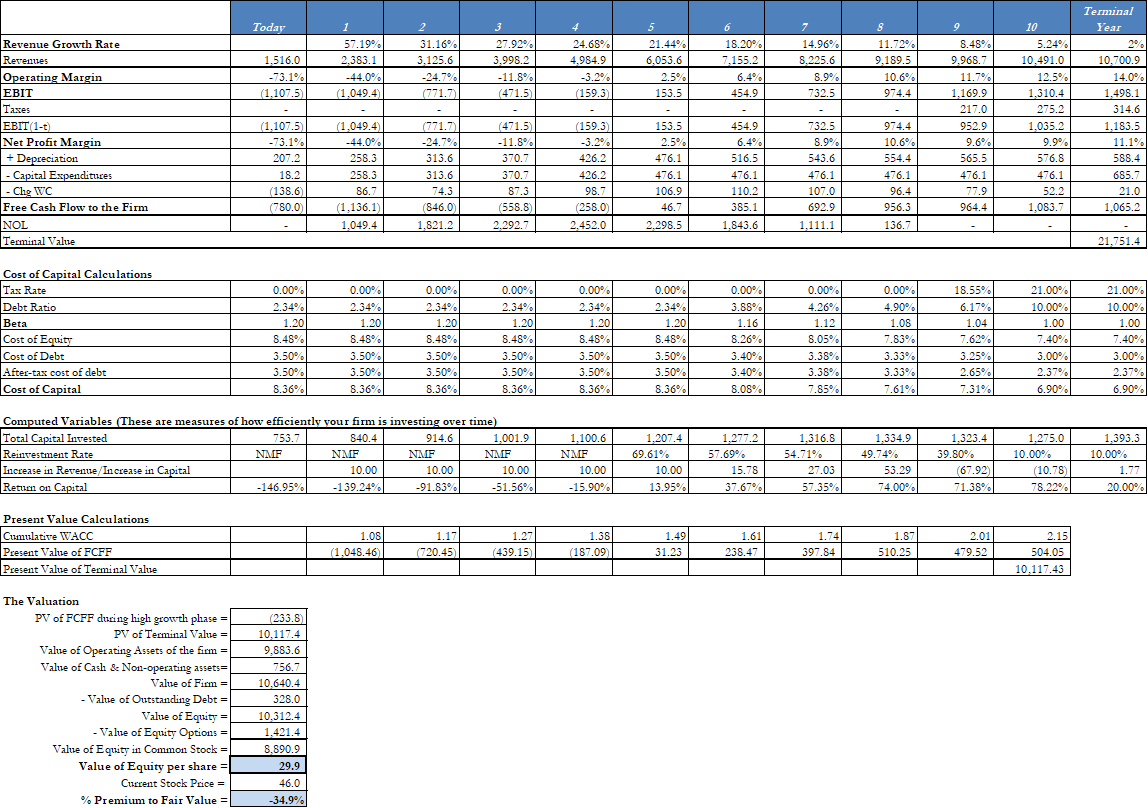

We assume a conservative 20% terminal operating margin in year 10 which is reasonable for a capital-light business Farfetch is. This assumption is also quite conservative as it likely understates what the business is likely to achieve if it manages to shift mix further away from direct sales and more towards its marketplace product. Our DCF implies the stock is ~9% undervalued given a $46 share price:

