Vistra (formerly “Vistra Energy”) (VST) hosted their annual Capital Allocation Plan this morning, outlining near-term guidance for 2020 – 2021 as well as several core development plans stretching out to 2030.

In this update, I will review the guidance, provide valuation estimates, and discuss VST’s longer-term growth opportunities.

Near-term Guidance

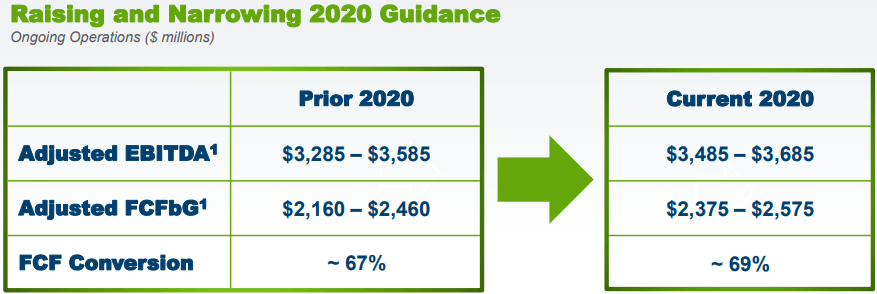

Vistra executed well during the COVID-19 crisis, exceeding management’s own expectations by demonstrating consistent and growing profitability during the roughest of economic conditions. More importantly, VST is expecting to hit and exceed the original EBITDA and FCF targets for 2020 as demand has returned to pre-COVID-19 levels.

The Company raised its guidance on both counts for 2020…

Source: Vistra Investor Call

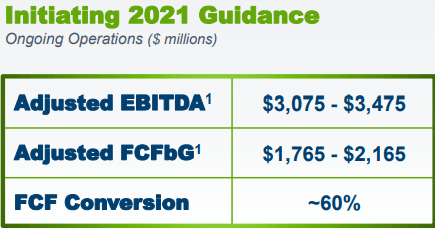

…while adjusting but still maintaining mid-point target guidance for 2021, with expectations leaning towards the higher end of that guidance (and the possibility of even exceeding it):

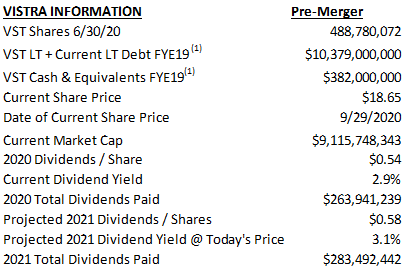

VST also announced an increase in its dividend distributions from a current $0.54/share to $0.58/share in 2021 to keep in line with both its target growth rate of 6-8% as well as its historic target yield of 3-4% with a bigger step-up to $0.76/share expected in 2022 (and larger step-ups to be discussed in the future).

This gives us enough data to help triangulate on a target valuation using the following additional information:

Source: Author Compilation

From a valuation perspective, the company remains significantly undervalued, but before diving into a few valuation exercises, let’s do a quick run-down on what may be driving the depressed stock prices:

This stems from VST’s legacy assets which have a history (pre-2015) of private equity ownership that led to excessive leverage and a subsequent liquidation/reformation/rebranding of the company.

- Historically High Leverage Ratio (>5x Adjusted EBITDA)

Over the past several years, management has remained laser-focused to reduce this leverage ratio to a target of 2.5x Net Debt/Adjusted EBITDA. As of today, they will achieve that target this year.

Already, the credit agencies have begun adjusting their ratings on VST, with Fitch (September 2020) raising VST’s credit rating to one-notch below Investment Grade (in line with Moody’s rating). VST expects to achieve an IG rating by end of 2021 which will provide VST with more attractive financing rates and terms, open the doors to a broader investor pool, and enable VST to pursue more attractive projects with counterparties who are limited to working with IG rated partners.

- Loss of Adjusted EBITDA from Asset Conversion

Fears of lost Adjusted EBITDA contributions abound, resulting from the transition away from carbon generation assets (e.g., coal generation – aka “Sunset” assets slated for closure between now and 2030)

VST over the past year has established existing Net-zero/Renewable projects (e.g., Solar and Battery Energy Storage Systems) and a future development pipeline of net-zero/renewable projects that will more-than-replace the lost “Sunset” asset EBITDA contribution losses.

