Investment Thesis

Baxter International’s (NYSE:BAX) global presence signals fundamental strength, albeit with a bumpy Q2 exit, missing the Street’s estimates on revenue by -4%, net income by -21% and EPS by $0.07. BAX has comparative advantages relative to peers within the medical devices and instruments industry, as the revenue model does not rely on utilisation rates of elective procedures alone; rather on home care, hospital admissions and providing critical therapy for those with life-threatening conditions, such as acute renal care and peritoneal dialysis, to give example. Thus, BAX’s performance was not as heavily impacted relative to peer entities in this time, nor from centres who elected to close elective procedures in the wake of government social-distancing restrictions and to reduce COVID-19 transmission rates.

Data Source: Market Data; Author’s Calculations

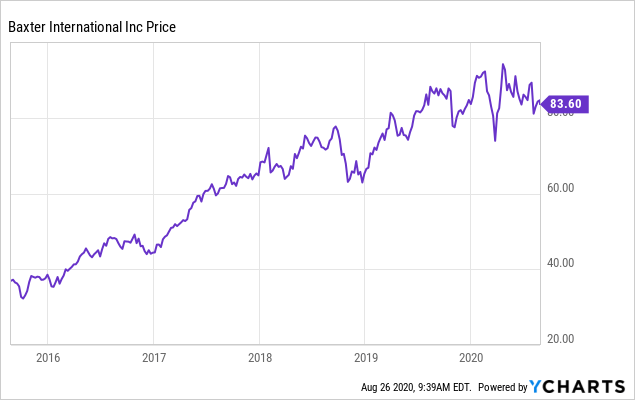

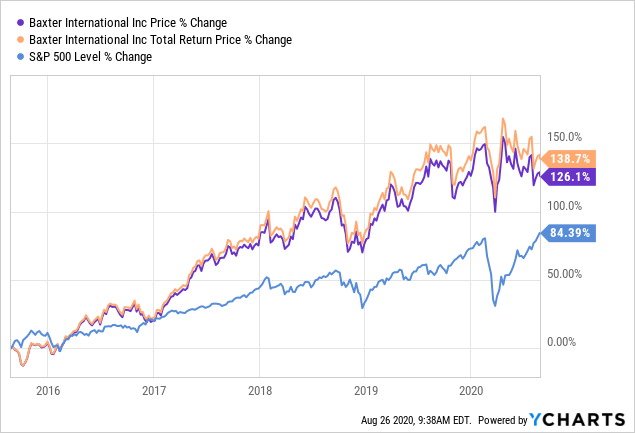

The market has consistently viewed BAX as a leading player within this operating domain for the previous 5-year period, and shareholders have enjoyed over 138% in total returns over the same term. Additionally, BAX recently declared $0.245/share dividend in July on a forward yield of 1.17%, evidencing the company’s commitment to sharing value to shareholders, alongside the financial strength of the company in operating in tough times. As such, the stock has seen steady growth over the long term with favourable upside along the way.

Data by YCharts

Data by YCharts Data by YCharts

Data by YCharts

We hold a long-term bullish outlook for Baxter and firmly believe the company holds fundamental resilience, coupled with the economic pillars to provide ongoing value to shareholders, over the coming 3 to 5-year period at least. We view a number of visible factors (amongst others discussed further along in this report) are evident to justify Baxter’s fair or undervalued status and signal ongoing revenue growth coming out of the pandemic, including:

1. Macroeconomic Considerations

As the economy slowly reopens rolling into 2021, hospital admission utilisation rates and home-care therapies will correlate to higher demand for BAX’s product suite, particularly for anaesthetics and injectables. We foresee global utilisation of hospital admissions and critical care procedures to be at around 60% of pre-COVID-19 levels by September/October, from discussion with experts and from data sets obtained via leading international government statistical measures. Furthermore, Baxter’s position as a global entity benefits top line earnings from multiple revenue arms for product supply, particularly in large, emerging markets such as Brazil and India, whom continue to gain greater access to improved healthcare standards and treatment of critical conditions, such as renal pathology and cardiothoracic conditions. BAX also flourishes in the home-care segment within these markets, where the model of healthcare and medical delivery reflects the same. Baxter’s global scale has created structural advantages at this time; the presence in many markets alongside the diversified operational suite ensures that the company generates revenues from the major aspects of healthcare delivery within each of these zones. Production facilities throughout Europe in strategic locations such as Malta enable low gross margin pressure and lower marginal costs to production, whilst maintaining a high standard of quality control. Further, as procedures and medical equipment continue to evolve over time, as they historically have done over the past 150 years, BAX’s position at the forefront of manufacturing and innovation will continue to place the company at the head of the bull in terms of capacity, commercialisation and distribution in key markets, not only for the company but for medical/healthcare personnel, whilst benefiting patients in the domains that BAX operates its product line.

2. BAX’s posture on revenue and FCF growth to date

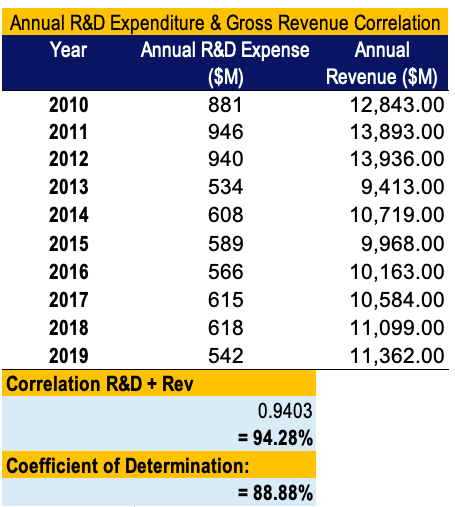

Baxter has grown TTM quarterly revenues at a CAGR of 6.85% over the past 3-year period and FCF at a 5-year CAGR of 12.57% to date. FCF has also expanded 49.44% YoY, and BAX has shown demonstrated growth in ROCE and satisfactory ROA over the 3-year period to date. Revenue growth over the previous 10 years is highly correlated with R&D expenditure at 94% correlation, with 88% of changes in revenue caused by changes in R&D expenditure, evidencing the importance of these figures to the company’s top line and management’s effectiveness in garnering return on invested capital.