Source: Author’s calculations

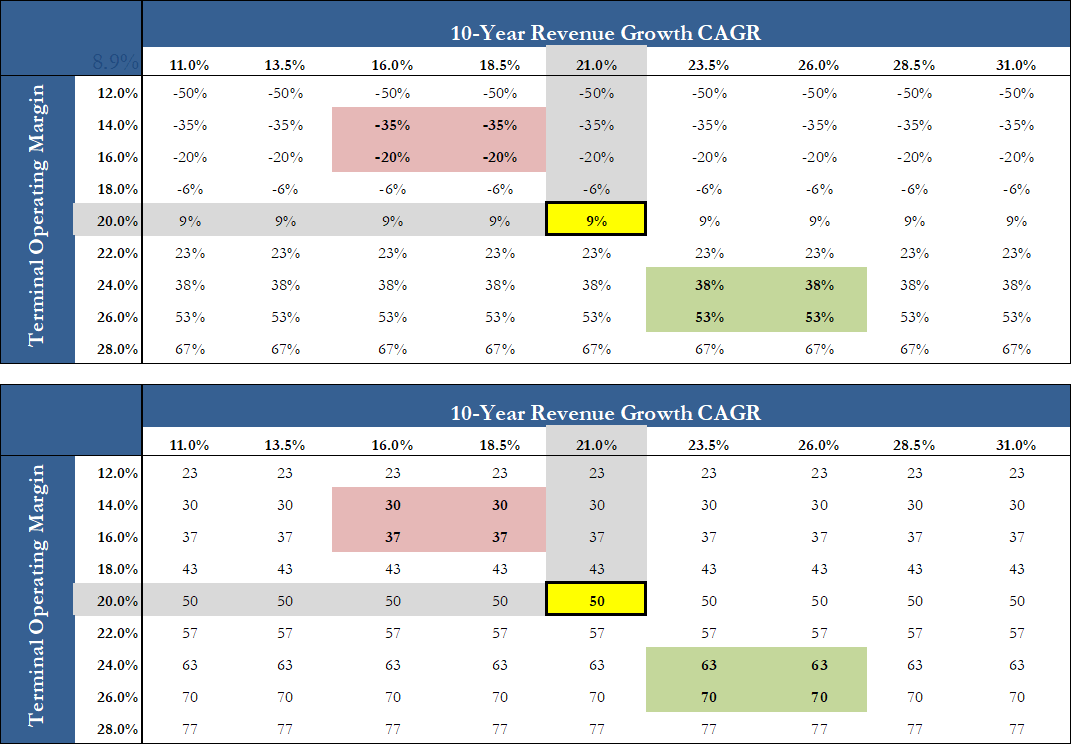

The above represents our Base valuation scenario, we present Bull/Bear scenarios and illustrate a sensitivity analysis of our core revenue growth and terminal operating margin assumptions below.

Our Bull case is a 25% terminal operating margin with a 25% 10-year revenue CAGR – we believe this is achievable given Farfetch is still below $1bn in revenue and it is transitioning further towards its marketplace platform business, investor expectations could reasonably shift towards this scenario. A fair price for the stock in this scenario is $67 or +45% from current levels.

Our Bear scenario is a 15% terminal operating margin with 16% p.a. revenue growth over the next 10 years. This is a somewhat pessimistic scenario given Farfetch is the established leader in its space, it should be able to leverage its position to continue growth at higher rates than this and scale towards better profitability. A fair price in this scenario is $33 or -28%.

The following tables illustrate the range of outcomes as per our DCF, the first table shows the % gain/loss vs. a current price of $46 and the second table contains DCF prices:

Source: Author’s calculations

To complement our DCF, we performed a cross-sectional linear regression of EV/FY1 Sales against FY1 Sales Growth and Gross Margin using a suitable comparable peer-group. Farfetch is a unique business, although its activities overlap or have some similarity to these companies to varying degrees. For instance, the D2C retail component of Farfetch is similar to other online retailers, except none of these is a luxury pure-play. The B2B marketplace platform Farfetch sells to luxury brands is also unique, although it is comparable to services offered by Amazon (AMZN) and Shopify.

Conclusion

Farfetch allows luxury firms to maintain ownership over their brands and leverage its scale to sell online. With over 2.5m active customers, and having made investments into technology and logistics, the company is well-placed to be the online marketplace platform of choice for luxury brands. Investors should look beyond thinking about Farfetch as simply an online store – the platform service it is selling to luxury brands to own their online presence is what investors should focus on. Peers like Shopify trade at significantly higher multiples based on revenue given the superb economies of scale and recurring revenue such businesses generate. Despite the strong share price performance, we believe the shares are still attractively priced and do not reflect the company’s full potential.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}