Buyout quick take

58.com (WUBA) is China’s largest online classifieds marketplace and has recently entered a definitive agreement for a going-private transaction which will value the shares at $56 per ADS. The transaction implies an equity value of approximately US$8.7B for the company which will be acquired by a consortium of investors, including Warburg Pincus Asia LLC, General Atlantic Singapore Fund Pte. Ltd., and Ocean Link Partners Limited.

The stock has been trading closer to its proposed buyout price which is expected to close sometime in 2H20e. There is a slight possibility that the proposal could be rejected should the business recover and that the buyout price is still meaningfully lower than its peak YTD.

The consortium holds ~44% of the shares and will still require about 22% voting right to put the motion forward. The other significant shareholder is Tencent (OTCPK:TCEHY) who owns about 28% voting rights and has a board seat. I believe it was likely that Tencent was in favor of the motion already.

Data by YCharts

Data by YCharts

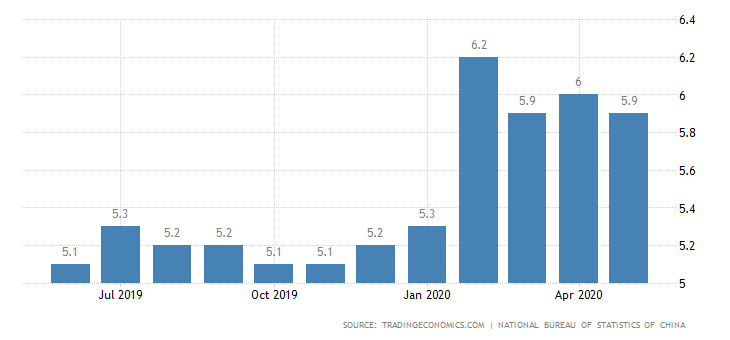

China job market is set to rebound

Given that China is already emerging out of the economic and health crisis caused by the pandemic, the job market will likely begin to embark on a recovery with various macro indicators showing positive signs.

China unemployment rate spiked but declining

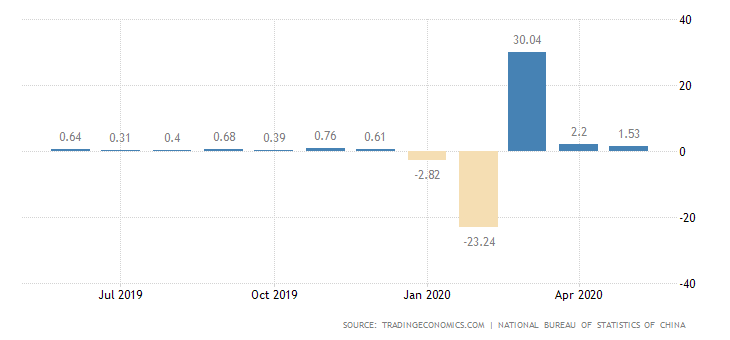

Industrial production (month-on-month change)

Industrial production took a large hit in February (partially due to the timing of the Chinese New Year holiday). But, as the country began to recover from the pandemic, cities gradually relieved lockdown conditions, and factories were allowed to resume. The March jump was mainly due to the digestion of the backlog.

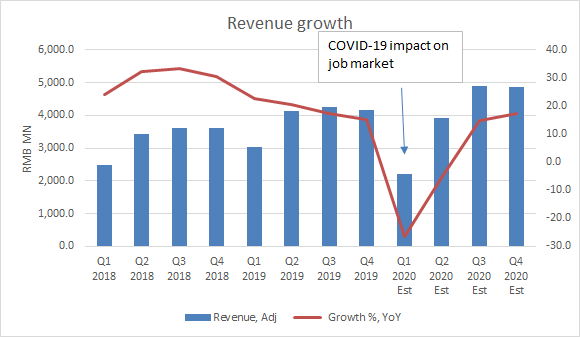

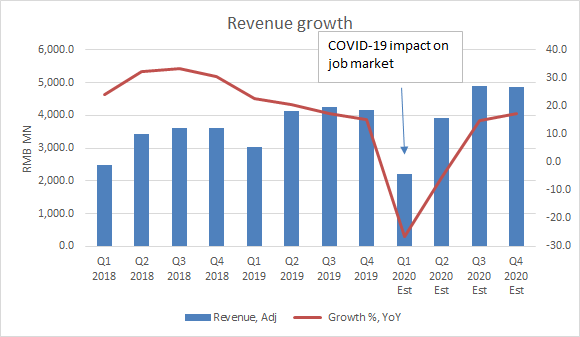

Market forecasts a V-shape rebound

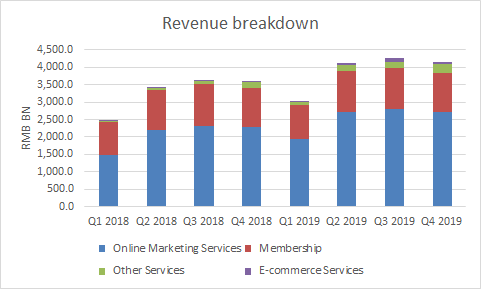

The company is estimated to return to double-digit (10-20%) revenue growth as China emerges out of the pandemic. Online marketing which is its biggest revenue driver is expected to rebound sharply.