Data Source: Author’s Calculation’s

Data Source: Author’s Calculations

3. Sturdy FWD gross, net and operating margins on OCF of $2.25 billion

Gross and net margins of 42.8% and 8.1%, respectively, alongside strong EBITDA margin of 17.5%; each showing resilience to pressure from reduced sales and marginal cost increases. Strong OCF margin of 19.7% showing YoY growth, with no foreseeable drains or pulls on liquidity highlights that the company is well situated to incur additional costs and any hits to liquidity without facing operating margin pressure.

4. Transparency from leadership

Providing clear guidance ranges in sales and earnings expectations for the remainder of FY2020, whilst highlighting potential risks for the company and therefore to shareholders. Guidance range of -1% to 1% sales growth for the remainder of FY2020 sheds light into company expectations, which the market will look to accurately price in amidst the continued flight to quality with the fallout from the pandemic. There is plenty of room to scale from these conservative figures as well, and management has purportedly modelled guidance using a variety of inputs to gauge accuracy over the forecasts.

5. Ongoing dividend growth and commitment to fulfil ongoing dividend payouts to shareholders

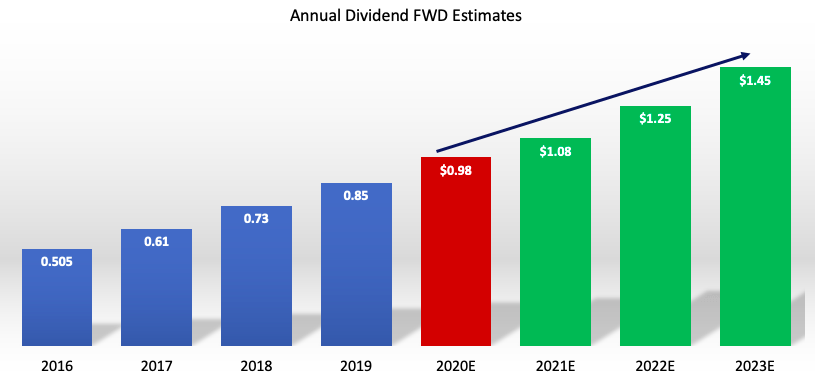

Ongoing dividend growth of 113% at a CAGR of 18.95% since 2017, alongside recently posted payment of $0.245, further highlights the strength in the company’s balance sheet, in addition to commitment to value for shareholders. Dividends have climbed at a CAGR of 3.88% over the previous 10 years. Within the quarter, the company announced an 11% increase to the quarterly dividend payment, again illustrating this sentiment, aiming for an annual dividend of $0.98/share. The dividend completion in the current market makes the stock attractive as a buy for income-style and value investors alike, especially those with a dividend-capture strategy. Dividend yield of 1.16% is above the 4-year average yield of 1.0%, and although in the lower quartile of US equities, with the commitment to ongoing dividend growth, shareholders can enter at the current market price and enjoy sustained dividend growth for years to come.

6. Adequate dividend coverage from FCF of $1.502 billion with expected growth in dividends of 13.95% over the next 3 years.

Favourable coverage from FCF of 33.5x with sustainable payout ratio of 32.03% adds weight to the company’s financial strength and ability to reward value to shareholders, plus incentivising future shareholders who will look to fly to quality coming out of 2020. Management has committed to ongoing dividend payouts and growth is expected until 2023 at least, at a CAGR of 13.95% on average.

Data Source: ValueLine BAX; Author’s Calculations

7. Debt facilities are well covered alongside competency in debt management

Debt obligations and interest payments are well covered from OCF and FCF, whilst management has successfully reduced the debt/equity figure from 139% to 84.7% over the 5-year period to date. As of 30th June, there were nil borrowings from the available credit facility both in US and Euro denominations. In March of this year, the company issued senior notes in a principal of $750 million, paying a 3.75% coupon due in October of 2025, alongside a $500 million issue of senior notes for maturity in 2030, at a coupon of 3.95%. Therefore, the company has no meaningful debt maturities within the next 3-year period. The total issuance was for $1.2 billion providing a forceful liquidity injection and bolstering the liquidity position for the company, to weather any financial storm that may arise out of the turbulent nature of the pandemic on the markets.

Interest expense will rise as a result of these issuances plus issuances in Euro from 2019; however, it is well covered by the EBIT total and will remain so for the foreseeable future based on earnings estimates.

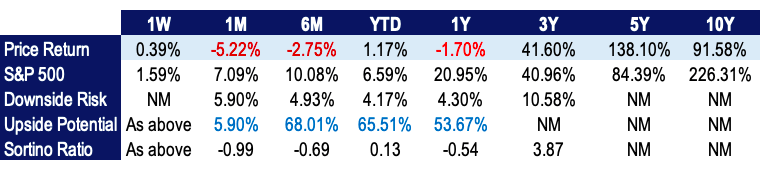

8. High historical total returns on limited downside risk exposure and upside potential ratio of 65.51% on YTD returns

Regarded, not indicative of future returns, however, the market has consistently priced in ongoing earnings growth and the fundamental basis of the company’s strength in their operating markets. Downside risk has hovered historically between 4% and 6%, which sits perfectly within our threshold where we seek to identify stocks with asymmetric risk/reward profiles that offer adequate compensation at a low level of risk in price returns.

9. Evidence of ongoing reinvestment into net working capital, with 91.92% growth in NWC investment YoY

The repeated history of reinvestment into NWC showcases BAX’s operational flywheel, which will likely generate more torque as time goes on and the reliance on advanced health and medical equipment from society also progresses. The torque already has surfaced in the company expanding their existing markets, whilst diversifying the product suite and portfolio to accommodate additional markets that cover all major domains within the healthcare paradigm, including: pharmaceuticals, renal care, medication delivery, clinical nutrition, advanced surgery, acute therapies and other segments within the greater industry. Many patients who require assistance within these domains will be using Baxter’s products alone.

