Investment Thesis

Pembina Pipeline Corporation (PBA) is an ideal holding for long-term wealth generation due to its stable earnings, massive growth plans and business model that supports consistent dividend growth. Pembina has been able to grow its business organically and through acquisition without attracting the negative headlines and regulatory delays that have plagued other midstream firms. The company is advancing an exciting portfolio of growth projects that will create shareholder value in the coming years. The company’s growth plan focuses on value extension through vertical integration. Pembina is pursuing this strategy across a broad portfolio of its business units, including polypropylene, oil sands, LNG and shale fracking. This growth strategy provides clear visibility for Pembina’s long term dividend growth potential. Pembina is well-positioned to continue growing and improving the quality and stability of its earnings. Through its recent growth, Pembina has enhanced the stability of its earnings by deriving more of it’s EBITDA through fee-based contracts that minimize commodity price sensitivity in earnings. Pembina is a great long-term investment for investors seeking a steadily growing stream of monthly income.

Company Profile

Pembina Pipeline was founded in Alberta, Canada, in 1954 to service the Pembina oil field. Over the last 65 years, Pembina has expanded its operations to include gas and liquids pipeline infrastructure as well as gas gathering and processing facilities. Headquartered in Calgary, Alberta, Pembina employs 2,100 people across North America. The company trades on the Toronto Stock Exchange under the ticker “PPL” and the New York Stock Exchange under the symbol “PBA,” where it has a market capitalization of ~CAD $26B (~USD $20B).

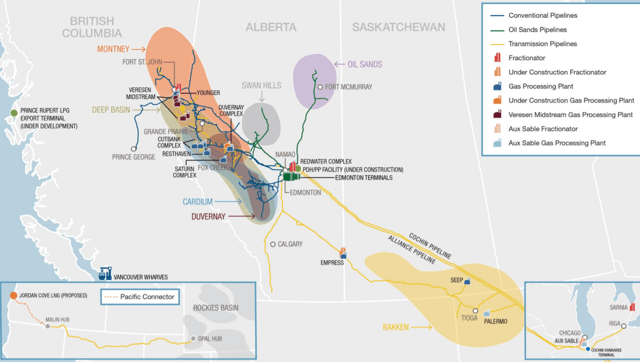

Pembina’s total transportation capacity throughout its network is approximately 3.2 mmboe/d, making it one of the larger midsize midstream companies in North America. Although it has expanded and diversified since its 2019 acquisition of Kinder Morgan Canada, Pembina primarily focuses on the western Canadian basis. In this region, Pembina has the largest fractionation capacity and is the largest third-party gas processor with capacity of 6.1 bcf/d. Amassed through a series of acquisitions, Pembina also operates a growing gas and liquids storage business with more than 23.8 mmbbl of hydrocarbon storage capacity.

Source: Pembina Corporate Update January 2020

As a vertically integrated firm, Pembina operates an extensive network of oil and natural gas liquids infrastructure that includes processing and marketing. Pembina’s oil sands pipeline operations underpinned by long-term contracts have healthy margins that have supported the company’s growth in other areas. Pembina is currently advancing significant growth opportunities in LNG and Polypropylene that will expand its scope and further optimize the company’s position in the hydrocarbon value chain. Pembina is a key supplier of condensate to oil sands producers; a required additive to thick crude that allows it to flow through pipelines.

Kinder Morgan Acquisition

Following a series of regulatory delays on its signature TransMountain Pipeline Expansion project, in May 2018, Kinder Morgan Canada Limited (OTCPK:KMLGF) sold its project to the federal government of Canada for CAD $4.5B. In the months following this sale, having lost scale in Canada, Kinder Morgan, Inc. (KMI) made the decision to sell their remaining Canadian assets as well as the U.S. Portion of the Cochin pipeline system; fully contracted, cross-border pipeline system.

Pembina’s strong balance sheet position enabled it to pick up Kinder Morgan’s Canadian assets for CAD $4.35B (USD $3.3B) in August 2019. The purchase added ~10M barrels of terminal storage capacity in Edmonton as well as a West Coast export assets at the Vancouver Wharves. The Cochin Pipeline system for which Pembina paid Kinder Morgan USD $1.546B, is a condensate import pipeline that connects Pembina’s Channahon, Bakken and Edmonton assets. The addition of these Kinder Morgan assets provides diversification across multiple condensate production basins by linking Aux Sable and Red Water. The pipeline also presents Pembina the opportunity to develop further in the Bakken and to connect to the company’s assets in Sarnia, Ontario. The acquisition of Kinder Morgan Canada’s assets has transformed Pembina from a regional transporter into a significant player in the North American energy infrastructure market.

