Macquarie Infrastructure Corporation (MIC) have recently posted results from the Q2 exit and have missed estimates of EPS by $0.05 and revenue expectations by 14.2%. Earlier this year, the company slashed dividend payments to shareholders in order to preserve liquidity and prevent value erosion on the back of the economic fallout from COVID-19 around the globe. Most recently, their existing Atlantic Aviation (AA) and Hawaii Gas (HG) markets have shown a slowdown in cash generation on the back of significant reductions in air passenger traffic, stay at home orders and overall contraction in tourism supply for Hawaii specifically, resulting in a contraction of demand for Hawaii Gas resources by the end-users. Whilst air passenger traffic has shown glimpses of a rebound during the exit of Q2, the restrictions on tourism continues to limit gas sales in Hawaii whilst reducing demand for AA’s ground staff moving out of this period.

Such impacts were partially offset by favorable results from the company’s International-Matex Tank Terminal (IMTT) arm, as the reduction in demand of petroleum products alongside the reduction in consumer consumption globally has shown an inverse-like increase in demand for storage of these resources. Consequently, IMTT showed a satisfactory improvement in performance for this section of MIC’s portfolio.

To demonstrate, the profitability of IMTT is propelled by the total capacity of liquid storage the entity has under lease agreements, alongside the yields on storage for those particular contracts. In Q2 2020, utilization of storage capacity at IMTT sites reached 94.6%, well above the 82.9% in the corresponding period in 2019. The resultant increases in these utilization rates for storage capacity ultimately is a reflection of the contango within petroleum markets where spot price for oil and petroleum has traded lower than the futures contracts closing out in Q2 2020 and beyond. Utilization is anticipated to remain above 90% for the remainder of 2020 on the back of the economic uncertainty in the evolving COVID-19 situation. In contrast to IMTT, for AA and HG, these markets are primarily driven by consumer preferences in addition to government legislature in the current times, thus guidance for these sections within the portfolio is unclear for the remainder of the year, much like many other players within the same domain.

It was noted however that the overall demand for aviation services in the US has shown promising signs of an earlier than expected rebound. For instance, the Federal Aviation Administration have recently commented that flight activity within the US domestically was around 82% of total levels in June last year, which also signifies an increase of 28% since the market turmoil in April. Consequently, AA has evidenced capacity for upheaval as the company reported that demand for AA’s services increased markedly on the back of this significant increase in air passenger traffic at US domestic airports where AA’s ground staff operate. In spite of this, the uncertainty over these key operating areas means the return of dividend payouts to shareholders is questionable at this point, especially in light of the company’s choice to withhold earnings for ongoing capital expenditures alongside preparation for large, one-off items that may impact the income statement coming out of 2020 and into 2021.

