SINGAPORE (ICIS)–Asian demand for chemical raw

materials that go into protective barriers used

to prevent coronavirus transmissions is

expected to remain buoyant as more economies in

the region reopen.

The uptick in demand for polymethyl

methacrylate (PMMA) into acrylic sheets for

transparent barriers is increasing in Asia as

economies slowly reopen, with indications that

this will continue for some time amid the

ongoing pandemic.

Sheet makers are now seeing increased demand

from within southeast Asia including Singapore,

Thailand and Indonesia, as lockdown

restrictions are being lifted.

Thailand started the last stage of its lockdown

on 1 June with the aim to fully re-open its

economy on 1 July, while Indonesia’s

“large-scale social curbs” ended on 4 June.

Singapore will also enter the next phase of its

economic reopening from 19 June.

In the week ended 4 June, PMMA prices were

assessed at an average of $1,500/tonne CFR

(cost & freight) China, up by $35/tonne

from the previous week, according to ICIS data.

Key feedstock acetone CFR CMP (China Main

Ports) prices have risen by more than twofold

since early April to an average of $1,050/tonne

in the week ended 12 June.

China domestic MMA prices have surged by 83%

since early April to CNY 13,000/tonne extank

east China in the week ended 12 June.

Transparent sheets are now being installed in

shops, restaurants, offices, hospitals and

other public spaces to prevent coronavirus

transmissions.

Cast acrylic sheet, made directly from the

monomer, and also extruded acrylic sheet, made

from PMMA resins, are commonly used to make

these barriers.

According to an Asia-based PMMA producer,

demand for protective sheets is still firm in

US, Europe and Middle East.

The producer, who sells PMMA resins to

extrusion sheet makers in the these regions,

said that it is receiving spot enquiries and

expects demand to remain supportive for the

rest of the year.

However, demand for protective barriers alone

is insufficient to lift overall demand for MMA

as other downstream sectors remain weak, with

major industries such as automotive and

construction still heavily impacted by

disruptions caused by the coronavirus.

This may result in weaker overall demand growth

for these products in the months ahead compared

with the sharp shikes seen so far this year.

Global exports of MMA to-date this year now

stands at 343,638 tonnes, according to ICIS

data.

Global shipments totalled 1.31m tonnes for the

whole of 2019.

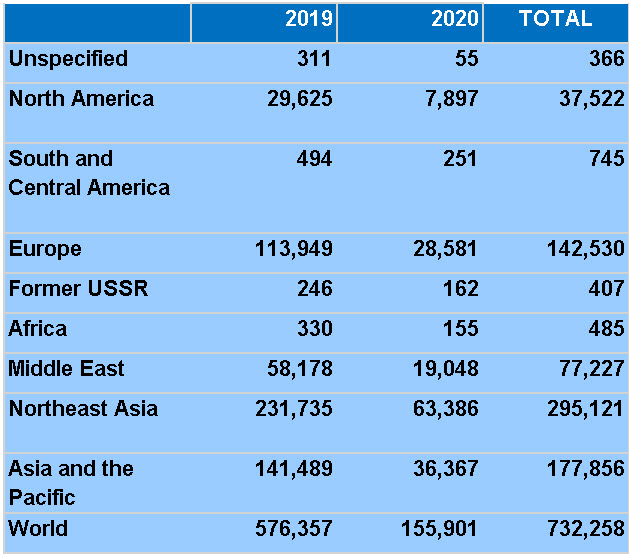

Global exports of PMMA meanwhile are at 155,901

tonnes while global shipments of PMMA totalled

576,357 tonnes last year.

Global PMMA Exports

Source:

ICIS

DEMAND FOR PERSONAL PROTECTIVE

EQUIPMENT SUPPORTING PP

With the

coronavirus pandemic, growing demand for face

masks, disposable syringes, and other medical

protective equipment is expected to boost the

supply of transparent polypropylene (TPP) grade

and polypropylene (PP) fibre grade, according

to US based analysis firm Beroe.

Demand for PP from the medical sector in China

remains supportive, especially for the

production of face masks, according to ICIS

senior analyst Joey Zhou.

Masks are made of two fibrous layers which use

PP fibre as the raw material, and a melt blown

fabric layer for antivirus protection which

needs to use high melting index PP (melting

1500).

“China is the largest producer for face masks

and both domestic and export demand remains

strong,” Zhou said.

The production of face masks remain the key

drive for fibre-grade PP in the short term.

However, demand has since waned since its peak

in April when face masks were in shorter supply

and will not be able to push PP prices much

higher, she said.

There are also government-led moves to tighten

regulations on illegal factories producing face

masks.

Furthermore, the higher production of face

masks has lowered their prices back to normal

levels, according to Zhou.

In southeast Asia, demand for PP non-woven,

fibre grades previously saw a surge in the

demand earlier in the year, which led to some

producers focusing production of these

grades, owing to increased demand and

attractive premiums.

However, demand for non-woven grades has

tapered down in recent weeks, amid the

slowing spread of the coronavirus in

southeast Asia.

Premiums have also been eroded as a result.

Offers for non-woven major supplier in

southeast Asia were at around $980/tonne CFR

(cost and freight) southeast (SE) Asia for

June shipments.

Offers were previously above the $1,000/tonne

mark.

In longer term, demand for fibre-grade PP can

support overall demand but will not be the key

driver. Demand from medical section takes over

less than 5% of China’s total PP demand,

according to Zhou.

With additional reporting by Li Li Chng and

Leanne Tan

Focus article by Nurluqman

Suratman

{kind=link}