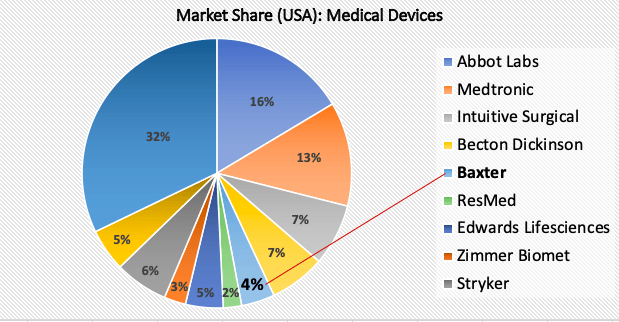

10. The medical devices and instruments market is huge and growing, barriers to entry in Baxter’s existing markets are high, and the revenue model on Baxter’s product placements is superior

The USA has the largest medical devices industry at $157 billion, which also represents 40% of the entire global market, which is around $390 billion on estimate. By all accounts, the US market is forecasted to grow by 33% to $208 billion by 2023, and $518.7 billion globally. BAX captures around 4% of the US market alone. Baxter claims the crown in the majority of its product lines within this domain, whilst competing within a dense peer group. For instance, BAX is a clear winner within the renal replacement therapy domain, in our opinion. To illustrate further, Baxter is only behind Fresenius Medical Care (FMS) to be the second largest dialysis and related equipment provider. Furthermore, in their advanced surgery segment, the firm’s proprietary technology in bleeding sealants and haemostats through their Tisseel and Floseal products, position it as the second largest US player in the market to regulate bleeding and wound closure, with Johnson & Johnson (JNJ) the top-tier here.

Data Source: Market Study; Author’s Graphic

However, Baxter take charge in the peritoneal dialysis segment, with around 70% of total patient share within this domain, and hold around 10% patient share in the haemodialysis segment. We also firmly believe that any competing firms will face difficulty in entering the niche segments BAX operates within, partially due to the high costs of switching that are associated with specialist medical equipment; and via intangible barriers, through Baxter’s proprietary protection over their technology and manufacturing processes. For instance, recent shortages of IV solutions to cover the broad spectrum of IV requirements partially evidence this point. Moreover, costs for production via a compliant manufacturing base would total over $300 million and take 3 years to fully complete, from estimates conducted by key players within the domain, in which time significant advancements to compounds and agents will likely be made, rendering the planned facility useless in capacity and competitive prowess. The time consumption alongside the ongoing expenditures required for compliance and regulatory acceptance is also high.

Following placement of its products, namely the peritoneal dialysis equipment, payment to Baxter is structured to reflect usage of the equipment, plus additional consumables via a subscription model, paid monthly. Each of the required attachments and solutions are actually distributed via Baxter themselves through their own channels. On this basis, patients are unlikely to switch between equipment providers, primarily as the treatment is self-administered, and if treatments are working, patients are disincentivized further to change providers or seek new equipment. Therefore, this model creates an ongoing source of revenue from the equipment itself, and the recurring turnover of the required consumables that relate to said equipment. In addition, patients benefit from the BAX’s “Sharesource” software that relays information and treatment results directly between medical personnel and patients receiving treatment, thereby eliminating the requirement for face-to-face consultation. This has added advantages within the current climate of restricted patient access from the pandemic. The benefits also extend to remote environments and in emerging markets, where patients may have low accessibility for transport and clinic locations.

Away from renal care, infusion pumps are a part of BAX’s arsenal and competitive battering-ram. This technology assists medical personnel, enabling staff to administer therapies by cutting down steps involved to complete various procedures. Additionally, throughout its life, the equipment remains contributing to ongoing revenue streams, through the consistent sets of consumables that go along with this type of technology, namely through injectable solutions, where most injectable therapies are administrable through the infusion pump, generating additional revenue streams from the one device. The long life of these pumps also bolsters the time-length of recurring revenue, from sales of the required add-on consumables. Additionally, facilities are unlikely to disrupt procedural care administration by routinely switching machines and devices from alternate providers. They are more content with sticking with one brand, where additional therapeutic value is generated via other modes of treatment and medical equipment supply. Additionally, the proprietary protection of this technology ensures that BAX remains at least in second position for the largest US provider, behind Becton, Dickinson (BDX) within this equipment domain. We have also heard of at least four innovations in infusion pumps from BAX, to be launched throughout the remainder of 2020 and into 2021, to permit a single unit that envelopes larger volume pumping, IV administration, and analgesia.

11. There are additional competitive and comparative advantages within the product segments

We see the company’s proprietary systems at play within its clinical nutrition segments too, primarily through un-replicable nutritional formulae, alongside modes of delivery under proprietary protection. Baxter even separates itself from peers within its generic pharmaceuticals markets, offering a competitive advantage by competing in segments that require complex manufacturing and administering of agents. For instance, within the inhaled anaesthesia and injectables segments, there are only a small number of participators, secondary to these complex manufacturing processes, compared to the oral counterparts that exist for similar administration. Additionally, by offering these injectables in a ready use state, there is a huge advantage in infection control, whilst reducing timing of the procedures involved with the injection. Medical personnel are therefore drawn to usage of these compounds, which sets Baxter clearly apart here.

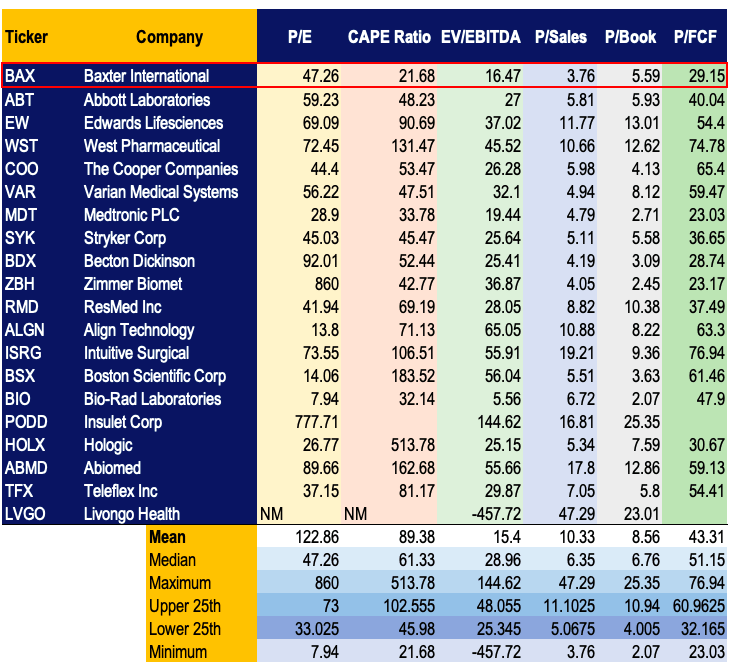

12. Strength in Valuation metrics from DCF analysis and comparables within the industry, particularly in P/FCF, P/Sales, EV/EBITDA and the CAPE ratio

From this examination (seen below), the company’s valuation is justified and is currently trading either at fair value or below, in relation to peer entities within the industry. The valuation also highlights market expectations for the company and gives weight to the repeated history in stability and resilience, particularly within the current economic climate.

