By Felipe Bijit

Utilities continue to be a supremely interesting sector. It offers opportunities in diverse exposures across power technologies and geographies, all providing similar resilience to impacts that would result from another set of coronavirus-related lock-downs. This resilience can be a consequence of consumer offsets to reduced commercial activity, with stay at home orders shifting power consumption to homes, or it can come from guaranteed remuneration schemes from governments in regulated utilities.

In the case of EDP (OTCPK:EDPFY), resilience comes from both types of businesses, where EDP operates distribution and transmission assets in Iberia and Brazil as well as manages a leading portfolio of renewable energy assets, earning it the ESG badge. With the recent deal with Engie (OTCPK:ENGIY), whereby EDP will sell a sizable portion of its Iberian Hydro assets, a multiple can be attributed to EDP’s renewable businesses. This confirms to us that this company is not only an ample income provider, but undervalued due to the excessive discount of their regulated utility concessions through the use of regulatory WACCs, and an under-appreciation of the marketability of their renewable asset portfolio. As such, EDP stands as an excellent investment at the intersection of value and income.

Resilience Demonstrated in Q1

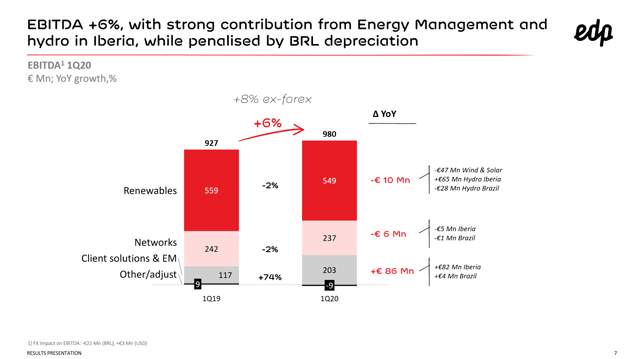

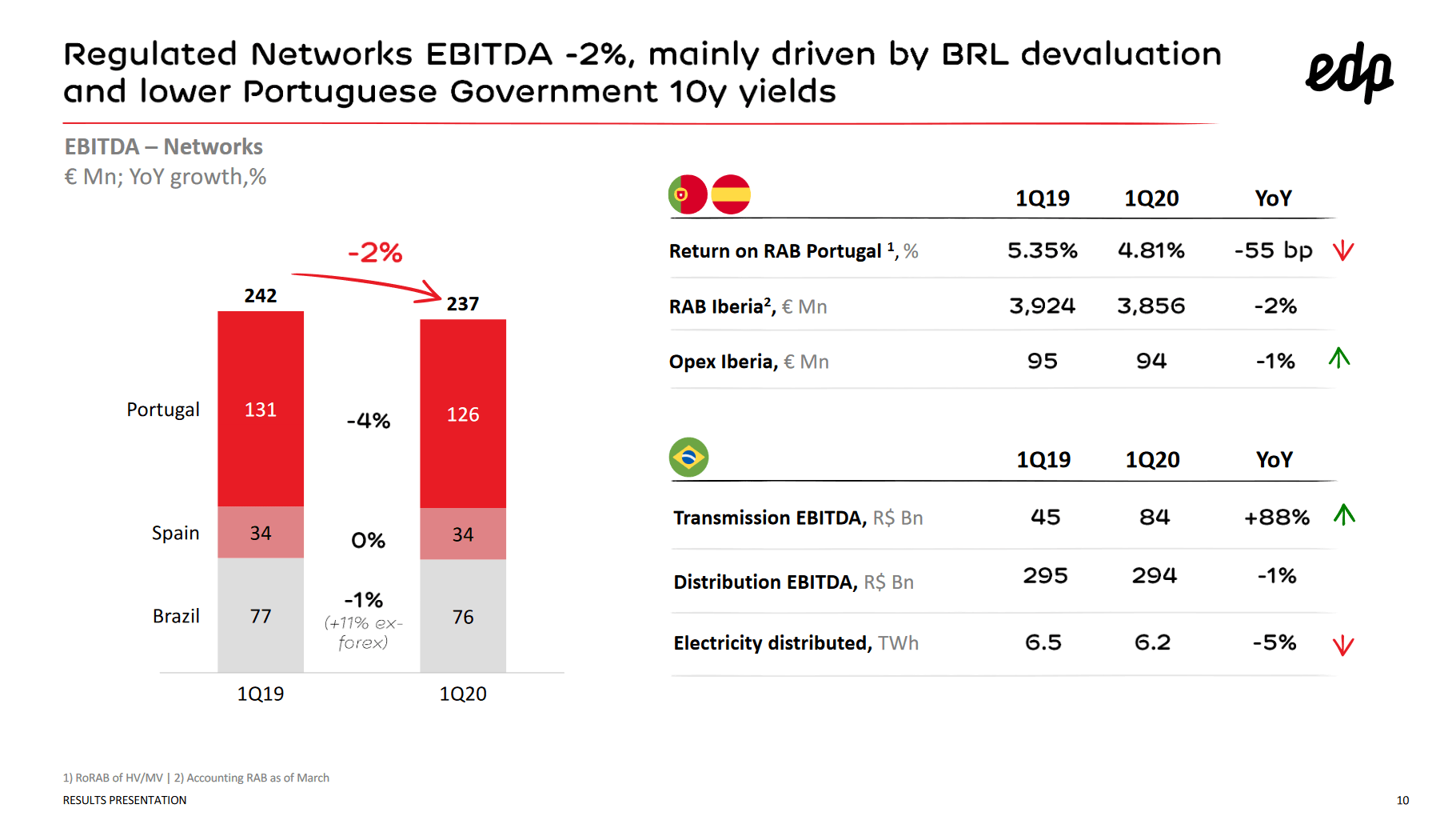

The potential resilience of utility companies in the lock-down environment was rather obvious, regardless of whether the panic selling in March hit them too. Indeed, even their renewable generation business, which is more beholden to free market movements in electricity prices, remained very stable despite the initiation of lock-downs in a large portion of Europe. The shifting of the populace from offices to homes did not have more than a marginal effect on electricity demand. Needless to say, their regulated utility operations for distribution and transmission of electricity under a tariff framework in Brazil and Iberia also held very strong during the period, with the only negative impact coming from FX.

(Source: EDP Q1 2020 Pres)

