Subscribe to The Financial Brand via email for FREE!

When Ally Bank opened its innovation lab, called “TM Studio,” in 2018 in the Camp North End neighborhood of Charlotte, N.C., it wanted to drive innovation in a new way. While financial labs often risk becoming something of an ivory tower, where the danger is that everyone sits around going in esoteric directions, Ally decided to maintain a small permanent staff. Projects are driven by teams assembled from experts in various disciplines from around the bank, tasked for a specific project and often rotated out when that’s done.

But before much happens in the Studio, Ally goes to the man or woman on the street.

And that’s pretty much literal, according to Emily Shallal, Senior Director, Customer Strategy & Innovation. Shallal, head of the Studio’s small permanent staff, says when Ally decides to develop a new product or service it prefers not to proceed from pre-conceived ideas. So it sends representatives out to meet the public and ask them about what the bank is thinking of. Part of the aim is to get input to product development from both customers and non-customers.

Building Features to Help People Save More

That was the start of the 18-month process that led to Ally’s development of a new selection of smart savings tools that it has added to its online savings account. “With those consumer conversations, they kind of crafted themselves,” says Shallal.

That’s a bit of an exaggeration — it’s one thing to come up with an idea and quite another to make it practical, and it took a team including bankers, IT staff, product strategists and user experience designers to develop the idea. But consumers’ input played a major part. One thing that Shallal noted was how much emotion gets tied up with subjects like savings.

“People get really stressed when they talk about money,” says Shallal.

“You can see them tense up.” She recalled one person she and staff met with who became flushed, and began fanning herself, when the subject of savings came up.

The research put human faces on troublesome statistics about Americans’ difficulty in saving. Study after study points out that large portions of the population cannot pay cash for a $400 emergency, for example. It’s a frustration and a fear. But actually talking to consumers began to illustrate what would help.

“People love smart algorithms,” says Shallal, who was a financial planner earlier in her career, “but you have to build a level of trust. What we heard from people around automation was often about maintaining control over their money.”

There’s control of money and then there’s self-control, of course. Ally notes that statistical research indicates that four out of five consumers are not personally “wired” to save, tending to spend what they have on hand in the short-term. While people may know in their heads that they must save, their heads don’t always talk to their wallets.

Read More:

Features to Drive Savings, Not Just Tips

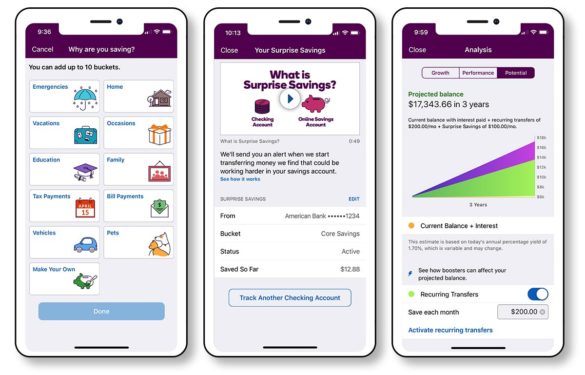

One feature developed for the app was “Buckets,” which gives consumers the ability to pick up to 10 savings goals in a single savings account, which they can give custom names to, such as “Disney World Vacation,” to build an emotional connection to the goal. Icons representing different savings purposes are assigned to each “Bucket.” The app tracks the user’s progress toward each goal. This is essentially an electronic version of the traditional envelope method for managing household cash, with more convenience and ease in changing plans.

REGISTER FOR THIS FREE WEBINAR

Modernizing B2B Payments with RTP

Find out why current B2B payment flows are fragmented and how RTP has the potential to significantly improve the B2B payment experience for all.

Thursday, February 27th at 2pm EST

Another feature is called “Boosters.” There are two types, each of which move excess funds from the consumer’s checking account to their savings account. (Ally can make transfers from its own checking accounts or those of other financial institutions, via ACH withdrawals.) The idea behind both was to facilitate savings, not just issue tips about how to save.

• “Recurring Transfers” enable consumers who are confident about their earnings levels to set transfers to follow a regular schedule. The consumer can set the frequency of recurring transfers and adjust the size and how they are distributed among the buckets. These automated transfers might be directed to one top priority bucket, for example.

• “Surprise Savings” analyzes the linked checking account. Based on cash flow, historical spending patterns, upcoming bills and the overall account balance, this feature of the app computes how much is safe to transfer to savings. The bank does not transfer more than $100 at a time and won’t transfer more than three times in a week, in order to avoid the risk of overdrafts. Account holders can adjust this feature or turn it completely off, as well.

Ally’s product testing found that both boosters tended to bolster account holders’ confidence levels, creating savings momentum.

The third feature, “Analysis,” shows projections of how savings will build up under current settings and allows the consumer to set up “what ifs” to see what changes would help them reach their goals more quickly.

Shallal says the company’s research indicates that consumers who use these proactive savings approaches can save five times as much compared to relying solely on accumulating compounded interest.

{kind=link}