We firmly believe that investors continue to view the long-term opportunities in cash flows and earnings potential for Baxter, to add to the appeal of the longer-term horizon. Presently, in the current market climate, we are undoubtedly susceptible to higher short-term volatility surrounding quarterly earnings, and revenue slumps from poor market conditions on the supply side. However, we see these as largely seasonal in the short to mid-term, and thus will have no bearing on the long-term bullish outlook for BAX. For instance, BAX has missed earnings estimates exiting Q2 with a possibility of the same reoccurring into Q3 and Q4 of 2020. Aside from these points, in respect to the pandemic being the major cause, we do not see any other drawdowns to our long-term bull case, as a short-term pullback or stagnation in price growth will unlikely have any reasonable impact on BAX’s competitive standing.

Our blue-sky scenario is based on revenue growth at a CAGR of 5.45%, with ongoing growth in EBITDA and CAGR FCF growth of 9.5% to 2025. We also see a sustainable FCF growth rate of 9.5% long-term, and long-term dividend growth at 9.15% in this case and our valuation reflects 7.1% upside from today’s trading price, to reach a target price of ~$90, from both our DFC target from FCF and 2-stage DDM model.

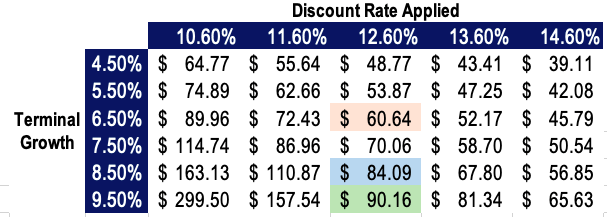

Our grey-sky scenario sees the stock as overvalued by around 20% and is based on FCF growth of 6.5% to 2025, and would result from lower than expected sales growth, alongside unforeseen impacts from COVID-19 on the long-term outlook. Here, we see a price of ~$60, representing approximately 40% downside from today’s price.

In the base case, our assumptions are at 8.5% FCF growth and dividend growth of 8.15% and are based on conservative trajectories of revenue and EBITDA. From the company’s track record in product supply and key differentiators in each of its markets, the top-tier position it holds within each of these segments, in addition to the citadel surrounding the company’s operations, we firmly believe that BAX will most likely adhere to the blue-sky scenario, thus we are assuming an outperform rating on the stock to date.

Performance To Date & FWD Growth Estimates

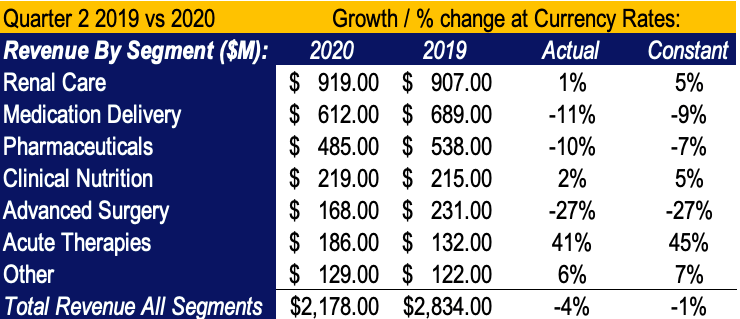

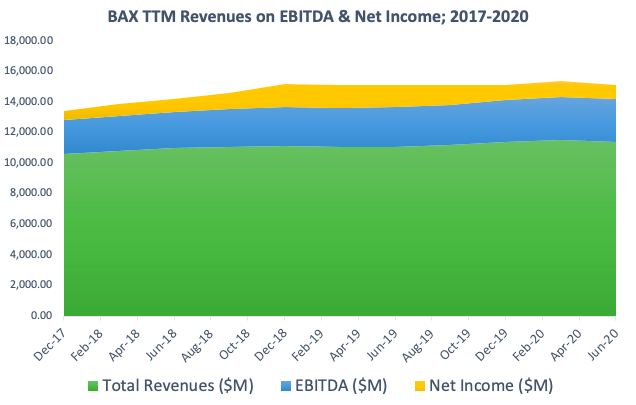

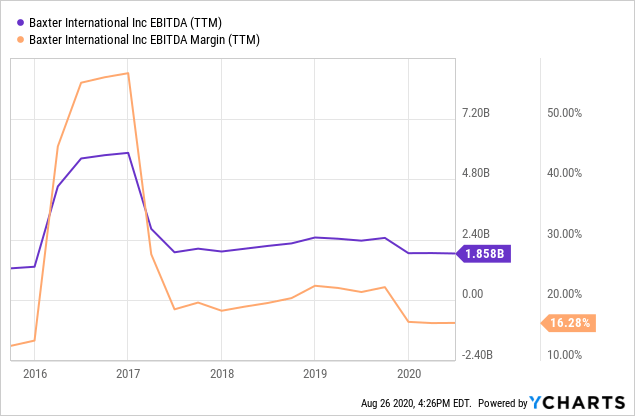

TTM revenues and net income for the exit of Q2 were $11.41 billion and $924 million, respectively. On these earnings, the company enjoyed gross and net margins of 42.8% and 8.10%, respectively, with an EBITDA margin of 16.28%. Revenues have grown at a CAGR of 2.73% over the 5-year period to date, and numbers have shown resilience to the turmoil faced by the markets from the pandemic. On a segmental basis, the company shone in its dominating segment of renal care growing revenues by 1.3% YoY in the midst of this turmoil. Elsewhere, other segments suffered losses, primarily due to COVID-19 related forces, albeit clinical nutrition which grew by ~2% YoY. We would like to see greater CAGR revenue growth closer to 5%, in companies who we believe will consistently deliver value to shareholders. However, BAX’s standing as a mature, stable growth company aligns itself with the capacity to generate additional revenues in the wake of uncertainty coming out of 2020, which is a favourable outcome.