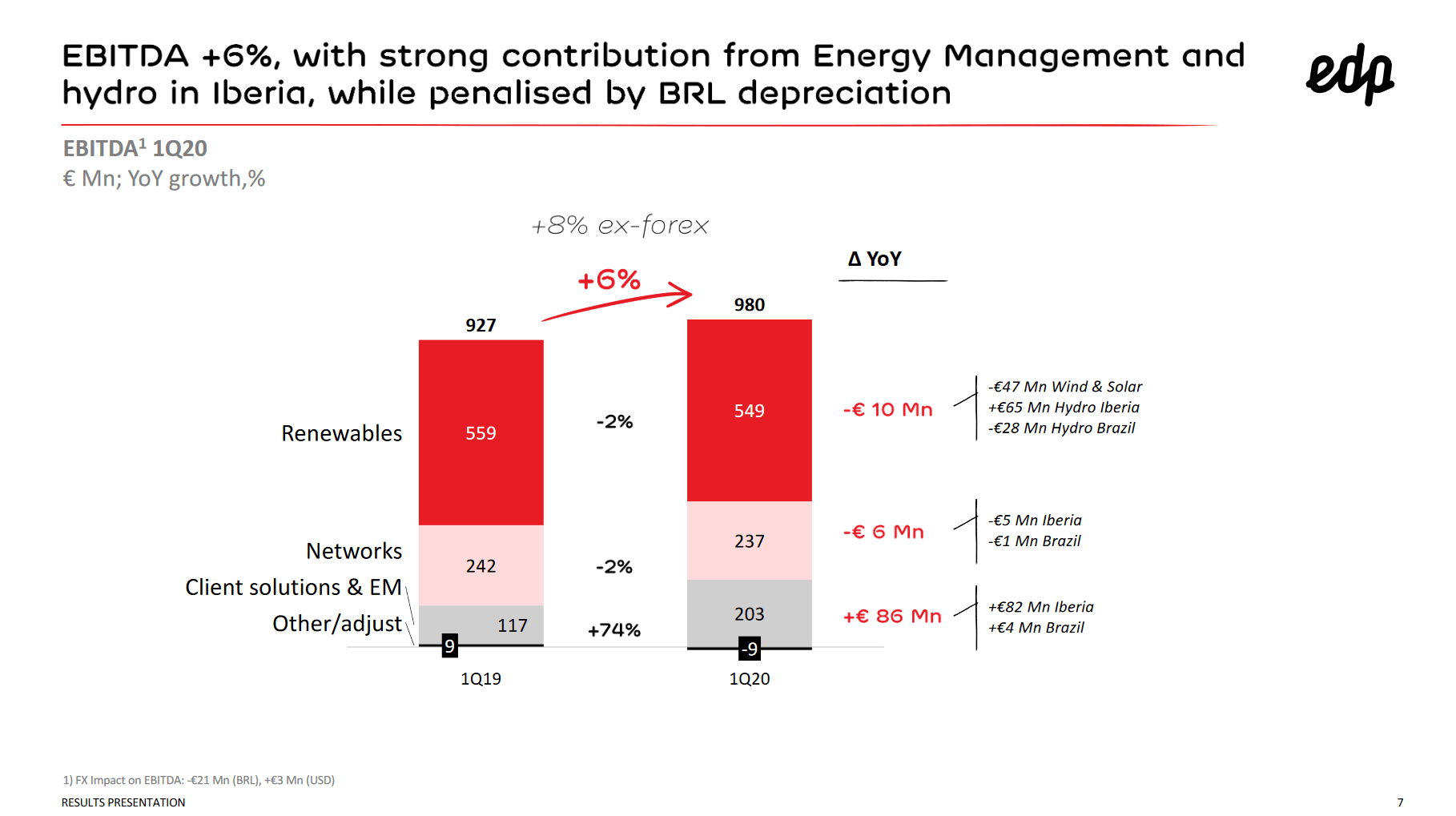

In fact, the only major source of volatility comes from factors entirely unrelated to the exposure of the business to economic risks. Weather effects have had large impacts on the renewable energy business in the past, with periods of little rain affecting EDP’s Iberia-concentrated hydro assets for almost a year. Likewise, windiness can impact the substantial portfolio of wind assets as well. Nonetheless, we expect that over time these natural fluctuations should result in flat power generation on average and can be written off as extraordinary negative or positive effects.

(Source: EDP Q1 2020 Pres)