Solvency & Liquidity

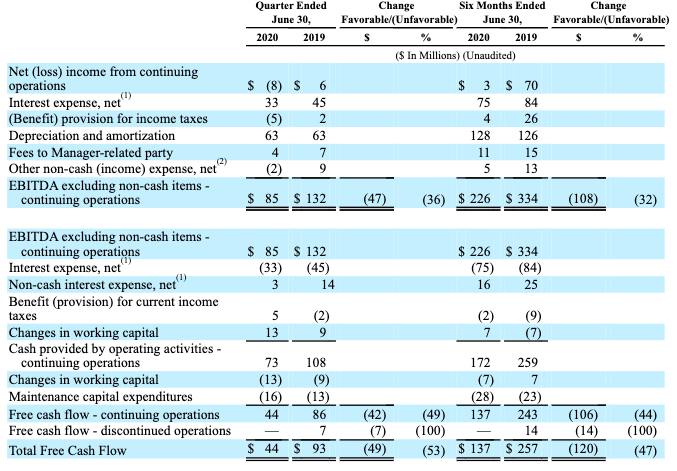

As of 30th June, total debt outstanding for the company was $3.315 billion, which includes access to their senior revolving credit facility. The accessible liquidity from this facility totals $661 million as of the same date. Back in March, the company had mentioned it aimed to keep leverage under 4.5x EBITDA totals which it has partially recognized with current totals at 4.8x EBITDA, on the back of a reduction of earnings and expansion of debt facilities required for additional liquidity during this period. To illustrate, prior to Q2, MIC drew down on $874 million on two of its revolving credit facilities. The spread was comprised of $600 million for the holding company and an additional $274 million for AA. Subsequently, the AA facility was eventually repaid in April and the company has no substantial near-term maturities on its convertible senior notes, which pay a coupon of 2.00% semiannually. These facts evidence competency from management in reaching their objectives.

NOTE: Click on image for larger view

Data Source: MIC 10-Q June 2020

The company also reports a cash balance of ~$875 million and corresponding quarterly FCF of $44 million from the Q2 exit, which gives a TTM FCF figure of $475.81 million. This is also on the back of a healthy FCF margin of 28.65%. However, this number is 91% below the 2019 Q2 FCF figure, majorly attributable to reduced contributions from AA and the Hawaii Gas terminal. In light of this MIC has managed to elicit profitability after meeting its obligations over the previous 2-year period whilst demonstrating a 9.8% increase in TTM FCF values over the same period. Consequently, the company registers a Debt/FCF measure of 6.84 which we would consider sound and evidences that the company would be able to accelerate its debt obligations if need be, albeit highly unlikely considering the current situation. Furthermore, the company’s long-term debt accounts for around 53.95% of total capitalization which we feel does not constitute as financing risk, particularly as operations open up coming out of the pandemic.

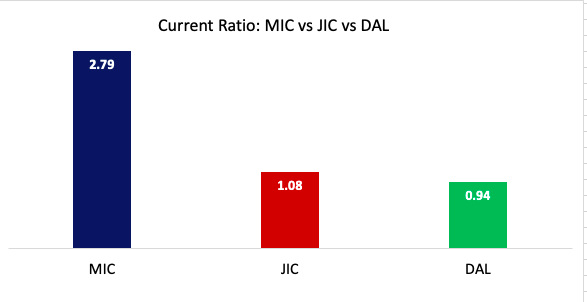

On a short-term solvency basis, MIC should be able to meet its obligations in the immediate to medium horizon with coverage of 2.79x from cash (and equivalents) alongside current assets as reported most recently. A ratio of 1 or above we deem satisfactory, particularly in those entities who have large ongoing capital leases with unavoidable CAPEX requirements, such as in the case of MIC. In relation to comparables Johnson Controls International (JCI) who show a current ratio of 1.08x and Delta Air Lines (DAL) with 0.94x, the company is better situated here. Furthermore, MIC has $13.31 in cash per share, which further illustrates that there is enough cushion in the event of further unprecedented market tribulations. Interest coverage remains well splayed at 1.42x quarterly contributions and 1.47x and the company most recently hinted lower unrealized losses on interest rate hedges following record low interest rates on commercial loans this year.

Data Source: Author’s Calculations

MIC intends to use the available cash on hand alongside its available revolving facilities to fund operations and additional capital works throughout the remainder of 2020, however, if current trends continue then the target of containing leverage to 4.5x of EBITDA may become unfeasible on the back of said works. For instance, the revolving credit facilities are used at both IMTT and HG as a measure of liquidity preservation, ultimately to manage interest payments and fund ongoing capital projects. In total, the company reports $1.54 billion in available liquidity on hand, including $275 million in cash allocated specifically to fund additional works at IMTT and HG. Of concern however is the uncertainty surrounding additional lockdown measures secondary to COVID-19, which will reduce the visibility on MIC’s ability to meet its objective on these projects. In other words, there may not be enough available liquidity to continue as planned.