- ERCOT Competitive Market Dynamics

ERCOT (“Electric Reliability Council of Texas“), is somewhat unique relative to other utility markets in that it runs a competitive marketplace for generation and distribution (e.g., unlike most utility markets where monopolies are established with fixed/contracted rates of return). This had made investors leery of the incumbent leaders Vistra and NRG (NRG) due to uncertainty of how sustainable and volatile a market like that can be.

For the past 5 years, VST has proven itself to be resilient in the ERCOT market marketplace demonstrating leadership, growth, profitability and stability through an integrated model that matches both Retail demand and Generation supply in a low-cost efficient manner. VST has since proven, during the peak of COVID-19 and the Texas resurgence, to be both countercyclical and resilient and a safe-haven for investment funds.

Valuation

- Adjusted EBITDA Valuation Estimate

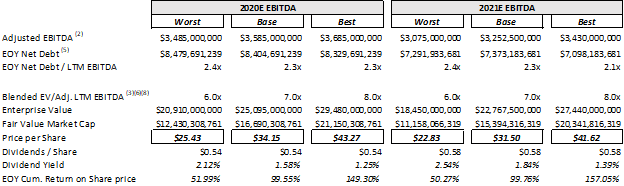

Given the above basic assumptions and discussions, I believe that VST remains both a low-risk and significantly undervalued growth utility. Based on a Blended Rate EBITDA Trading Multiple (assuming FCF after Growth Capex is used for debt paydown), the target minimum FY 2021 share price would range from a minimum of ~$23/share to a maximum of ~$42/share. This depends on where you fall in the spectrum of the selection of forward blended Adjusted EBITDA multiples and the outcome of forecasted FY 2021 Adjusted EBITDA guidance:

Source: Author Analysis

It’s important to note that with the higher guidance on 2020E Adjusted EBITDA, VST will have already met and exceeded its target leverage ratio of 2.5x (see chart above) by year-end. For 2021, I have assumed that VST will apply any remaining cash flows for 2020 to further debt reduction due to the lower Adjusted EBITDA guidance anticipated in 2021, in order to ensure maintenance below the 2.5x leverage ratio.

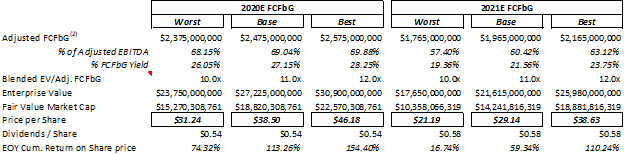

- FCF Yield Valuation Estimate

Another alternative valuation technique is to look at Free Cash Flow before Growth Capex (“FCFbG”) yields. Since FCFbG yields are not expected to decrease in the foreseeable future beyond 2021, we can estimate VST valuation based on an analysis of its Forward 2021E FCF Yield of ~20%+ and current Blended EV/ FCFbG trading multiples. From this analysis, the target minimum FY 2021 share price would range from a minimum of ~$21.19/share to a maximum of ~$38.63/share:

Free Cash Flow Yield Share Price Valuation Estimates

Source: Author Analyses

Note: This valuation is somewhat conservative as a result of an ~5% reduction to FCF conversion rates to 60% in 2021 resulting from a one-time expense associated with the closure of carbon generation assets. This is a non-recurring charge and conversion rates are expected to return to 65% thereafter (increasing FCFbG by ~8.3%). However, for the purposes of being conservative, I chose to use the lower guidance which estimates as they still demonstrate how “undervalued” VST is relative to its intrinsic value.

- Share Repurchase & Associated “Project” Valuation Estimate

VST also announced an aggressive proposed share repurchase program (subject to Board Approval) expected to launch at the start of 2021 and extend for two years thereafter. VST is planning to allocate up to $1.5Bn of its FCF (or equivalently, more than 12% of its current market capitalization) for share repurchases.

Another method to help triangulate on what the appropriate share repurchase price target should be is to examine “Project investment” targeted returns with VST’s targeted minimum project return of 500-600bps in excess of cost of equity.

This method assumes that a share repurchase should be viewed as on par as an “investment” with the same associated target returns as a project. This method would establish a minimum floor target of 15% – 16% (i.e., VST’s targeted after-tax return on equity inclusive of the 500-600bps gap) to reverse engineer an associated implied share price.

