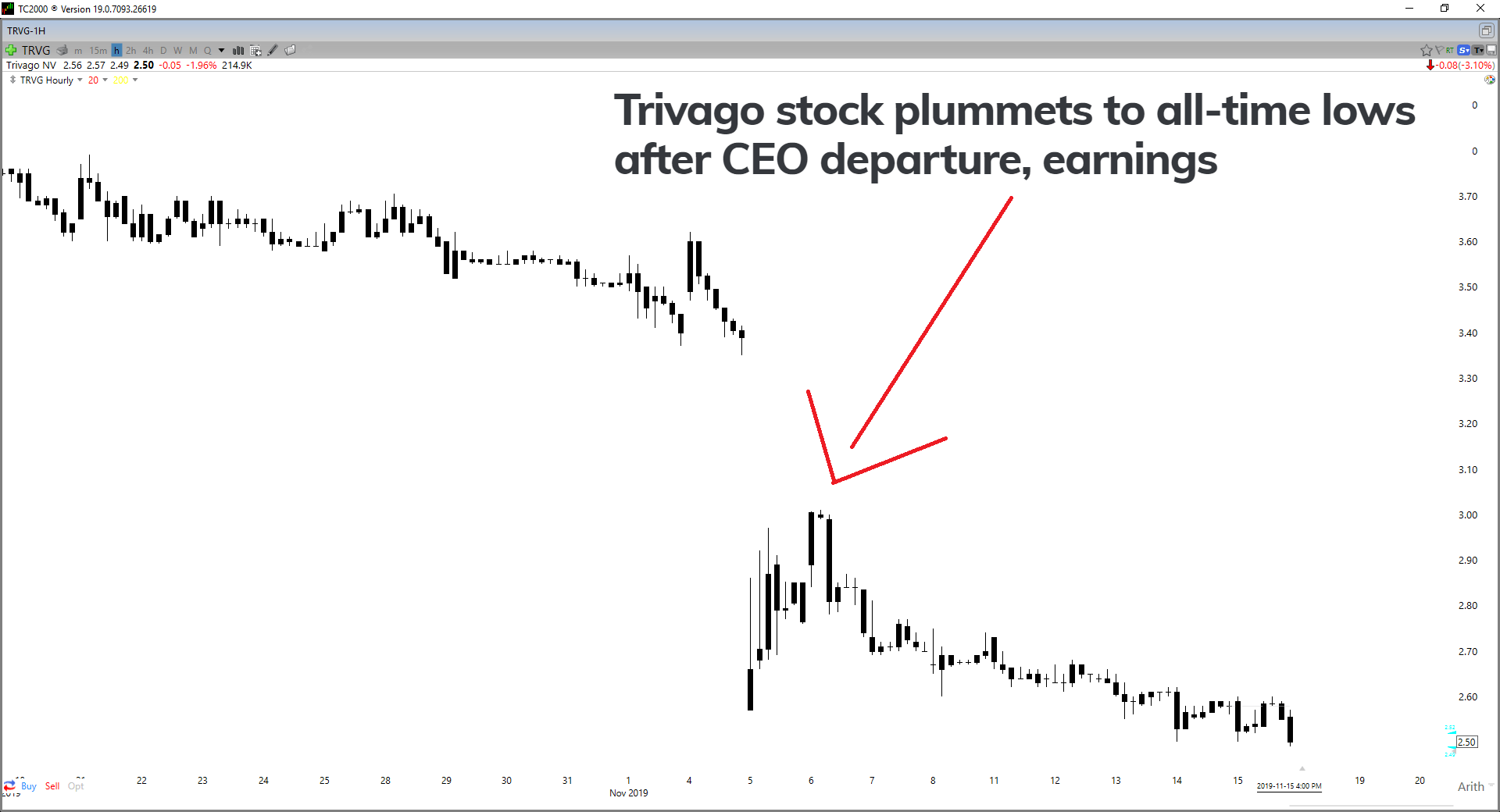

While the S&P-500 (SPY) has seen a strong start to November with a 3% gain just eleven trading days into the month, Trivago (TRVG) continues to go in the wrong direction. The company’s Q3 earnings report was yet another disastrous quarter, with high single-digit declines in revenues year-over-year, and news of a CEO switch-up, with Axel Hefer replacing Rolf Schrömgens. The disappointing performance over the past year should be of no surprise to investors, as cheap stocks that look too good to be true are often there for a reason. The market has an uncanny ability to sniff out companies that are going in the wrong direction, and I’ve never seen any reason to own a company that is seeing consistent declines in revenue year-over-year. While Trivago’s stock is beginning to head towards short-term oversold levels here, I see no reason to go fishing for a bottom. If I were holding the stock, I would be using any sharp rallies of 30% or more to exit my position. Any rallies of this magnitude will likely end up being oversold bounces within a bear market.

(Source: TC2000.com)

(Source: TC2000.com)

