{kind=link}

Overview

Aquestive Therapeutics (NASDAQ:AQST) has posted Q2 results beating the street by $0.36 in EPS and $12.91 million in revenues, on the back of a sturdy quarter related to sales of its licensed commercialised pharmaceutical products, including Sympazan, Suboxone, Kynmobi and Zuplenz. Sympazan is an oral film of which the active ingredient is used in the management of seizures; whilst Zuplenz is the marketed brand for the compound Ondansetron and is the gold standard in anti-nausea medication, whilst Suboxone is an opioid-based drug for pain-relief. The company has exclusivity over these compounds and Sympazan is proprietary to AQST.

Data by YCharts

Data by YCharts

Revenues over the previous periods to date have been generated on the back of purchase orders of these compounds made via licensees, in addition to the manufacturing and supply & co-development of other active compounds. The firm also generates revenues from research fees and royalty income derived from proprietary ownership over the compounds and of course through sales and agreements with licensees on this basis.

Profitability

Total revenues on the exit of Q2 were $21.7 million, up 95% from the previous quarter, on a net loss of -$2.33 million or -7.0 cents a share. Gross revenues were obtained on a margin of 57.90%, but the net margin blew out to -134% following the loss. Compared to the same period in 2019, revenues grew by 144% whilst the net loss was ~$18 million less over the same term, which is pleasing considering the current climate. The increases were partially a mirror of the carry-over from license fees and royalties that were received on the back of the Kynmobi approval, which is indicated in the use of Parkinson’s patients as a dopamine agonist to alleviate motor-function related symptomology. Income received from licensees and royalty payments for this compound amounted to $12.5 million during the quarter. Furthermore, Sympazan generated around 60% in YoY sales growth which also drove the change in net loss over the single-year period, alongside a reduction in R&D expenditure and general COGS. EBITDA totals reached $2.9 million in this period, in stark contrast to the ~$16 million loss in the previous term, on the back of the sales growth mentioned above.

Data Source: Market Data; Author’s Calculations

Of the changes in revenue, there was a 19% reduction in manufacturing and supply revenue, assigned due to lower sales volume of Suboxone, which may continue along this trajectory considering shifting attitudes amongst professionals regarding opioid-based interventions. Furthermore, the presence of many generic substitutes in this category signifies this likely downfall, thus impacting demand for the brand itself. Additionally, operating costs decreased by around 35% on the back of reduction in volume of this product.

Moreover, R&D expenditure was down almost 54%, following a reduction in clinical trials from the Covid-19 pandemic, which has ultimately impacted the company’s pipeline of developing new compounds this year. SG&A costs were also lower by 14% and the company attributes this to less cash allocated towards marketing and factory overheads.

Solvency

Interest expenses increased 42% and are not well covered at only 0.14x coverage. This is alarming as the company also is required to fulfil primary claims after issuance of a $70 million principal in senior secured notes issued in July last year at a fixed coupon of 12.5%, which is high in comparison to other issuances by similar entities. Edwards Lifesciences’ (EW) senior notes are fixed at 4.333%, for instance. Although the fixed coupon on the senior notes reduces market risk, the overall interest expense including capital leases and LT debt increased drastically, and is therefore an essential factor for the company to consider in remaining solvent whilst fulfilling its obligations to primary claimants. The indenture also allows an additional $100 million in further issues if required, giving another arm of liquidity to the company.