Furthermore, in particular, operating costs have increased on the back of COVID-19 related issues, in the form of increased labor presence at terminals, cleaning and hygienic protocols and implementing additional pandemic related plans, to name a few. Whilst the increases are relatively small, they are also partially offset by a contraction in operating costs from reduced operations, resulting from COVID-19 as well.

Profitability

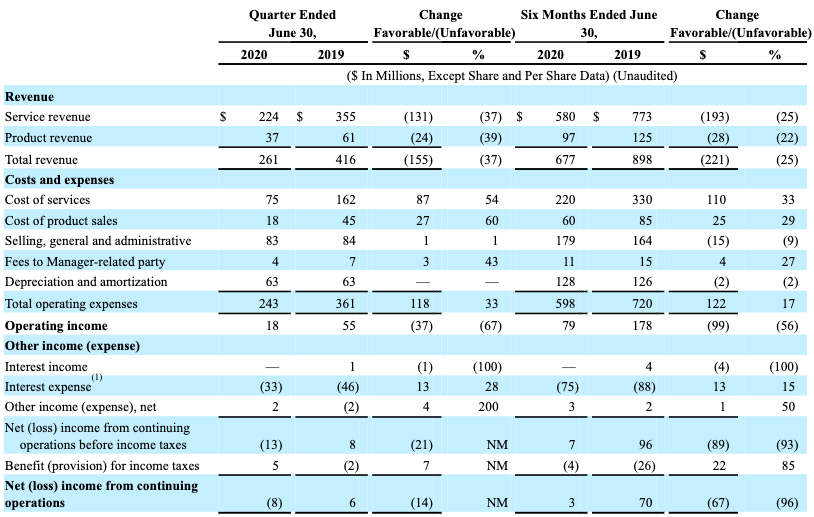

The company has experienced an upset in revenues missing estimates by $35.7 million and posting a net loss of -$8 million from continuing operations in Q2. TTM gross revenues were down -37.25% from the March quarter and surmounted to $261 million on a gross margin of 52%, which the company enjoys from its IMTT, AA and HG markets combined.

NOTE: Click on image for larger view.

Data Source: MIC 10-Q June 2020

MIC most recently elicited a meager 2.3% ROCE which is also down from 4.41% 3 years ago. This was coupled with ROA of only 1.84% for the quarter and 2.7% for the trailing twelve months, around a -36% decrease over the 3-year period to date. The company’s assets are only generating around 22 cents for every dollar invested in the asset base, which needs to show strength in order for the company to remain profitable and meet the capital project outcomes it has outlined. JCI has returned 3.58% on capital employed with around 2% ROA, whilst DAL have performed poorly, generating 1.48% ROCE and -5.06% ROA, to draw examples for MIC.

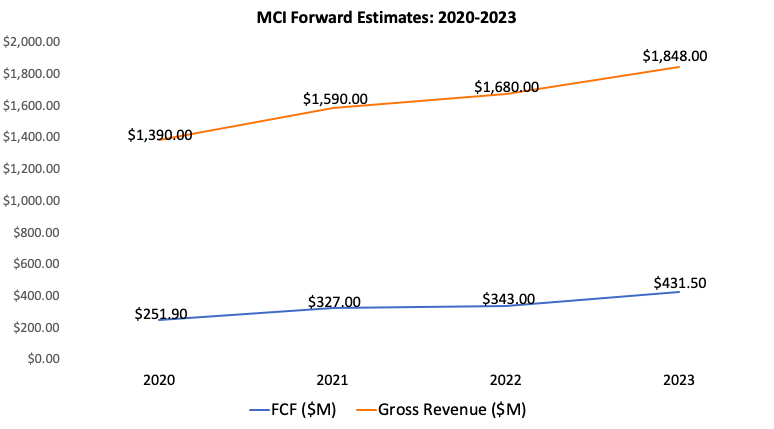

Visibility is unclear for MIC in terms of estimates, secondary to 66% of their portfolio makeup attributed to aviation and tourism. There is no saying when flight activity will return to pre-COVID-19 levels; and there is more uncertainty around the fact that HG relies heavily on purveyors within the hotel and leisure industry in Hawaii and surrounding areas. Thus, the company has not provided clear guidance on these two arms of the portfolio. Performing linear regression on the consensus of analyst estimates, it seems as if gross revenues will continue south for one more period before entering a small parabolic uptrend in the j-curve moving into 2021 and beyond. FCF is poised to follow an upward trajectory using the same approximation method, particularly on the back of the cuts to dividends earlier this year, alongside favorable solvency metrics to support the case.

