{kind=link}

Bear markets and recessions are the metaphorical “restart button” which, in classical economic theory, flush away the excesses and misallocations of capital created during the previous economic expansion. In capital markets, a similar restart button is often pushed, usually creating a rotation in leadership. We all know that one of the key facets of value investing is that the most overpriced stocks, sectors, and countries, will tend to underperform similarly undervalued stocks, sectors, and countries over a long enough period of time. Thus, it makes sense that bear markets have historically provided turning points in leadership between value and growth investing. See the chart below for an illustration of a relative strength chart of the MSCI World Value Index versus the MSCI World Growth Index (click the image to enlarge).

Source: MSCI

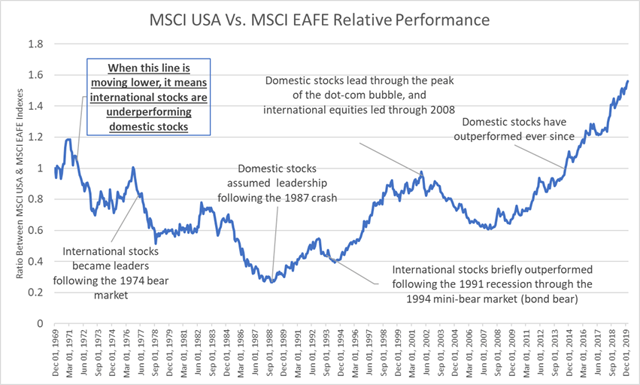

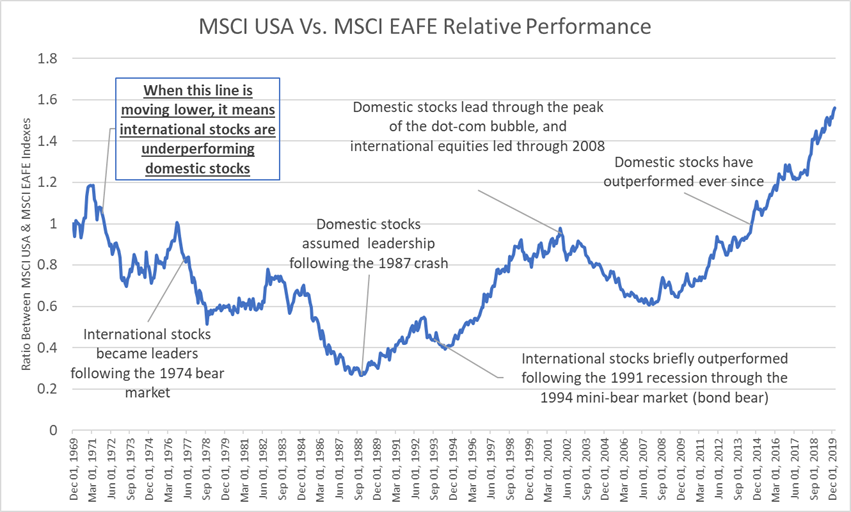

Similarly, bear markets have often provided the impetus for changes in leadership between stocks domiciled in the United States versus those of other countries.

Source: MSCI

Source: MSCI

Therefore, simply observing these patterns leads to a conclusion that the time to begin investing in value and international stocks is nigh, or at least soon. However, these are only historical patterns – we need some fundamental data to confirm our story.

Capital Market Assumptions Suggest Higher Returns For Both Value Stocks & International Markets

We will go through this exercise to confirm that there is a fundamental story to confirm that international stocks and value investing are both primed to outperform going forward. Most major companies release their own forecasts of expected returns for various asset classes using fundamental data, and most of them suggest international stocks will outperform over the next decade.

Here you can see Research Affiliates’ expected returns. As of the end of February, EAFE equities had an expected annual return 2% higher than US large cap equities. That’s a roughly 22% return differential over 10 years.

Blackrock similarly expects European and emerging market equities to deliver longer term outperformance on the basis of undervaluation

With regard to value stocks, GuruFocus.com creates a convenient table of the S&P 500 sectors and their respective P/E ratios. The annotations are my own.

Source: GuruFocus.com

One can see that in the chart above, sectors like technology (XLK) and healthcare (XLV), are significantly undervalued relative to financials (XLF), energy (XLE), and industrials (XLI).

I’ve Heard These Plays for Years. Tell Me About Timing

The running joke is that international markets and value stocks have been undervalued for the last several years, and they have continued to underperform for the last several years anyway. The current bear market, if historical patterns repeat, suggests that the potential for a leadership change now is higher versus during in the middle of a bull market.

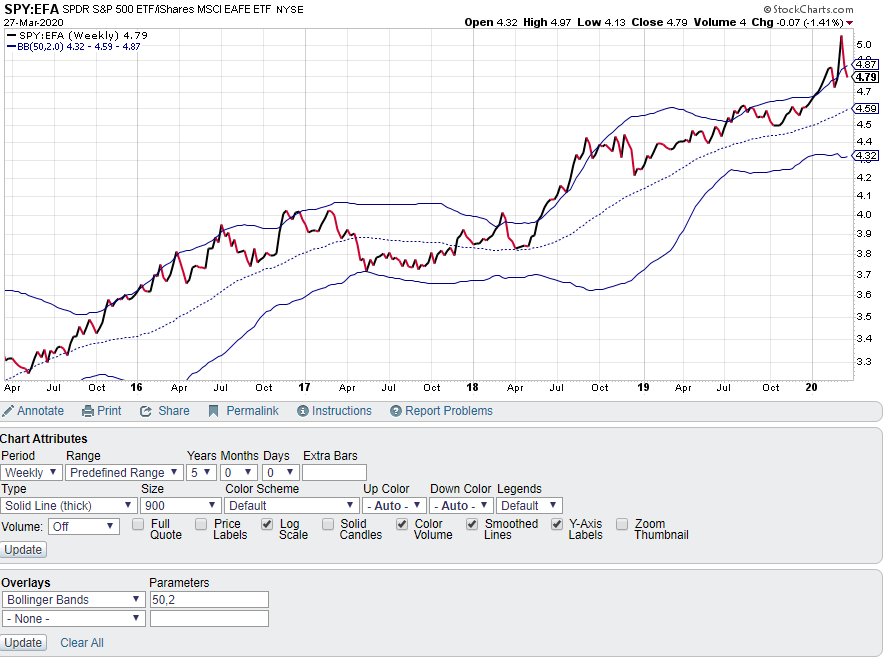

Even so, I can appreciate anyone who would prefer to fine tune their asset allocation changes. One method I use for fine-tuning my valuation-based investment adjustments is to use some sort of trend following signal. In the example below, I create a weekly ratio chart of the S&P 500 ETF (SPY) and the MSCI EAFE (EFA) ETF and then plot Bollinger Bands around it. In this case, if the ratio touches the bottom band, it would be an indication that international stocks are catching a bid and that I would overweight them relative to domestic stocks. You can see one of my chart settings below.

Source: StockCharts.com

As expected, this trend following strategy has had one overweight US equities for most of the last five years. Once could use other trend-following systems such as moving averages, price channels, or linear regression slopes to accomplish a similar goal.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.