Data Source: BAX 10-Q June 2020; Author

Data Source: BAX 10-Q & 10-K; Author

Data by YCharts

Data by YCharts

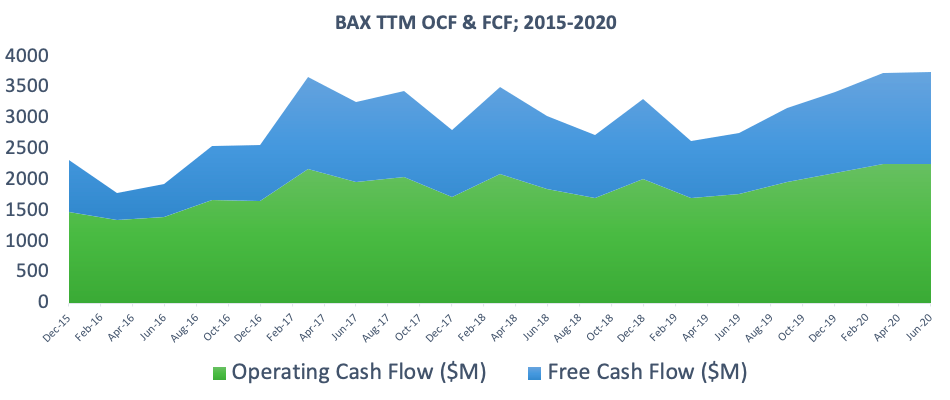

Furthermore, FCF has been impressive over the 5-year period to date, remaining positive and showing growth of ~44% YoY and a CAGR of 12.57% over the 5-year period to date. This is pleasing to us, and we seek companies with demonstrated growth in FCF and also free cash flow growth YoY, to gain insight into future company performance. OCF has shown a similar trend and matched FCF largely in terms of growth and revenue performance. In these uncertain times, the fact FCF has grown YoY and has an upward trajectory, we feel this further illustrates the strength of the company in delivering value for shareholders, especially in maintaining dividend payouts and funding ongoing capital expenditures.

Data Source: Valueline BAX; Author’s Graphic

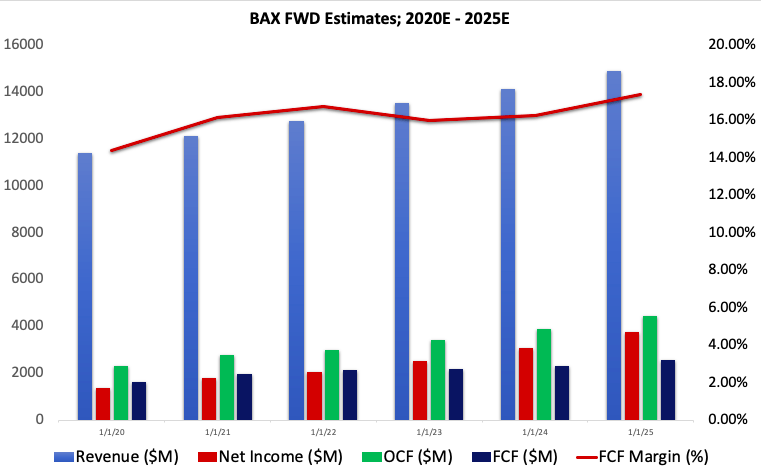

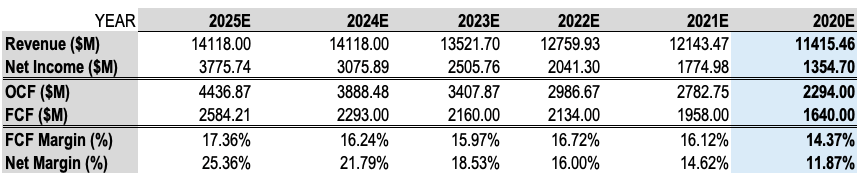

Our estimates align with analyst forecasts for future revenues and FCF growth. We have obtained figures using our own analysis and by performing linear regression over the consensus of analyst estimates. From our examination, we foresee revenues climbing at a CAGR of 5.4% over the coming 5-year period, alongside growth annual in FCF of 9.52% over this same term in the blue-sky scenario. Currently, FCF is 13.1% of turnover, and based on works in the pipeline, BAX’s non-reliance on elective procedures and key differentiation in product areas, we firmly believe the FCF margin will expand to almost 18% by 2025, representing superb value for shareholders and enabling ongoing coverage of dividends over this period and beyond.

Data Source: Author’s Calculations

Data Source: Author’s Calculations

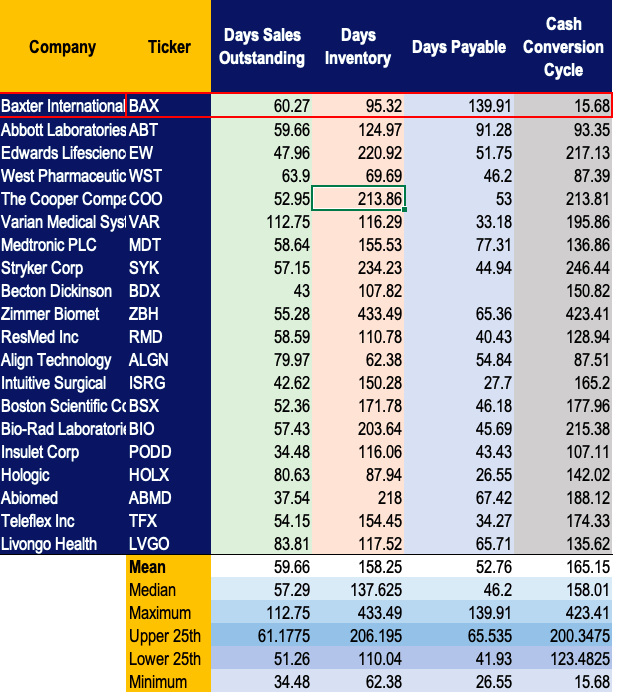

On an operational basis, we are extremely pleased with the company’s evidenced performance to date, most notably in inventory turnover and their cash conversion cycle. We see the company as demonstrating greater operational capacity from this point relative to peers, with a cash conversion cycle of around 16 days and inventory holding period of 95 days, as opposed to the peer median of 158 days net operating cycle and 137 days inventory turnover. This demonstrates BAX’s efficiency in generating additional sales, whilst keeping purveyors happy, enabling more relaxed terms of payment and purchase. This is advantageous for the company in the current climate and shows a higher comparative advantage over operations.