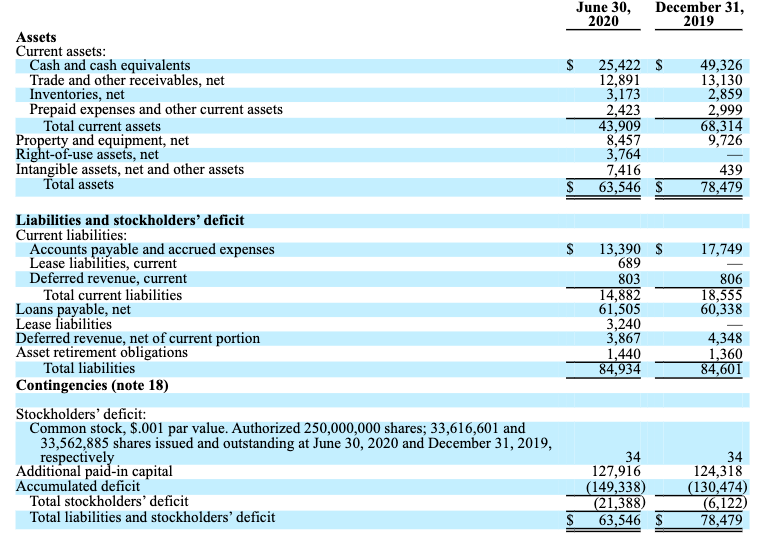

Exiting Q2, the company has cash and cash equivalents of $25.4 million. But long-term debt/total capitalisation is at 145%, indicating the company is highly leveraged and investors must be careful considering the net loss posted this quarter alongside poor interest coverage moving forward. From a short-term perspective, the company should meet its obligations in the immediate term with a current ratio of 3.33x coverage over short-term liabilities. Inventories have been well managed over years showing a decrease in recent times. Thus, if the company were to quickly sell its inventory, the quick ratio shows coverage of 2.93x which is favourable in the short term.

Moreover, debt/FCF is a negative score following the company’s FCF-negative position of -$35 million at -1.74. Thus, any chance at accelerating its obligations over the debt facilities is unviable by this analysis. FCF has also been poorly managed over the previous 5-year period, in deficit since 2018 on TTM figures. Further sales growth of the hero products is needed to accommodate for the unpleasing scores in this light, particularly to bolster FCF to prop the company’s position in weathering the pandemic. The company also has $1.06 in cash per share, reflecting the negative score in EPS over this period.

Data Source: AQST 10-Q June 2020

Additionally, ROA has been poor at -105% alongside ROCE which is surprisingly low at -78% over the TTM; however, these points are offset by the fact that assets are turning over around 74 cents for every dollar invested. We consider this metric to be high for the company and are satisfied to see this, and thus predict ROA and ROCE to correct in line with the asset turnover coming out of the pandemic. The company has also invested an additional 35.75% in NWC YoY and we will be anticipating growth in ROA and ROCE from ongoing capital expenditures following the same, particularly as volume is likely to expand in its existing markets on the back of the economy reopening and increases in medical consumption from the same.

Forward Estimates

From the company’s end, guidance for the remainder of the year indicates that revenues are expected to reach a range of $35-45 million in the next periods, on expanding margins of around 70-75%. Cash burn to the end of the year is foreseen at $45-50 million or around $9-10 million each month leading up to December, which is anticipated to amount to an EBITDA loss of around $50 million over this same period.

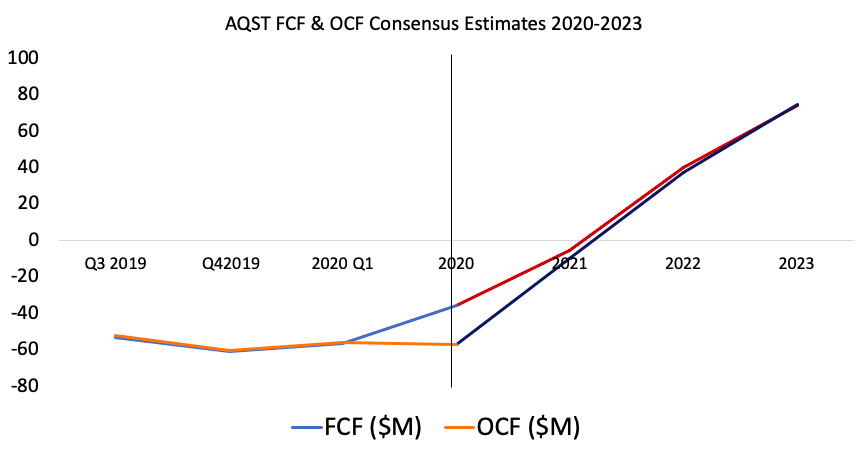

Analysts seem to confer on the above, based on figures we have arrived at performing linear regression over the consensus analysts’ estimates for the 2020 outlook and beyond. Moving out of 2020, revenues are forecast to climb at a CAGR of 57.79% from 2020-2023 reaching a total of $237.4 million by the end of that period, using the same method of approximation. FCF seems to be at the upswing of the j-curve and is forecasted for profitability by 2022 (using the same method). OCF will likely follow suit at the same period, considering its correlation to FCF over the periods to date.