NOTE: Click on image for larger view.

Data Source: Author’s Calculations; obtained using linear regression from the consensus of analyst estimates.

Valuation

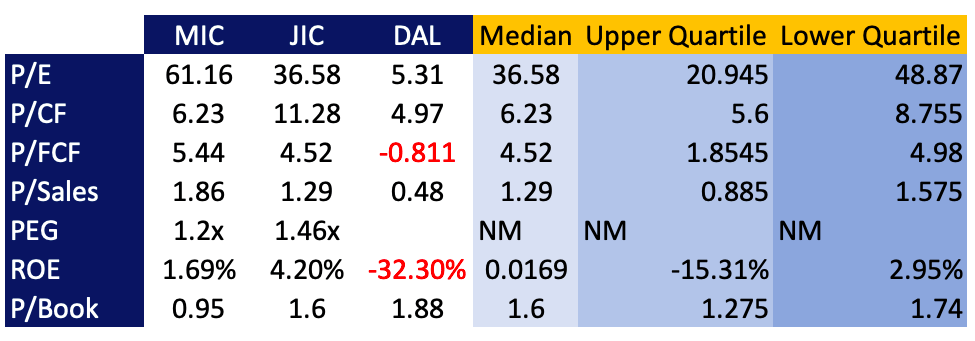

The company trades at a premium with a P/E multiple of 61.16x, well above comparables JCI and DAL and also above the sector median of 22.87x. Furthermore, MIC registers a P/FCF of 5.44 which is above JCI but also emphasizes the company’s ability to generate additional revenues moving out of 2020. On a PEG ratio of 1.2x, this is slightly above the median figure of 1.18. However, the company is better situated here compared to JCI. DAL’s PEG score was not recorded as they are currently not profitable and thus it is hard to estimate PEG for the company.

MIC is also fairly valued on a P/Book front, however, we will continue to monitor this metric as investors do not seem to want to pay above the accounting value of the company’s shares. We also see the P/Book metric as a measure of value creation for shareholders – if it is below 1, then questions arises on whether or not value has been created for shareholders. MIC is around about 1, sitting at 0.95, but we will want to see movement here particularly for any long-term holding scenario.

Data Source: Author’s Calculations

The market has also valued P/Sales for MIC ahead of JCI and DAL at 1.86, so we believe there is an expectation the company will continue to perform, albeit at a reduced capacity from previous times. Charles Lewis Sizemore, CFA, has agreed on this sentiment earlier this year. As well, the above percentile data may be slightly off-put by DAL’s negative metrics recorded from our calculations. Either way, relative to the sector median and in relation to these 2 companies, MIC seems to be trading at a hefty premium from the assumptions of these metrics.