Asset Base Undervalued

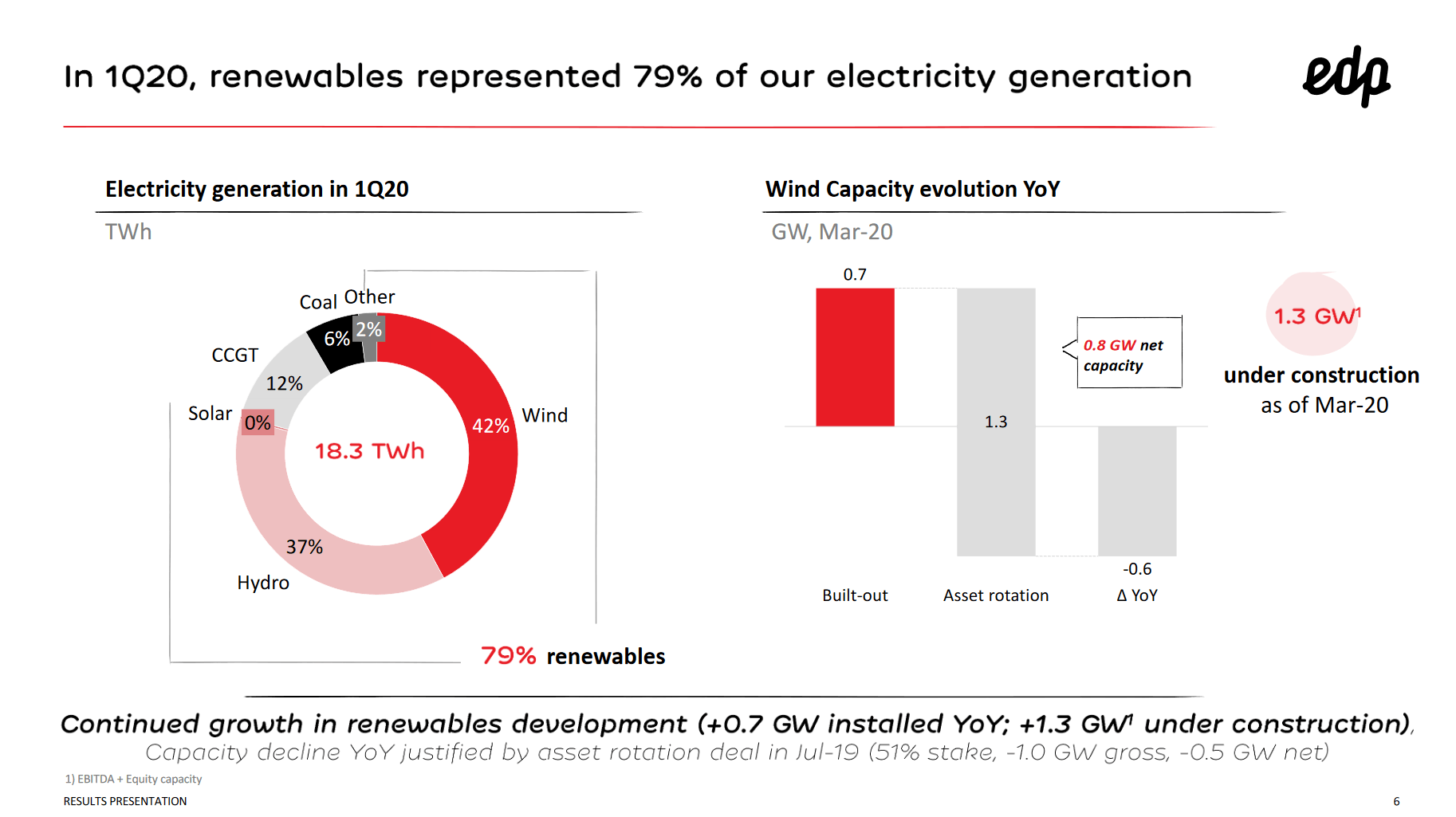

In addition to a resilient income to support the current 4.2% dividend yield, EDP also shows signs of being undervalued. Consider that a sizable portion of their hydro assets in Iberia were recently agreed to be sold to a consortium led by Engie. This transaction constitutes a superb precedent to value their hydro assets.

(Source: EDP Q1 2020 Pres)

Considering that they also have a large wind portfolio, constituting primarily traditional onshore wind assets, we can use our recent coverage of peers to value those assets as well.

(Source: Valkyrie Research)

(Source: Valkyrie Research)

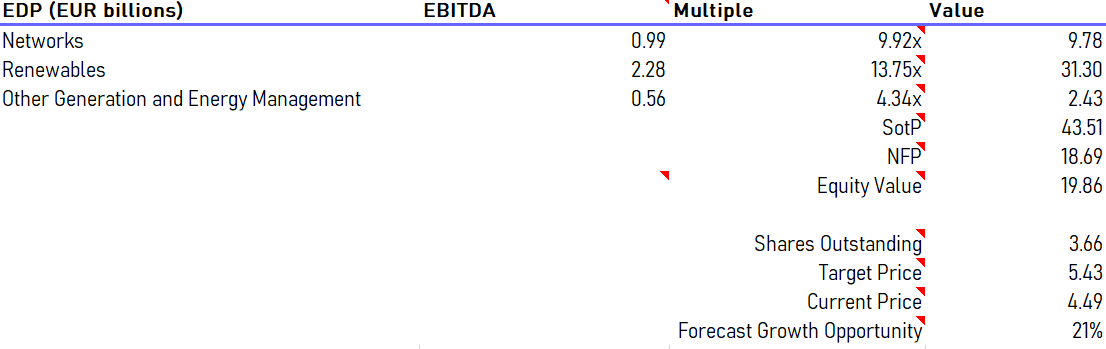

Applying the TWh as weights to create a weighted multiple based on mix in renewable technologies, using Iren (OTCPK:IRDEF) as a multiple for CCGT (which it uses extensively in its generation) and applying a 0x multiple for coal within ‘Other Generation and Energy Management’, as well as applying a 9.92x multiple for the networks business using Red Electrica (OTCPK:RDEIY) as a comp, we get the following valuation.