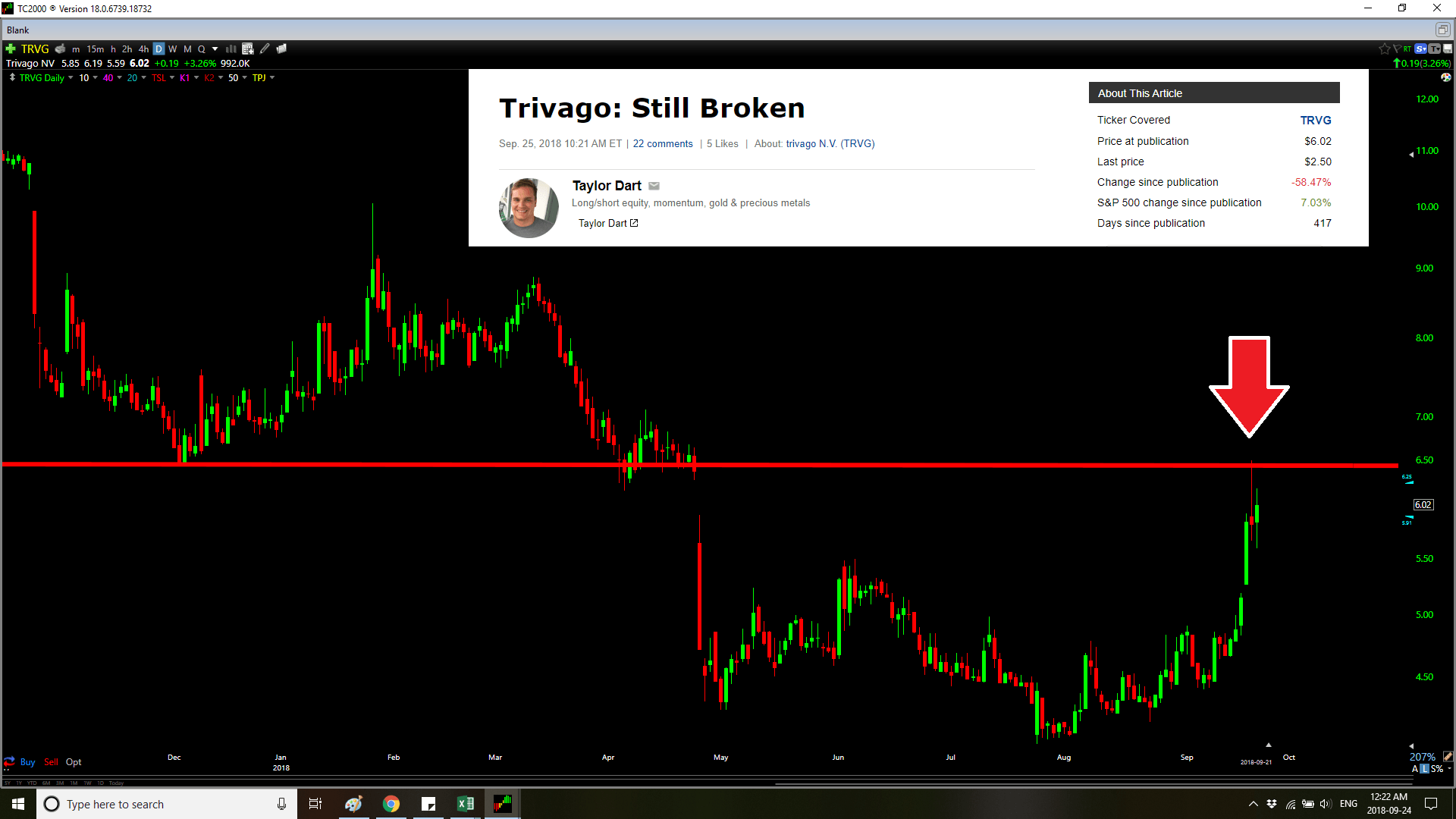

I first wrote on Trivago a little over a year ago in my article “Trivago: Still Broken,” and discussed that there was no reason to get excited about the strong rally at the time. While the stock was up 60% off of its lows, there were absolutely no signs of a turnaround in top-line growth. This suggested that the rally was most likely just a bounce to relieve oversold conditions and an opportunity for investors to exit while the going was good. This thesis has turned out to be right, with the $6.00 level now a distant memory as the stock trades at $2.50 just over a year later. The biggest problem with the Trivago story has been revenue growth, and the company cannot seem to turn this around. We are now nearly four years out from Trivago’s IPO debut, and it’s hard to see any path to consistent profitability until the company can manage to reverse the downtrend in quarterly revenues. While cost-cutting is one way to flip a company’s bottom-line to positive, it’s not a long-term plan to grow a company. Ultimately, this requires revenue growth.