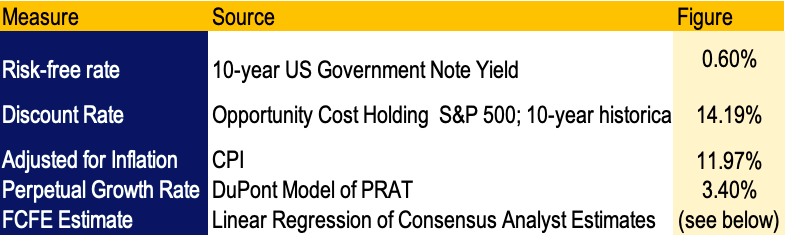

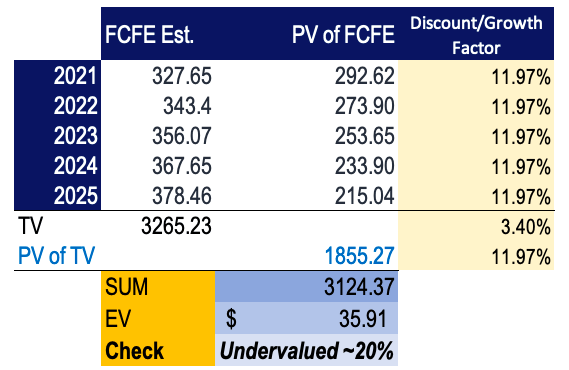

To add weight to the valuation model, we have analyzed FCFE estimates using linear regression of FCFE estimates, obtained from the consensus of analyst expectations. Using the valuation model, we have assigned a perpetual growth rate of 3.40%, obtained from using the PRAT model to identify the sustainable growth rate. We have also opted to use the 10-year historical mean as the opportunity cost instead of the S&P equity risk premium of 6.00%, considering high uncertainty in equities markets at this point.

Using our built-in model, we observe the stock may be undervalued by around 20% on a fair value of $35.91. We will be observing this figure very closely over the coming months to witness how MIC’s share price will fare in response to earnings and ongoing market tribulations, now with many countries experiencing the second wave of COVID-19 – particularly in Australia where Macquarie base is headquartered. We therefore set a price target of $35.91 based on this valuation, and want to see support up to this level in volume and low volatility to the downside.

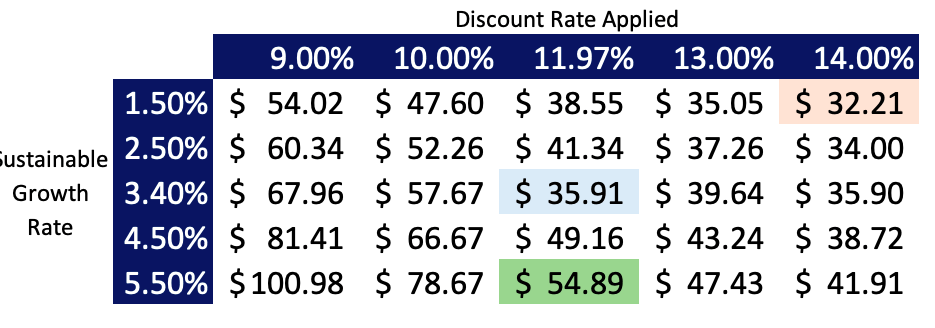

We believe the stock’s undervalued status is correct based on our assumptions, as even if we are wrong in any 2 out of the 3 combinations, it still appears undervalued in a range of $32.41-$54.89, illustrated in the sensitivity analysis over the inputs below.

Therefore, deep-value players should pay close attention to these metrics moving forward, and we will be providing additional coverage coming into Q3 2020 on the same.

Risks

Firstly, around 80% of the revenues given to IMTT are from contractual firm commitments. Any prolonged decrease in consumption and economic activity will have an unfavorable reaction for IMTT’s clients and thus will impact demand for certain products that the business stores on their behalf. Additionally, the company has increased their exposure to finance risks in drawing down repeatedly on their revolving credit facilities. Whilst there is no near-term maturities on debt obligations, the requirement for cash will be large in light of planned works at IMTT and HG alongside uncertainty when a rebound in air passenger traffic will occur, thus reducing AA’s contribution to the revenue stream.