These assets are a good strategic fit for Pembina as they enhance vertical integration, add scale and help to diversify the company. Following the deal, Pembina is better diversified in terms of geography, customer base and currency. According to Chris Cox, Equity Research Analyst at Raymond James:

The acquisition further strengthens the quality of the company’s integrated value chain, improves the quality of the company’s cash flows and adds a new compelling business line with the Edmonton storage business.

The acquisition has also been immediately accretive for Pembina as the assets being acquired are expected to generate CAD $350M in EBITDA in 2019 and yield CAD $50M in run rate synergies over the next five years.

Growth Profile

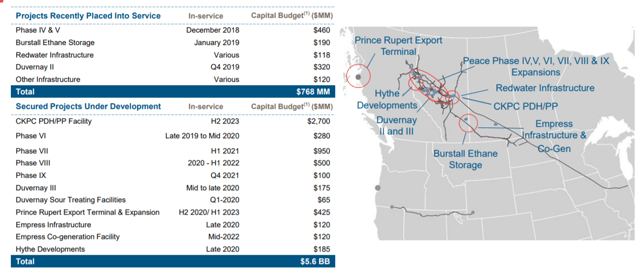

Pembina’s numerous attractive growth opportunities are what makes it a compelling long-term investment. The company is well-positioned to capitalize on a broad-based portfolio of growth projects. These include opportunities in LNG, shale fracking, oil sands and polypropylene. While Pembina has demonstrated its ability to successfully acquire and integrate companies, it has developed its own ambitious organic growth strategy. Pembina has a secured project portfolio of CAD $5.6B out to 2023. In addition to its secured capital program, Pembina has an additional CAD $4.4B of projects awaiting final investment decision, including further pipeline expansion in the Peace region and the Duvernay.

Source: Pembina Corporate Update January 2020

Polypropylene

To advance its Alberta polypropylene & propane dehydrogenation facility, Pembina entered into a 50/50 joint venture with Petrochemical Industries Company K.S.C. of Kuwait. Regional rival Inter Pipeline Ltd. (OTCPK:IPPLF) is advancing a similar project, however the market has responded better to Pembina’s efforts of de-risking the petrochemical project by securing an experienced partner, rather than going it alone as Inter Pipeline has done. This joint venture will allow Pembina to take advantage of cheap and abundant propane feedstock in western Canada and move its product up the value chain into plastics. This is an exciting opportunity for Pembina as the polypropylene market is forecast to see demand growth of 22% over the next five years in North America. When operational in mid-2023, the facility is expected to utilize ~23,000 bpd of propane to produce 550K metric tonnes of polymer-grade propylene and polypropylene production annually.

Source: Financial Post

Peace Pipeline Expansion

Beyond its CAD $2.7B investment in the polypropylene facility in central Alberta, Pembina’s largest current capital commitment is the expansion of its Peace Pipeline system. Following the success of its recent Peace Pipeline expansions, the company has advanced Phases VI-IX, which together account for an additional CAD $1.83B investment. These highly achievable segments are anticipated to come into service approximately one phase per year out to 2023. These phases are supported by strong demand and underpinned by 10-year contracts with take-or-pay provisions which will result in the addition of stable cash flow for incremental pipeline capacity. Pembina’s ultimate goal is to have segregated ethane-plus, propane-plus, crude and condensate lines across multiple pipeline systems in the Peace region. Product segregation in the pipeline system will support “incremental customer demand in the Montney area by debottlenecking constraints, accessing downstream capacity, and further enhancing product segregation on the system.”

Source: Pembina

LNG Expansion

In addition to its secured and uncommitted pipeline of expansion projects, Pembina is also evaluating CAD $6.5B+ of value chain extension projects. The most important of these projects currently in the preliminary regulatory approval phase is the Jordan Cove LNG Terminal. This proposed project in Coos Bay, Oregon, would feature a liquefaction and export facility with an LNG production capacity of ~1.3 bcf/d. The terminal would be connected by a newly proposed ~229 mile (~369 km) pipeline connecting Coos Bay to Malin Hub in southern Oregon.

The project would facilitate the delivery of natural gas from western North America to Japan. Oregon is a nine-day boat trip to Japan that avoids the hurricane risks of Atlantic routes and the costs of the Panama Canal. LNG shipped from Oregon to Tokyo will be competitively priced compared to LNG shipped from the U.S. Gulf Coast. The final Federal Energy Regulatory Commission (FERC) decision is expected in February 2020.