(Source: TC2000.com, Seeking Alpha Premium)

(Source: TC2000.com, Seeking Alpha Premium)

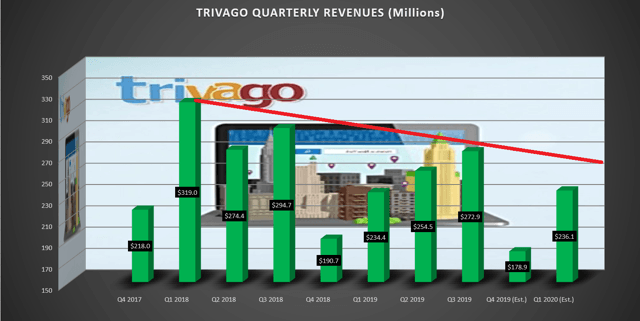

As the below chart I’ve built shows, we’ve seen no change in this trend yet. Trivago’s revenue growth for Q3 came in at $272.9 million, down 7% year-over-year, and the linear regression line for quarterly revenues is heading lower. Q4 2019 revenue estimates are expected to come in at $178.9 million, and this would mark yet another 2-year low in revenues for the company, below the prior low of $190.7 million reported in Q4 2018. While some value investors have pointed to Trivago being a buying opportunity late last year, I believe they are missing the forest for the trees. A profit over growth strategy like Trivago has been targeting can pay off, but ultimately we need growth in revenues to get excited about any turnaround. This is one area where Trivago is still unable to deliver. Let’s take a closer look at the growth metrics below:

(Source: YCharts.com)

(Source: YCharts.com)

