A weak job market does not bode well for Ally Financial.

Ally Financial

Zacks Equity Research, Piper Sandler, and Goldman Sachs

GS

ALLY

Ally Financial (Ally) share price October 8, 2018 – October 2, 2020)

Yahoo Finance

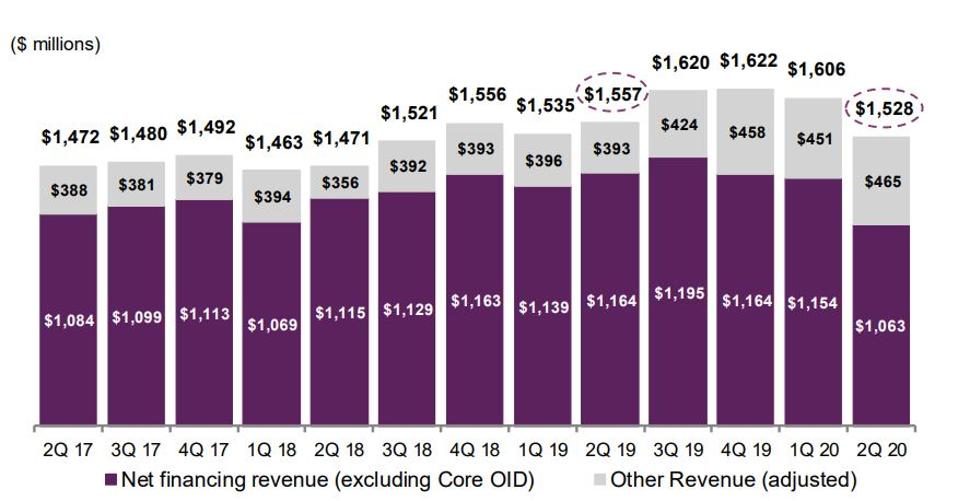

Ally Financial has worked on diversifying its revenues by adding to its digital offerings and introducing new products. Yet, the firm’s adjusted revenues declined for a second quarter in a row. Its second quarter net income of $241 million was a significant improvement over its first quarter loss of $319 million. However, the firm reduced its loan loss provisions by almost 70%. I would like much more transparency to see if such a reduction on loan loss provisions is warranted. Additionally, its performance was adversely affected by an 26% year-on-year decrease in retail auto loan originations as well as an over $10 billion sequential decline in dear floorplans due to declining dealer inventories. Essentially, Ally has lacked the earnings to offset rising credit costs.

Adjusted total Net Revenues; this represents a non-GAAP financial measure.

Ally Financial

According to R. Christopher Whalen, Chairman of Whalen Global Advisors and previously Head of Research at Kroll Bond Ratings Agency, Ally Financial suffers from “poor equity market performance, wide credit spreads, a weak funding profile and a lack of clarity in terms of forward business model.” Whalen also believes that “the market’s assessment, as usual, is correct as illustrated by the fact that ALLY trades at a bit more than half of book value. Like most banks, the ALLY common equity is down 30% YTD.”

Net Loss/Average Assets, %

FFIEC & Institutional Risk Analyst

Whalen’s analysis also points out the importance of looking at market signals which are more dynamic than relying only on financials or on ratings. “A review of public benchmarks suggest that the performance of ALLY is mediocre,” said Whalen. Analyzing data from according to CapIQ, Whalen pointed to the fact that Ally Financial is “trading at a book value multiple of equity ~ 0.6x and that ALLY has a beta of 1.6x the average market volatility and a forward dividend yield of 3.25%.” As of September 25th, Ally had an implied credit default swap (CDS) spread of 132 basis points over the curve; this is twice the spread for the largest U.S. banks. This means that market investors are worried about a rising probability of default of Ally Financial bonds. The CDS spread that is generated by Bloomberg, maps to about the ratings agency equivalent of about +BB plus.

R. C. Whalen

Whalen Global Advisors

Ratings presently lag this market implied rating. Nonetheless, because rating agencies have bond investors first and foremost on their minds, they are more critical about Ally’s financial condition than are stock analysts. Fitch Ratings has a current rating of BBB- and a negative outlook on Ally Financial. According to Fitch Ratings analysts “Ally’s ratings remain supported by a strong franchise, leading market position in the U.S. auto finance industry, solid track record in credit performance, diverse funding base, ample liquidity, adequate risk-adjusted capitalization and seasoned management team.” Yet the analysts believe that Ally Financial is constrained by its “concentrated and cyclical business model and higher price sensitivity on internet-sourced deposits relative to branch-based banks.”

Moody’s

MCO

Already in April, DBRS Morningstar had confirmed Ally Financial’s long-term issuer rating of BBB (low) and short-term issuer rating of R-3. DBRS revised its outlook on Ally’s long-term ratings from positive to negative, and revised its short-term ratings outlook from positive to stable. The outlook revisions took into account the “abrupt and severe economic downturn” related to the coronavirus pandemic and the expectation that this would negatively impact Ally’s financial results. DBRS Morningstar expects “material profitability pressures” as a result of the “dramatic decline” in auto loan originations and deterioration in the company’s credit quality.

As Whalen points out “ALLY has lower gross spreads on its loans and higher funding costs than do the larger banks.” FFIEC data shows that ALLY has tracked below its peer group in terms of this key measure of profitability and asset returns. Caveat Emptor!

Net Income/Average Assets, %

Institutional Risk Analyst and FFIEC

Note: Ally Financial will release its third quarter financials on October 16th.

{kind=link}