Data Source: Author

Return on Capital

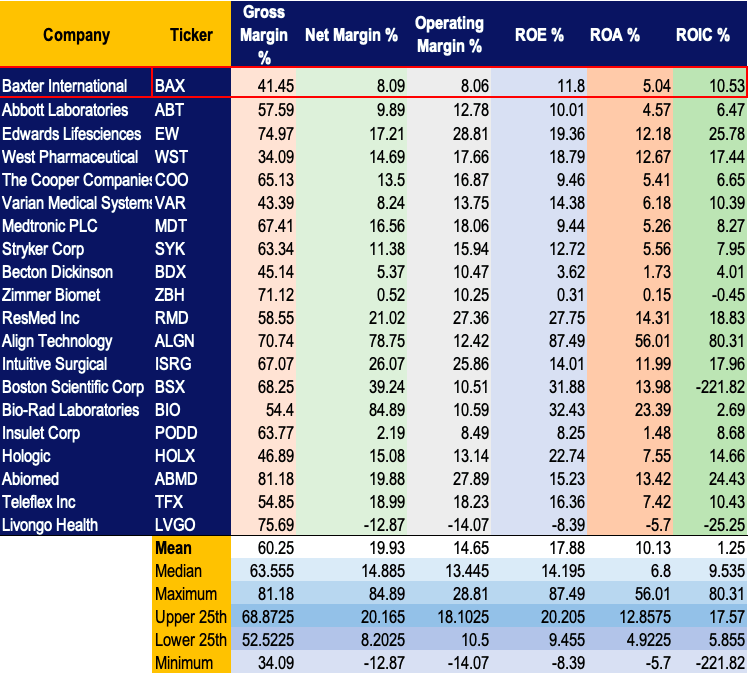

Baxter has shown additional strength in performance through garnering satisfactory returns on invested capital and with solid return over the asset base. We seek companies who elicit greater than 5% ROIC and ROA, thus BAX has scored well here, with 10.53% ROIC and just over 5% in return on the asset base. This sentiment is boosted by the fact that the company is generating ~65 cents for every dollar invested in the asset base, which we deem as exceptionally high and further evidences management’s effectiveness in decision making to generate additional returns and value to shareholders. We see growth of ROCE from 3 years prior as well with the company generating 12.5% in return over employed capital, up around 9.6% from 3 years prior. We are firm in the belief that entities whom can evidence ongoing growth in return on invested capital and capital employed are ubiquitous with increases in valuation over time. BAX certainly scores well here, and we see this evidenced in the tabulation outlined below. Additionally, in relation to the comparables examined in this report, we see ROIC above the median figure, which we are equally as satisfied with, as the ~10% figure is sustainable whilst also offering wiggle room for growth coming into the future. Edwards Lifesciences (EW), for instance, demonstrates exceptionally high ROIC, but we question if this is sustainable and the capacity for growth in this figure over time, to draw example. Again, we are interested in companies which can elicit growth in these figures moving forward, alongside a number greater than 5%. Align Technology (ALGN) has shone in this regard, but again, we question the sustainability for growth in this measurement, so we are more content with BAX’s 10.53% ROIC to deliver the growth we seek here.

Data Source: Author

We would however like to see net margins improve from the current figure, particularly in relation to the entities on this list. We would argue that if any drains on liquidity do in fact present themselves over the coming periods, this may place additional margin pressure on the bottom line, which may in turn impact the payout ratio for shareholders. We are keeping a close eye on the company’s moves here, particularly in relation to tax payable, to observe how the company might be using the available tax shield to their advantage and if this may be impacting net margins, as well.

Dividend Coverage and Solvency

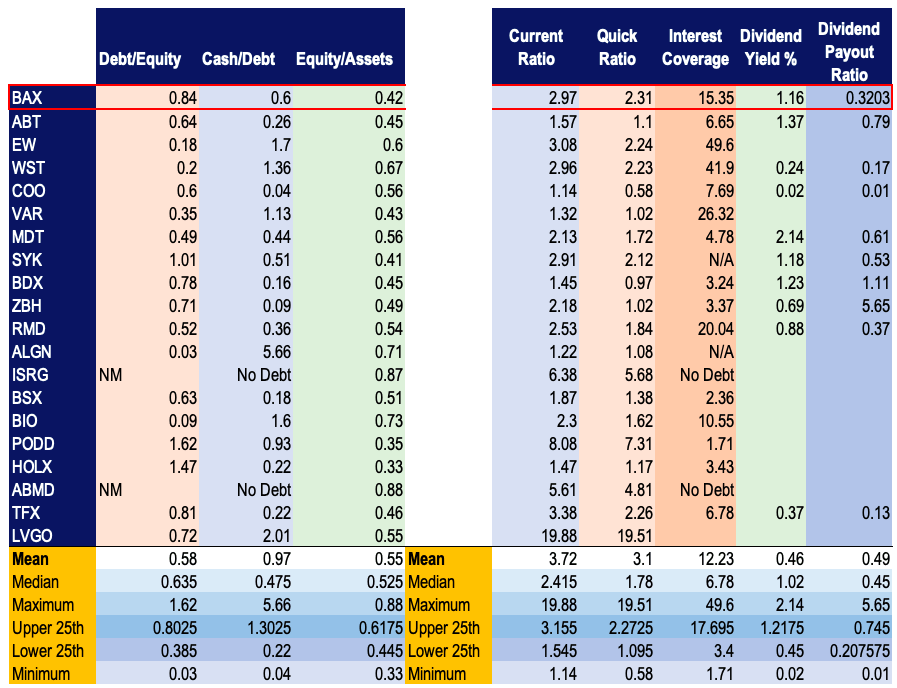

BAX exited the quarter with $4.85 billion in cash and equivalents plus marketable securities, thus is well capitalised heading into the remainder of FY 2020. On a short-term solvency basis, short-term obligations have 2.97x coverage, and the management have opted to carry higher levels of inventory to ensure ongoing product availability, prior to hurricane season and to sustain sales through the uncertainty in demand surrounding the pandemic. Even if inventory is unable to be sold quickly, there is 2.31x coverage. Therefore, the company should meet its short-term obligations as they fall due. Management is confident that liquidity preservation measures undertaken are sufficient to fund ongoing operations and to execute capital expenditures required to fulfil growth expectations.