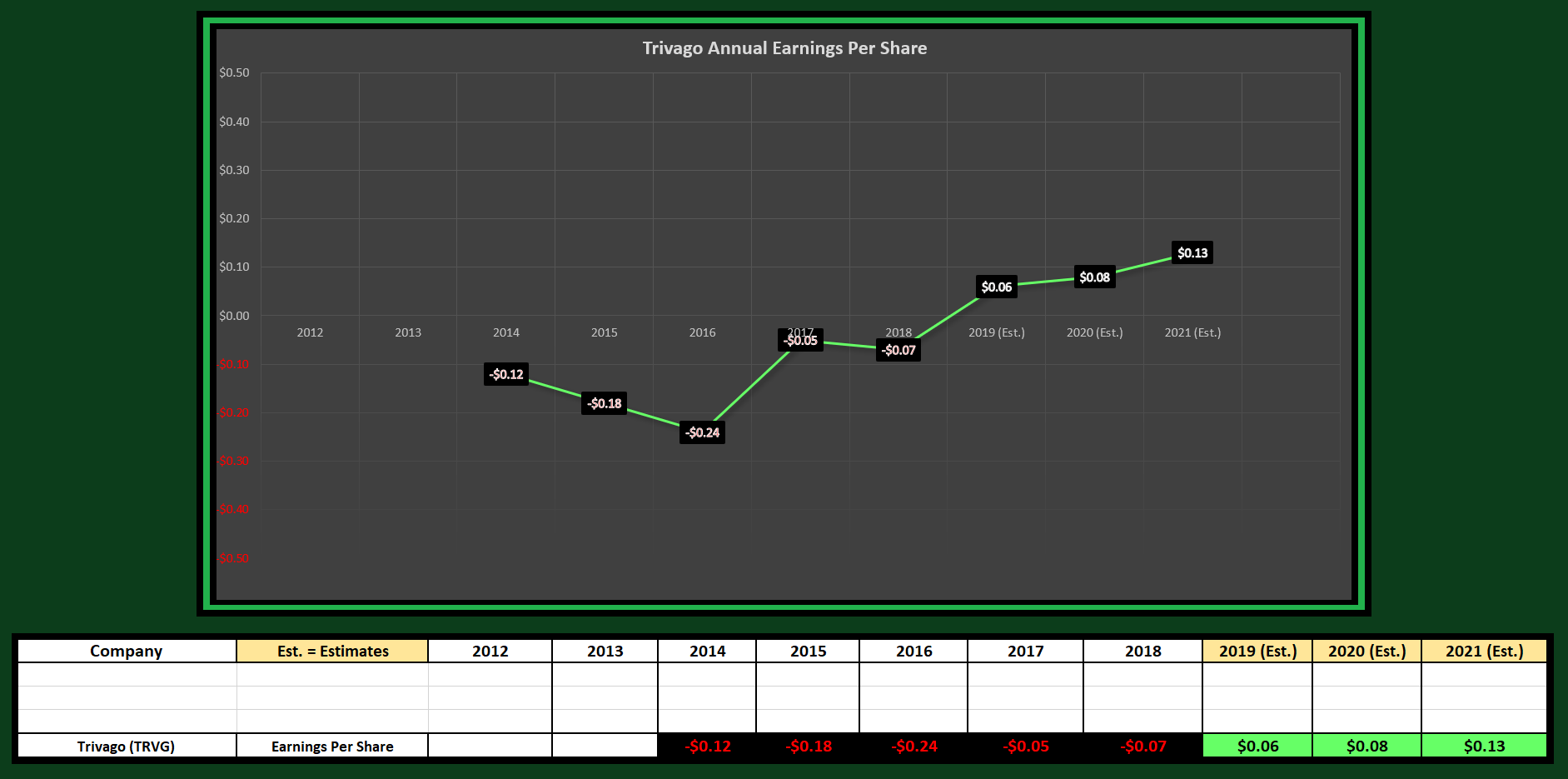

Taking a look at Trivago’s annual earnings per share, the company has posted net losses for five years in a row (2014 through 2018) and is expected to see its first year of positive earnings per share growth in FY-2019. While some investors are likely confused by the company’s terrible share price performance in its first year of positive earnings growth, they are overlooking the fact that EPS growth is not sustainable without robust revenue growth. While cost-cutting that driven this push towards profitability for the company, I always highly discount any turnarounds that come on the back of cost-cutting. Generally, extreme cost-cutting leads to competitors gaining the upper hand, even if it does look good on the bottom-line short-term. In a market that is highly competitive and continuously evolving, the best way to stay relevant in one’s industry is to grow sales consistently, and then use a portion of increasing sales on spending to hopefully innovate or out-do the competition.