Source: Bloomberg estimates, Himalayas Research

Source: Bloomberg, Company, Himalayas Research

Source: Bloomberg estimates, Himalayas Research

Pressured valuation

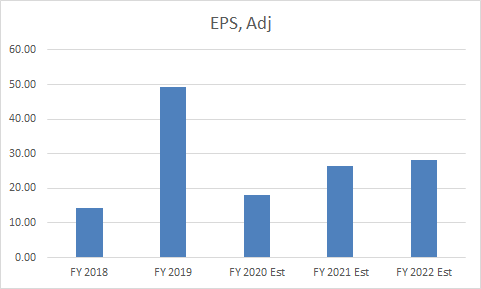

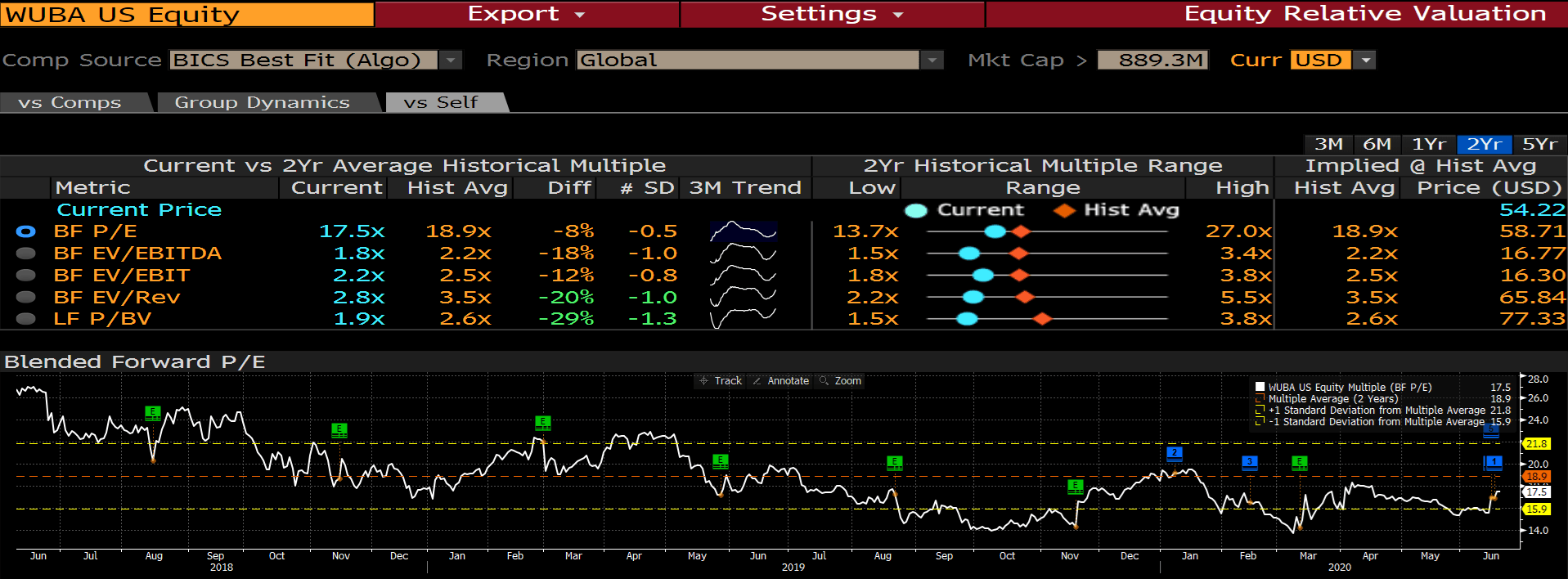

The stock is trading at about 17.5x forward earnings. Its 2-year historical average is only about 1.4 turns higher. EPS estimates for FY20e and FY21e are RMB18.2 and RMB26.5, implying a decline of 63% and an increase of 45% YoY, respectively. EPS 2018-2021e CAGR is estimated to be about 22.6%, which is quite healthy from a longer-term perspective.

Unless the proposed buyout is revised, the price is currently the ceiling for the stock, leaving current expected return quite low. Thus, I have a neutral view on the stock.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Disclaimer: All research, figures, and interpretation are provided on a best effort basis only and may be subject to error. Any view, opinion, or analysis does not constitute as investment or trading advice, please do your own due diligence.

{kind=link}