(Source: TTM Data, Valkyrie Research, NCIs included)

(Source: TTM Data, Valkyrie Research, NCIs included)

Given EDP’s focus on renewable, we can be rather sure that some market actors are paying attention to their renewable assets, especially with a comp so relevant. This means that even though the renewable assets are perhaps not getting full recognition, a fair portion of the undervaluation must be coming from Networks even though it’s a much smaller segment than renewable, since we were conservative with the CCGT and thermal multiples.

We used Red Electrica as a comp for networks specifically because the CNMC which determines Red Electrica’s compensation is rather unfriendly to investors, where risks related to outcomes of Spanish elections have been credibly cited in the past. This rather conservative multiple was supposed to reflect the greater uncertainty with emerging market governments, even though Brazil, whose authorities determine EDP Brasil transmission compensation, have had a better track record than the CNMC.

(Source: EDP Q1 2020 Pres)

(Source: EDP Q1 2020 Pres)

The reason we think that our upside is very credible is to do with the way equity research analysts on the Street value EDP. For the Brazilian business, they will simply take the Brazilian business EBITDA and apply a mark-to-market approach using the publicly listed subsidiary EDP Brasil. However, this method has some erroneous assumptions baked in. Although some discount might be justified compared to European players due to EDP Brasil being in an EM, the current multiple on EDP Brasil, which is 6.3 EV/EBITDA is close to what one would get if you applied a reasonable 20% EM discount on the overall multiple derived from a target multiple analysis on the business using the Brazilian regulatory WACC for DSOs and TSOs of around 7.5%. This would be with the conservative assumption that the ROIC and WACC were equal, which is what governments basically aim for when remunerating regulated utility operators.

However, this 7.5% WACC cannot be used for valuing EDP Brasil. Firstly, it does not represent the funding conditions that a sponsored organisation like EDP Brasil has, where they are securing much lower rate bonds based on current IPCA. Secondly, target multiple analysis, which is derived directly from DCF, has the inherent drawback of excessively discounting companies when higher WACCs are used as a way to adjust the valuation for risk, where probability weighted cash flows is the rigorous way to incorporate specific risks in cash flow analysis. Excessively discounting the Brazilian business by using the higher regulatory WACC (which is simply a driver of rates of remuneration, not necessarily proportionate to specific business risk) than their Spanish counterparts, where the regulatory WACC is around 5%, is inappropriate especially since the level of risk between the businesses is not particularly different, as they both have similar regulatory economics and similar reliability of utility authorities. Overall, we think that using a mark-to-market approach here perpetuates some erroneous assumptions that are evident from the use of regulatory WACC as a proxy for a risk-proportionate discount rate.

(Source: EDP Brasil Q1 2020 Pres).

This approach with the Brazilian business would be conducted while using multiples closer to that of Red Electrica for the Portuguese and Spanish concessions, and explains 4% of the 21% upside shown above despite the smaller weight of the network business.

Conclusions and Risks

Most of EDP’s business is without much risks. Clearly the renewable energy assets are dependent on certain weather conditions, and a figurative ‘perfect storm’ could perhaps impair their ability to pay the dividend if very unlucky. Within their emerging markets exposure, i.e their distribution and transmission operating concessions (TSO and DSO), there are risks related to changing remuneration schemes, which as of recently will be re-evaluated on a yearly basis in Brazil according to recent ANEEL directives. These can decline with declining interest rates on Brazilian sovereign debt, but this is partially offset by better debt-raising conditions.

Moreover, our assessment of the valuation could be inaccurate. However, even applying a 6.3 EV/EBITDA to the Brazilian business and Red Electrica multiples to the other concessions within the networks segment (weighted 8.5x for overall networks business), there is still a strong of margin of safety. If we were correct in our assessment, this would also indicate that the renewable assets aren’t being valued with the proper premium that they’ve been able to justifiably command on an increasingly crowded renewable energy market where ESG is becoming a prime European issue.

With the high likelihood of a healthy margin of safety from the valuation side, and a reliable 4.2% dividend yield on the income side, EDP strikes us as an excellent, all-weather utility pick for whatever might happen in the coming quarters. We rate EDP a buy.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}