As the below chart shows, Trivago is expected to post annual EPS growth of $0.06 for FY-2019, $0.08 for FY-2020, and $0.13 for FY-2021. This is an improvement from the trend of net losses, but I believe it’s masking the real problem, which is growth in revenues.

(Source: YCharts.com, Author’s Chart)

(Source: YCharts.com, Author’s Chart)

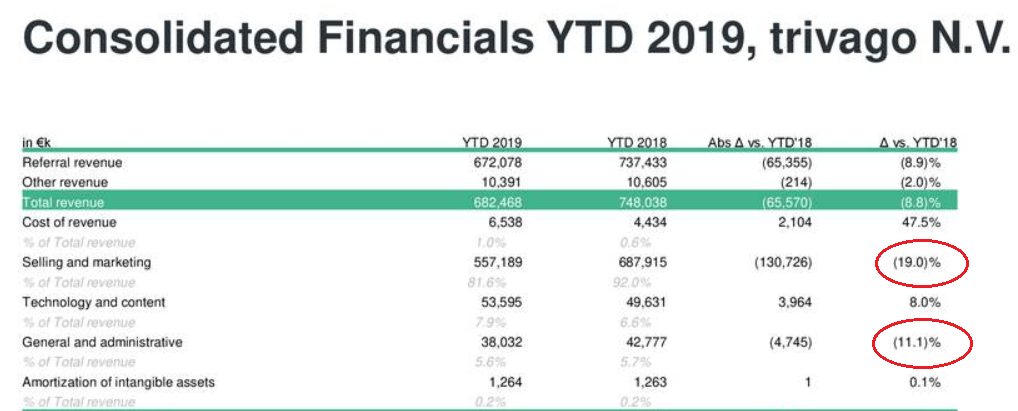

As the below table shows from the company’s Q3 earnings call, general and administrative expenses are down 11% year-over-year, with selling and marketing expenses down 19%. This savings of nearly 150 million euros is what’s helping the company to be profitable, but it’s coming at the cost of no real improvement in revenues. While there’s no guarantee that extra spend translates directly to the top-line, it’s also hard to imagine the company solidifying a sustainable turnaround in a period of cost-cutting. Based on this, I am not impressed at all with the flip to positive annual EPS. The story here has always been revenue growth, and there have been no improvements here yet.

(Source: Company’s Earnings Call Slides)

(Source: Company’s Earnings Call Slides)