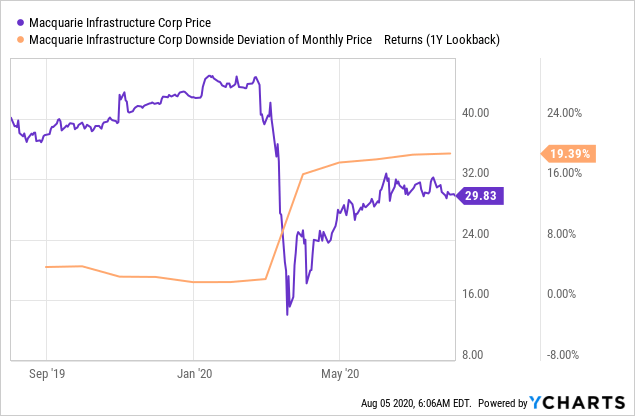

Furthermore, the share price has not shown signs of recovery prior to February highs, trading around -30.5%, down YTD from the previous market high. Moreover, the share price has shown exquisitely high risk towards the downside over the single-year period to date, with 19.4% downside risk on monthly price returns over this term. We have used monthly returns for the scope of medium to long-term investors.

Data by YCharts

Data by YCharts

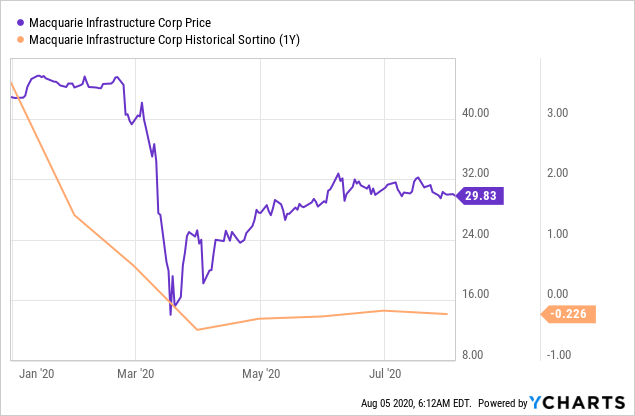

We are dissatisfied with the amount of historical downside risk at play here, moreover with the sortino ratio over the same period which has fallen drastically below zero, indicating investors are certainly not being rewarded for accepting the level of risk at play here. Thus, we would urge potential shareholders to enter with caution, because the downside metrics are biased in the case of MIC’s returns over the 1-year period. We have looked back over the entire single-year period instead of YTD to give a more thorough picture of what was the story pre-COVID-19, however as mentioned, remain unpleased with our analysis here.

Data by YCharts

Data by YCharts

Current and potential shareholders should therefore use this time as a stress-test for the company to identify its resilience in facing out these incredibly uncertain times, particularly in light of the correlation of their portfolio makeup. We certainly don’t see the company being absent from our radar in 5 years’ time, say, as the assets within the pipeline will continue to generate fantastic cash flows, provided we don’t wait too long before the reopening of the global economy. That will be the crux of the so-called test, in fact, to see how the company remains solvent moving out of the pandemic and is able to situate itself ready for a rebound following opening of borders with tourism, fuel use and air traffic.

Conclusion

We hold a neutral stance on MIC as it has demonstrated superior capacity in past market times leading up to 2020. MIC has also remained solvent with a bastion-like mentality from management in ensuring liquidity preservation and value erosion to face out the pandemic this year. Whilst the stock price has tumbled since March and has hardly made a strong recovery case, we see the company’s stance on the aforementioned pointers as strengths in facing out the uncertainty. However, it will ultimately depend on the length of time it takes for the reopening of the economy, most likely in 2021/2022 by all expert estimates. Will the company opt to repay shareholders as previous? It seems unlikely considering covenants placed over its debt facilities and the requirement to retain earnings to bolster cash flow and maintain operations. It is an unfortunate fact, but we can completely understand any decision to withhold dividends from shareholders over the coming years. Long-term players will be watching the company closely therefore.

Thus, as mentioned, shareholders can use this time as a stress-test for the company to observe its resilience and management style, whilst paying attention to the balance sheet to observe a strong turnaround and the stock price moving towards our price target of $35.91, where we would advocate on that momentum the tide will shift to a buy case. We will provide ongoing coverage of the company leading into Q3 2020.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}