Management has been proactive in remaining competent over debt, reducing the debt/equity figure from 139% to around 84% over the previous 5 years, a 61.44% decrease, or around 12% each year. The total debt figure is well covered by OCF at ~33x coverage, and with growth in OCF expected over the coming periods, the company has greater access to liquidity preservation measures via its debt issuances this year. The interest expense has increased from these issuances and also over long-term debt. However, it remains well covered at 15.35x the TTM EBIT total, evidencing management’s competency in managing the increased debt levels and providing additional liquidity preservation measures to prevent value erosion. The company also has $2.69 in FCF per share, further signalling the company’s propensity to pay its debt obligations moving forward.

NOTE: Click image for larger view

Data Source: Author

Dividends remain well covered at 1.88x net income and 3.52x from FCF, therefore illustrating the company’s ability to continue dividend growth and deliver value to shareholders. The payout ratio of 32% is sustainable and allows room for growth with earnings expansion. We firmly believe that the company will continue to reward shareholders through ongoing dividend growth, and that this will reflect in the share price, particularly as investors fly to quality and seek resilient companies with strength on the balance sheet with evidenced capacity to continue revenue growth in the midst of the pandemic. The fact BAX has kept its dividend and committed to growth signals to investors that this is a company which has the legs for the long-run, which is why we advocate investors to consider this time horizon when entering a position for this company’s stock.

Valuation

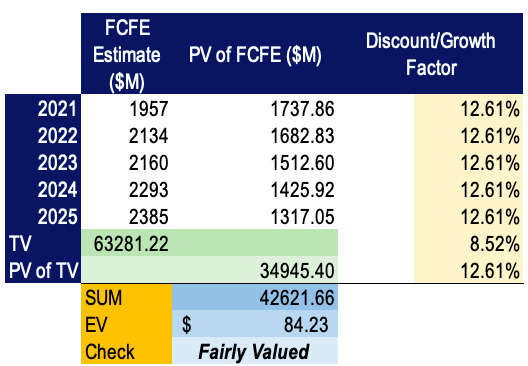

To value BAX at today’s market price, we have completed a number of analyses to gain insight into the right valuation for the company, starting with a DCF analysis over FCFE; figures we have obtained performing linear regression over the consensus of analyst estimates. We are accustomed to using the PRAT model of DuPont to assign a terminal growth rate based on the sustainable growth rate of the company’s FCF earnings; whilst we have utilised the summation of the risk-free rate as the current 10-year treasury yield in addition to the 10-year expected (mean) return of the S&P 500, as an opportunity cost, for the proxy of the discount rate.

Data Source: Author’s Calculations

Using these implied inputs, we have arrived at a figure that shows BAX is fairly valued at today’s trading price, which we are in firm belief of the same, based on the plethora of factors outlined in this report already. There is ongoing evidence that the company has the capacity to generate additional growth in share price. Hence, we have performed a sensitivity analysis over our inputs to the FCFE model, to gain insight into the range of possible values in the valuation that can be obtained. We believe that BAX is likely to follow our blue-sky scenario and continue growth over FCF and, therefore, assign a target price of $90.16 over the coming year from our analysis alongside the growth prospects of the company in this time period.

Blue-sky scenario in green, grey-sky in salmon, base case in blue. Our DCF target price is $90.16:

Data Source: Author’s Calculations

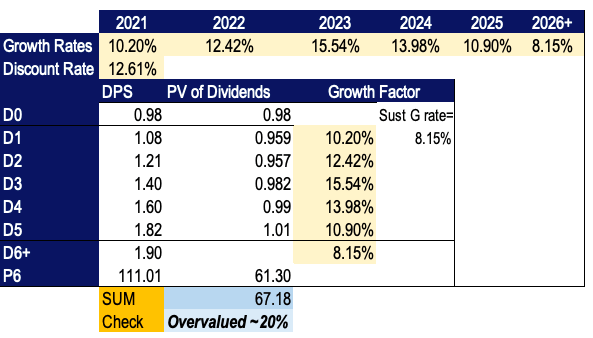

Considering the company’s history in ongoing dividend payments, we feel it fit to bolster the valuation by performing a 2-stage DDM valuation. Using our inputs, we foresee 3 years of accelerated growth in dividends based on recent dividend increases, afterwards reverting back towards the sustainable dividend growth rate. As such, we have assigned a terminal dividend growth rate of 8.15%, which was obtained from this sustainable growth rate examination. We feel the company is able to support dividend growth at this rate in the long term at a minimum, based on the super-nominal growth of ~18% we have seen in dividends over the previous 4 years. In our analysis, we observe the stock as potentially overvalued by approximately 20% in the base case. However, in our blue-sky scenario, we see our target price of $90 arise again, which we are confident the company can reach if continuing along the current trajectory of dividend growth.

Data Source: Author’s Calculations

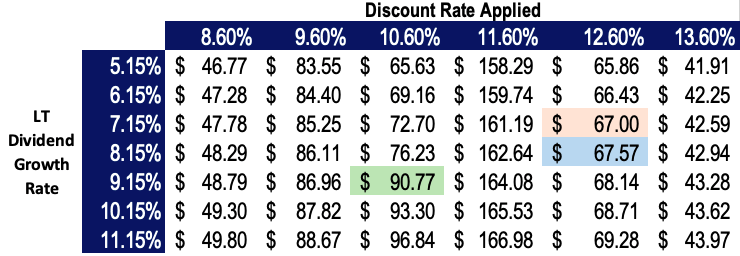

Our DDM price target in the blue-sky scenario is $90.77. We are confident the company can continue to grow dividends at the upside rate.