Equivalently, this would imply (see below) a share repurchase target of between a minimum of $22.57/share and a maximum of $29.53/share based on 2021E FCFbG (in line with prior statements by the CEO advocating for a share repurchase program when the shares were trading at ~$22 per share):

FCFbG Share Repurchase Price Target Estimates

Source: Author Analysis

It is important to note that the CEO specifically is the number one Capital Allocator given where shares are trading at today (and reiterated that several times during the call).

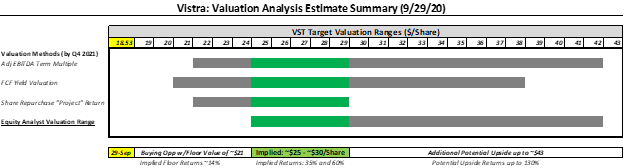

Equity Research Analyst Valuation Estimates

It helps to actually sanity check these valuations with what Equity Research Analysts think. There are three equity research firms that recently covered Vistra since their 2nd Quarter earnings release and who have issued price targets over the last two months:

- Credit Suisse, Michael Weinstein maintained a price target of $32/share on 9/28/20 with a upside guidance of $43/share (in a “blue sky” scenario)

- RBC Capital, Shelby Tucker maintains a Buy rating as of 8/16/20 with a price target of $25/share.

- UBS raised its price target to $32/share while maintaining a Buy on 8/6/20.

The Equity Research Analyst price targets generally range from $25 to $32/share, reflecting a ~35% to ~70% return (based on the closing price of $18.50 as of 9/29/20) with a “blue sky” target of $43/share.

In summary, the implied valuation, across all 3 of my valuation estimates and in comparison with the three equity analyst estimates, is between $25 – $30/share (reflecting a ~35% – ~60% return on the current share price of $18.53 as of 9/29/20).

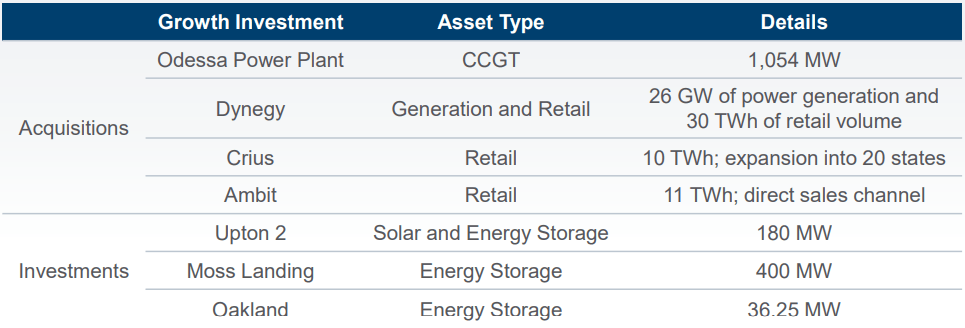

Beyond 2021

Vistra has already established a relatively new foothold in Energy Storage Systems (ESS) and Solar Energy investing as renewable energy assets and:

Source: Vistra Investor Call

Most notably, Moss Landing has been the subject of much discussion in the press with a recent permit approval for an expansion up to a global record of 1,500 MW of ESS (currently at 400MW-already a global record in itself, with an additional 350MW under review, and approved environmental permits for an additional 750MW thereafter).

This new flagship expansion will play into Vistra’s ongoing transformation into a zero-carbon portfolio under a new brand, “Vistra Zero” (consisting of over 4k MW in development or under operations today) that will leverage VST’s:

- Growing expertise in the development and operations of renewable assets

- Distribution network for “clean” energy to their ~5MM retail customer base

- Economies of portfolio scale (e.g. construction and procurement)