Data Source: Author’s Calculations

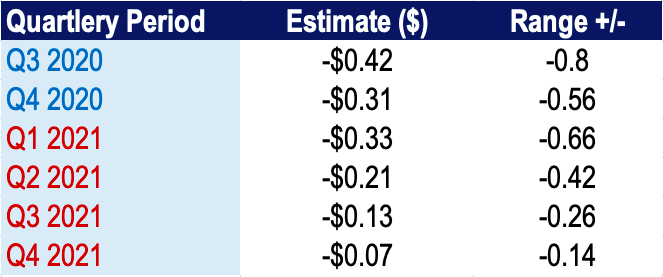

EPS estimates are likely to remain within the negatives over the next single-year period and although the company has beaten the street on EPS, the previous two quarters were a miss to highlight potential uncertainty over this measure.

Data Source: Seeking Alpha; Author’s Tabulation

Valuation

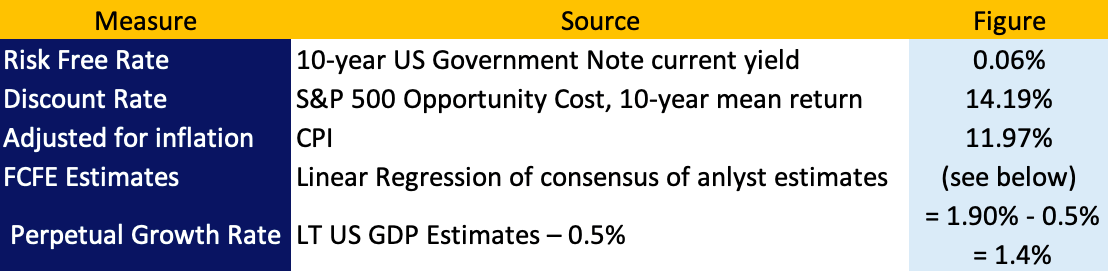

We have built an FCFE valuation to the stock price to gain an estimate of the fair value. As we see uncertainty from the company in terms of historical growth and projected growth into the future, we have limited forecasting risk by analysing estimates over the coming 5-year period only, obtained from performing linear regression over the consensus of analyst estimates. To achieve this, we have assigned a terminal growth rate related to the long-term US GDP forward estimates, as the company is currently unprofitable and thus, a sustainable growth rate is difficult to accurately assess in order to obtain a terminal value in year 5. We have also utilised the opportunity cost of holding the S&P 500 using the 10-year mean return for the equity proxy over the S&P equity premium due to uncertainty in the accuracy of that figure right now.

Data Source: Author’s Calculations

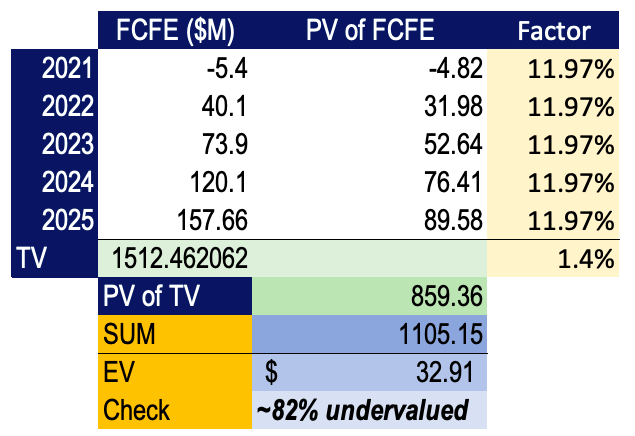

From our estimate of intrinsic value, we believe the stock may be currently undervalued by around 80%. This is not out of line with other analysts’ estimates for intrinsic value. We would take this number with caution, however, as the company has delivered low ROCE and ROA which we firmly believe will impact the share price and valuation. We, therefore, intend to review the figure on a regular basis to observe how the stock price will be affected by the recent earnings call and market sentiments regarding the Covid-19 situation. We do not feel this is an accurate price target at this point, so we are not advocating for this figure in that regard, only as a measure of intrinsic value.