Global demand for gas is forecast to grow by 45% from 2015 to 2030 with Asia being the key driver of demand growth. West coast LNG export capacity would give Pembina significant exposure to demand growth for the world’s fastest demand growth hydrocarbon in its fastest-growing region. LNG also fits well with the company’s model of vertical integration and value added model. With robust processing and collection assets at the wellhead, Pembina will be able to capture full value for this commodity by ensuring its delivery to the most attractive global markets.

A Business Model that Supports Dividend Confidence

As many readers will know, the single most important litmus test that I use to measure management’s confidence in future earnings is the firm’s record of dividend growth. I favour companies with long histories of uninterrupted dividend payments that span all stages of economic cycles. No company wants to be in a position to cut its dividend, so corporate directors take the decision to commit to a dividend increase very seriously as these commitments have long-term recurring impact on available capital. While companies across many industries have achieved impressive dividend growth records, the companies that investors can have the most confidence in are ones that can demonstrate clear pathways to earnings growth and a high degree of stable recurring revenue.

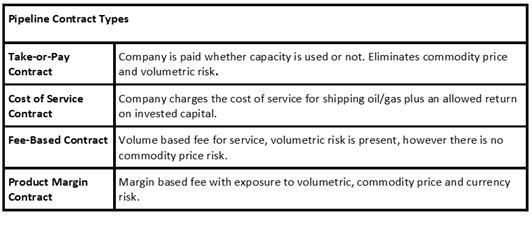

Midstream companies fit this bill nicely as their cash flow is largely underpinned by long-term fee for service contracts. Pembina’s practice of covering 100% of all dividend payouts and corporate costs through fee-based revenue ensures stability in its model and allows for increased optionality for uses of non-fee based revenue such as the company’s margin-based revenues. At 85% of estimated 2019 adjusted EBITDA, Pembina’s fee-based revenue accounts for the vast majority of its earnings. Included within this 85% of EBITDA that is sheltered from commodity price fluctuations is 64% of total 2019E EBITDA that is comprised of take-or-pay contracts and cost-of service contracts that eliminate volumetric fluctuation risk as well. At 85% for 2019, the portion of EBITDA that is fee-based has improved from 77% in 2016. This improvement in the quality and stability of earnings is a meaningful compliment to the firm’s growth in total EBITDA.

Source: Sell Side Handbook

Dividend Growth

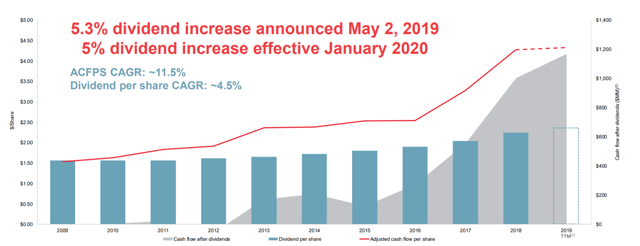

Pembina paid its first distribution in 1997 and has been rewarding shareholders ever since. In 2010, Pembina converted from a Trust to a Corporation and started paying dividends. Pembina’s allocation of monthly versus quarterly dividends makes the company an ideal income holding. In January 2020, the company increased its monthly dividend by CAD $0.01 per share, to CAD $0.21 per common share, marking the 9th consecutive year of dividend increases.

Morningstar Senior Equity Analyst Joe Gemino estimates 2020 distributable cash flow to be CAD $1.6B for a distributable cash coverage ratio of 1.25X, leaving the company well-positioned to support its dividend. Over the next 5 years, Morningstar expects Pembina to increase its annual dividend at an average annual rate of 5% while maintaining a comfortable distributable cash coverage ratio averaging 1.45X out to 2025.

Source: Pembina Corporate Update January 2020

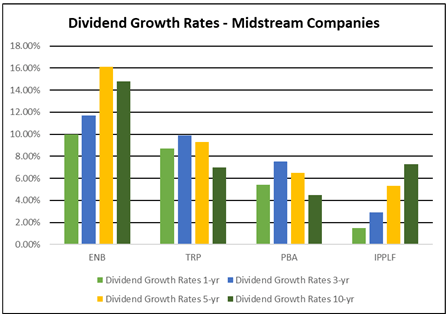

Compared to Enbridge Inc. (ENB) and TC Energy Corporation (TRP), Pembina has a much slower dividend growth rate at 4.5% annually over the last decade. At the same time, the company has grown adjusted cash flow per share at an annualized rate of 11.5% since 2009. This trend of having cash flow per share outpace dividend growth has allowed Pembina’s dividend payout ratio to steadily decline to its current level of ~74%. While growth has not been as impressive as its larger peers, Pembina’s reasonable payout ratio and its gap between its cash flow growth and its dividend growth should allow the company to continue its steady dividend growth for years to come.