- Existing land/sites

- Fortified balance sheet

Source: Vistra Investor Call

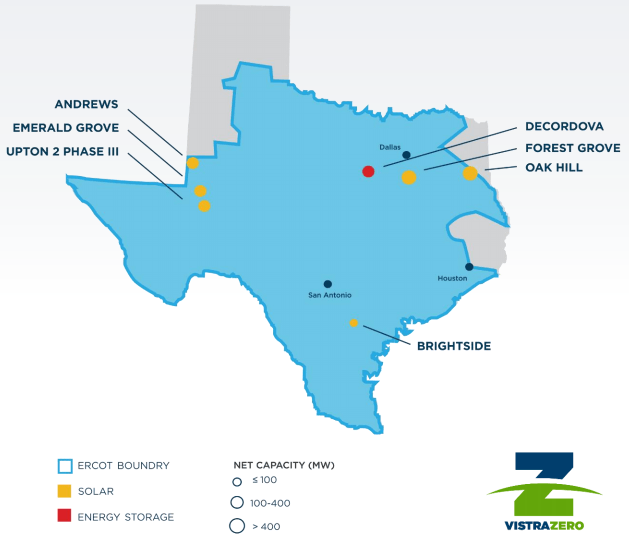

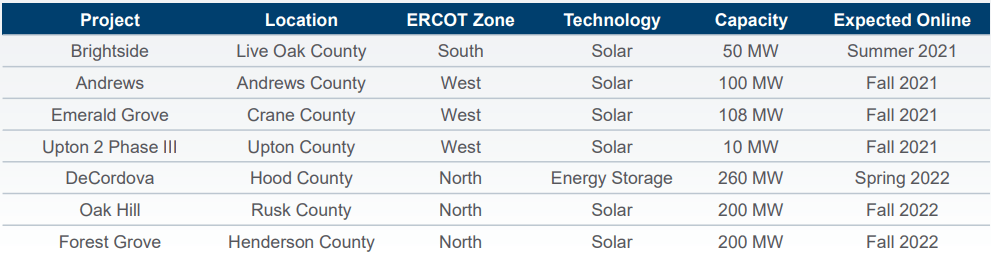

The Company also announced today the details of Phase 1 projects in Texas accounting for almost 1,000MW of solar and ESS projects with returns in excess of 18% average expected levered returns and EBITDA growth of $90-$100MM/year:

Source: Vistra Investor Call

Each of the above sites slated for development also allow room for further expansion as demand grows and load balancing is required.

As the shift in the generation portfolio trends towards renewable energy (with more than 50% of VST’s power generation Adjusted EBITDA contribution coming from carbon neutral sources by 2030, 70% by 2040, and Net-zero Carbon Emissions by 2050), VST’s EBITDA trading multiple should shed the “dirty energy” discount (from its coal generation assets) and trending closer to 10x Adjusted EBITDA of its clean energy peers (driving further share price appreciation). Regardless, natural gas will remain a core part of VST’s generation portfolio as a relatively efficient low-cost low-carbon source of energy for the foreseeable future.

VST management has stated that its Texas Phase II pipeline will be announced in the near-future with an additional >1,000 MW of solar and storage in that pipeline.

Outside of Texas and California, VST is pursuing ~450MW of solar and ESS opportunities in Illinois pursuant to tax benefits provided under the Coal to Solar and Energy Storage Act.

Inorganic Growth

During the call, VST also announced two inorganic opportunities:

VST has invested in a venture fund focused on technological innovation and sustainability to help accelerate the viability of carbon-free and carbon-reducing technologies

VST made it clear that they will also continue to look for tuck-in acquisitions focusing on their retail markets (with a focus to matched balance in the East and ERCOT). Since NRG, VST’s largest competitor in the ERCOT market, is tied up in a merger, I believe this will open up opportunities for VST in pursuit of other retail target opportunities to grow the customer base.

Conclusions

Vistra is set to re-energize its share price with growing and consistent profitability. I believe Vistra shares represent a low-risk opportunity for a 35% – 60% upside to shareholders as a result of historically depressed prices. Today’s “Capital Allocation” call represents a “crystal ball” not only into Q3’s earnings but also a roadmap into the next decade of strategy and growth for a company that has outperformed every year since they emerged.

Disclosure: I am/we are long VST. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: We pride ourselves on conducting extensive primary & secondary research, analyses, and/or interviews with Senior Management, Partners, and/or Customers in order to identify and vet undervalued investment opportunities. That said, we aren’t always right and these are just our humble opinions. Don’t get us wrong, we would love for you to follow us to show you the “hidden” gems we find, but we also always encourage everyone to do their own homework and research and as the saying goes….BUYER BEWARE. Happy investing!

{kind=link}