Data Source: Author’s Calculations

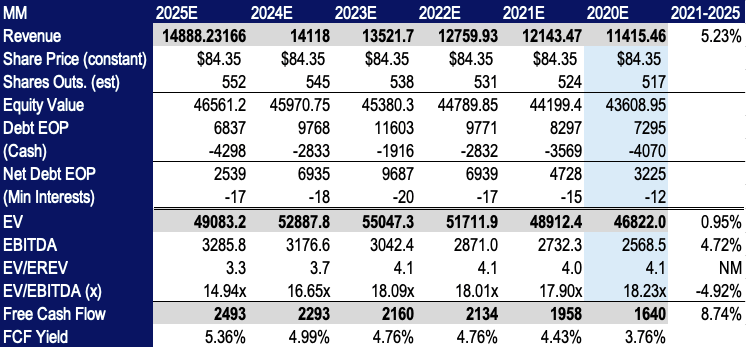

Additionally, we foresee that the company has the capacity to retain a competitive valuation from a ratio analysis front, whereby, based on our assumptions, the EV/EBITDA multiple will likely remain low within the list of comparables we have analysed for this report, falling in line with the fair or undervalued status we place on the company today. We foresee EV/EBITDA and EV/REV decreasing over time, as the company expands revenues and reduces speculated debt totals. In light of estimated FCF growth, there is a likely increase in FCF yield over this period, again favourable for dividend players and value investors alike moving forward. We are confident with our estimates, which we have obtained by performing linear regression over the consensus of analyst estimates alongside our own calculations.

Data Source: Author’s Calculations

Based on the figures above, we feel fwd EV/EBITDA and EV/REV estimates are correct on current figures, based on the spread of comparables examined below, alongside other metrics to support the upside case.

Data: Author

On a Price/FCF front, we are satisfied with the figure as BAX lies within the lower quartile of the comparables listed and is also below the median figure of the group. We seek companies which are in these categories on examination, and we feel that the P/FCF signals value to investors based on this. Additionally, we look to the Price/Book figure to signal value creation for shareholders in addition to a valuation metric, where we believe a score above 1 signals value creation for shareholders above and beyond book value. We see BAX’s score of 5.59 as evidence of the same, and we are pleased to observe the score is below the median of the peer group, signalling value. The company’s P/E is high, which we agree with, based on the market’s expectations of the company moving out of 2020, where it lies exactly as the median figure of the peer group. We see this as satisfactory for an expectation of performance by the market. Undoubtedly, you get what you pay for in equities, evidenced by this comparables analysis.

Additional Growth Catalysts

The company has been busy with acquisition activity over this period. In February, BAX acquired the rights to the Seprafilm Adhesion Barrier product, known simply as Seprafilm. The company paid around $340 million in cash for the rights to the assets and the product line. Seprafilm is used for administration in patients who undergo abdominal or pelvic laparotomy procedures, indicated to reduce the prevalence and incidence of postoperative lesions and adhesions in the abdominal wall and viscera, particularly the omentum, mediastinum, small intestine, bladder and stomach. The indication extends also to preventing adhesions following pelvic laparotomy in the uterine and ovarial anatomy, alongside the large intestine and surrounding structures.

As the economy slowly reopens, so too shall the utilisation of hospital admissions and home-care visit scenarios. There will be a surge of growth in sales and recurring revenue streams for BAX based on their equipment placement model. In their renal segment, the company has planned launch of the dialysis unit known as Kaguya, for the under-utilised peritoneal dialysis market of Japan. Kaguya is a newly innovated peritoneal dialysis system that allows greater user interaction and is combined with Sharesource, to deliver a patient experience that is superior to other providers, by sharing test results to doctors in real time. Already, Kaguya is in use in around 40,000 individuals in Japan, with growth in patient uptake expected as the product rolls out to major medical and health centres, which will continue to adopt the technology secondary to its simplicity and efficacy in delivering test and treatment results in real time, from people’s homes. The same placement model is in place here, with a subscription payment and ongoing revenues obtained from additional consumables required for operation of the unit.

Risks

The risks in our view are mainly geared towards the company, which may in turn roll on to impact shareholders. Management has estimated around $180 million in downside to revenue from the exit of Q2, with lower than expected sales guidance for the remainder of the year. Additionally, an additional $150 million in costs are expected for absorption, following an increase in supply chain expenses and measures related to COVID-19 protection for staff. These are very damp risks in perspective, as the supply chain costs were increased to prioritise delivery of systems and continue to supply critical care products to patients in need.

Additionally, the company will face risks if the pandemic continues longer than planned, or if there is the continuation of the so called “second-wave” of the coronavirus. This will undoubtedly hurt the majority of entities as well. However, the risks here are offset by Baxter’s non-reliance on elective procedures and key differentiators in their critical care markets. Where Baxter will see most pain is in the advanced surgical segment, particularly in their anaesthetics market, as surgical interventions will likely remain low as long as there are governmental restrictions from the coronavirus and front-line personnel are redirected towards maintaining control on transmission rates and treatments associated with COVID-19. Apart from these visible market risks, we don’t have any other major indicators of risks to the company, as they are well capitalised, have no foreseeable drains on liquidity, have access to sufficient liquidity sources, debt and interest is well covered, and perhaps most importantly, the company has committed to ongoing dividend payments, which, for shareholders will make the stock attractive moving forward.

Conclusion

We hold a bullish long-term outlook for Baxter for the reasons outlined in this report. Bastion-like fundamentals, coupled with ongoing evidence of value creation for shareholders, position BAX towards the head of the bull. With little foreseeable risks and commitment to dividend increases into the future, the stock becomes an attractive play for both income-style and value players. As investors fly to quality in the current economic climate, the key differentiators that position Baxter in the crown position in many of its existing markets mean that the company will continue to flourish and keep on chugging away bit by bit, whereas shareholders can enjoy the ride. We set a price target of $90 over the next 1-year period, and we firmly believe that market expectations will prevail, and there is a high probability that the stock will reach its target price in time to come.

Disclosure: I am/we are long BAX. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}