Source: Graph Author, Data from Canadian Dividend All-Star List

Valuation

Pembina is currently trading at an Enterprise Value/EBITDA ratio of 17.13X, below the company’s 5-year average of 18.82X. The company’s Price/Cash Flow ratio of 10.45X is below the company’s 5-year average of 13.66X. The current dividend yield of 4.99% is in line with the firm’s 5-year average yield of 4.83%, suggesting that dividend growth has kept up with share price appreciation.

Source: Seeking Alpha

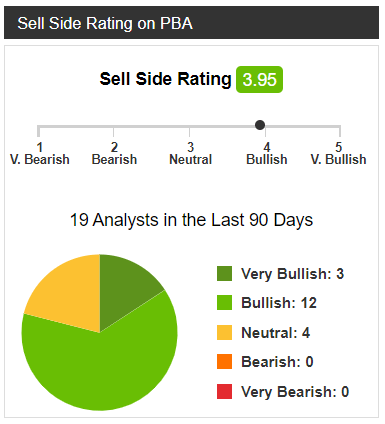

Sell-side analysts are bullish on Pembina with 15 of 18 analysts with ratings on the stock citing bullish or very bullish. Of the 18 analysts who maintain one-year price targets on the company, the median target price is CAD $55.89, suggesting an upside of approximately ~9% for a total return of ~14%. A total return in the mid-teens with 5% annual dividend growth is attractive in an era of frothy stock markets.

Source: Yahoo Finance

Risk Analysis

Midstream companies tend to have a degree of revenue that is regulated or contracted over the long term. Most pipeline expansion projects are not built until shippers have signed long-term contracts that ensure capital costs are recouped over time. As noted previously, Pembina enjoys a significant portion of its earnings being considered lower risk with fee-based contracts rather reducing the firm’s commodity price and volumetric risks. However, even at 85% of EBITDA being fee-based, Pembina has greater exposure to volumetric and commodity price fluctuations than its larger Canadian midstream peers. TC Energy has ~95% of its EBITDA regulated, while Enbridge is even more stable at ~98%. In particular, the company’s gas gathering and processing operations are exposed to underutilization as they can be impacted by production cuts at the wellhead. In general, the closer the pipeline is to the production site, the more exposure it has to commodity and volumetric risks.

Although Pembina has recently acquired a large international pipeline, with its new Cochin line, the majority of its infrastructure is regional primary oil and gas pipelines. As a less regulated business than its peers, Pembina has more cash flow volatility due to volume and commodity price fluctuations, but faster project approvals. As Pembina is a more regionally focused player with only one trans-border asset, its projects tend to stay out of the spotlight when compared to its larger industry peers. This project profile of smaller, more executable projects tends to mean fewer regulatory delays.

With CAD $3.1B in current liquidity and a BBB credit rating, Pembina has maintained a good balance sheet that has enabled the company to act quickly and execute on opportunistic acquisitions. Historically, Pembina has maintained a capital structure comprised of approximately 40% debt. Going forward, the company expects that half of future growth will be debt-funded which will tilt the capital structure to a more even balance of debt and equity. While the company’s debt may increase in the coming years, the firm is anticipating significant free cash flow growth that can be used to pay down debt if leverage were to become problematic in the future.

Investor Takeaways

Pembina is an ideal holding for long-term wealth generation due to its stable earnings, massive growth plans and business model that supports dividend growth. The company’s long-term contracts offer stable fee-based revenue that is ideally suited to support long-term dividend growth. Pembina’s recent growth through acquisitions and through the addition of incremental pipeline capacity has driven the company’s portion of fee-based revenue to 85% of 2019 EBITDA. Since 2009, Pembina has achieved an adjusted cash flow per share growth that has far outpaced its dividend growth rate. By having cash flow growth outpace dividend growth, Pembina has been able to maintain a lower payout ratio and fund significant capital projects. Pembina’s combination of stable earnings along with its dividend growth record gives the company all the characteristics of a future dividend aristocrat and an ideal monthly income stock.

Disclosure: I am/we are long TRP, ENB. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}