As the company is presently unprofitable, P/Sales is a better metric to compare ratios on. Outcomes obtained from P/Sales suggest the company is at a reasonable value at 3.10, below the sector median of 6.85 and also below comparable entity Liquidia Technologies (LQDA) at 15.21, but above Bionano Genomics (BNGO), who scored 1.76 on our assessment. We also checked EV/Sales because we feel it was essential to factor in the company’s leverage coming out of 2020. On our examination, AQST performs well, scoring 4.39 which is below the median for the industry figure of 7.4 and well under LQDA at 15.21 and BNGO who posted an EV/Sales figure of 7.88 most recently. Thus, we feel the company may be undervalued; however, we will be scrutinising the available data regularly to gain a better insight over the next few months as we want to observe how the debt and revenue figures pan out over the next 1-3 months at least.

Risks

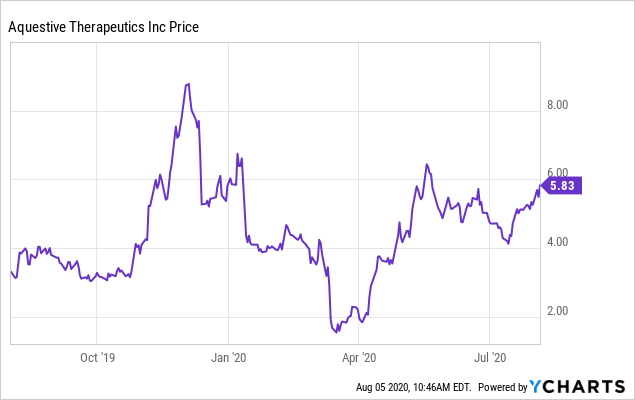

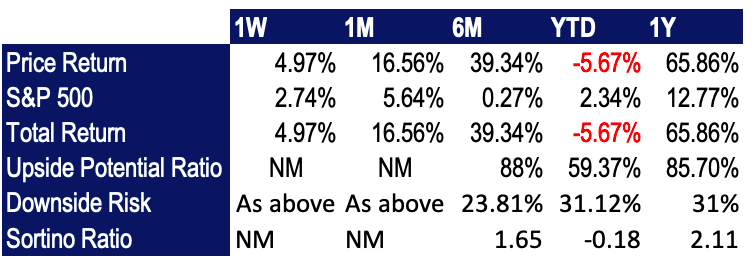

Risks to shareholders on a price perspective lie in the fact that historically, over the previous singe-year period and YTD, investors have not necessarily been rewarded for exposure to the additional downside risk in price returns, evidenced in a 6-month Sortino ratio of 1.65 to demonstrate. This, however, is offset by the fact that the stock has delivered 65.86% over 1 year and 39.34% over the 6 months to date, albeit with high risk to the downside. The volatility is evident in comparing the upside to the downside potential, where downside risk is around 60% as a function of the upside ratio. Furthermore, whilst investors will be pleased with the company beating the street most recently from its Q2 results, further growth is needed over the coming periods for the company to continue to deliver on the market’s expectations.

The company also faces risks related to the Covid-19 pandemic, as sales for key product domains have fallen drastically, partially due to the fact that all elective medical and surgical procedures have been put on hold to free up human capital to fight the coronavirus. Undoubtedly, there are impacts to the company here which relies on these procedures in its opioid and anti-nausea markets. Aged care facilities are also a large domain in this regard for the company, and there is lack of visibility on guidance into expectations for the aged care sector coming out of Q2, thus sales forecasts are unclear here also.

We would also argue that the company’s interest coverage is not well displayed at only 0.14x coverage, alongside expanding LT debt levels which require ongoing cover as the company intends to move towards profitability. The entity’s senior notes pay a fixed coupon of 12.5%, which we feel is high in comparison to other indentures that are in circulation at this point. So evidence of debt management is required in order to make an informed decision prior to an entry point.

Conclusion

A sturdy Q2 in beating expectations whilst benefiting from sales growth in its existing markets demonstrates the trajectory AQST is on moving into the remainder of 2020. We would advocate that investors should continue to monitor the company’s return on capital to realise management’s growth strategy alongside the debt management plan. If FCF estimates are to pan out, the company will be profitable by 2022 which we foresee as likely to occur on the back of its recent performance, should it continue. We are, therefore, bullish on AQST. But we will wait for the evidence of appropriate fundamental and price momentum to make the case for an entry point, whereas for now we are happy to sit on the sidelines and enjoy the AQST journey as it pans out during the course of the pandemic.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.