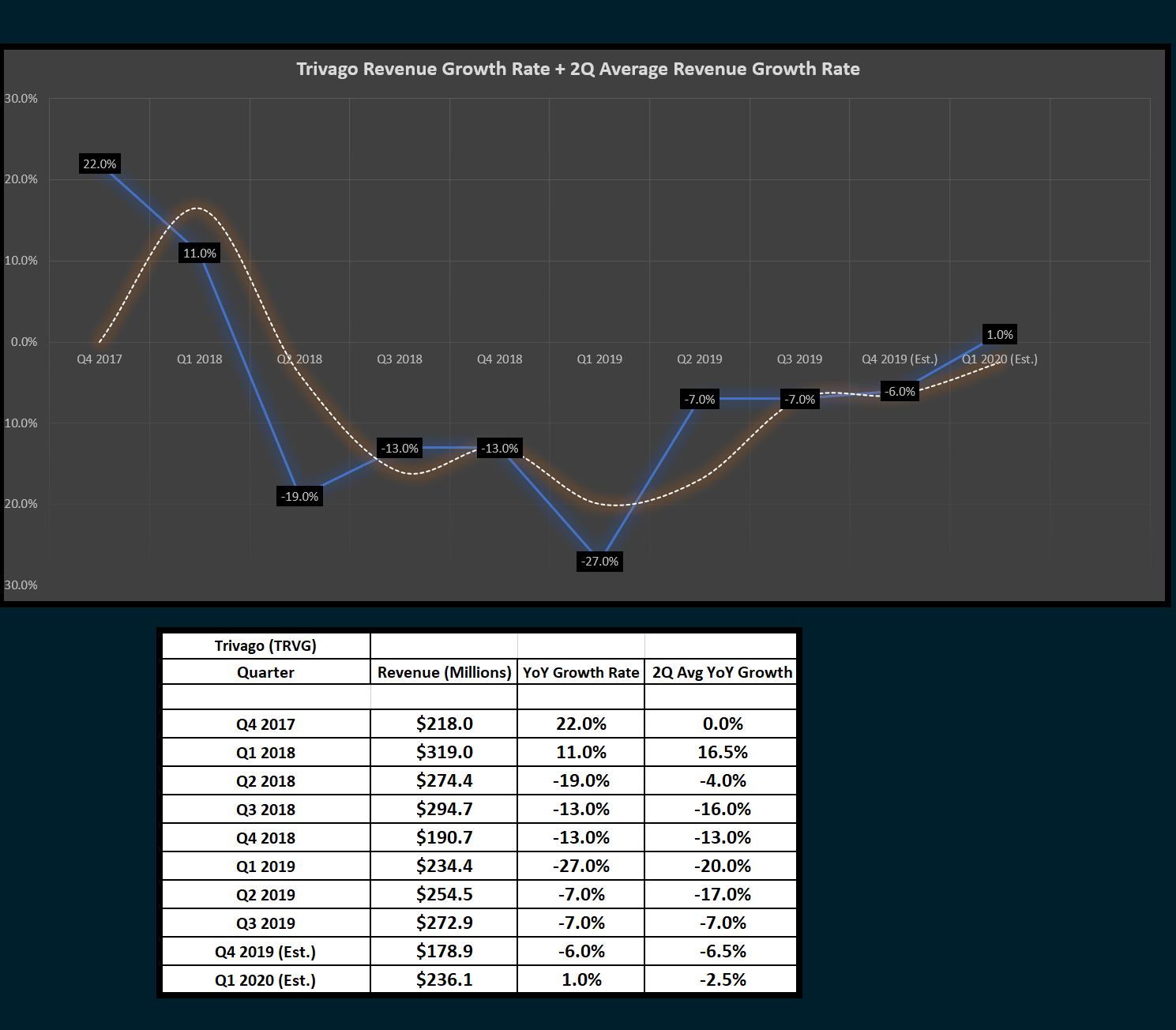

Taking a closer look at quarterly revenue growth rates below, we can see that Trivago has spent much of the past two years in the negative, with Q1 2019 being the worst quarter, with a 27% decline in revenues year-over-year. Q3 2019 was a narrower decline at (-) 7%, and Q4 2019 is expected to narrow further at (-) 6%. While it’s a good sign to see these year-over-year declines narrowing, it also must be put in context. The reason that we see narrower declines sequentially is that the company is up against easy comps from a disastrous fiscal 2018. With Q4 2018 revenues down 13%, it would be difficult unless Trivago’s business was falling off the map to see yet another double-digit decline. Therefore, while these year-over-year declines are narrowing, it’s nothing to be impressed with at all.

(Source: YCharts.com, Author’s Chart)

(Source: YCharts.com, Author’s Chart)

The blue line in the above chart represents the quarterly growth rate, while the white line represents the two-quarter average. I like to use a two-quarter average for revenue growth rates as it helps to smooth out any lumpy quarters and better dictates the overall trend. As we see, the two-quarter average is trending up and looks to have made a trough in Q1 2019. However, we still do not have any revenue growth; we only have a return from negative levels back to flat. Flat revenue growth after a period of low double-digit year-over-year declines is not anything to get excited about. It shows that things are stabilizing at these lower levels, but it doesn’t suggest a turnaround is in place. For investors to be confident of a turnaround, they should be looking for two consecutive quarters of double-digit revenue growth.

Based on the above growth metrics, I still see no reason to get involved in Trivago, even at this lower valuation. The company is currently trading at a forward P/E ratio of 31x based on the $0.08 forecasted for FY-2020, and there are much better companies than can be bought for 31x forward-earnings in all industries. While the company’s transition to positive EPS may look attractive to investors, it’s the revenue growth that’s the problem here. It is nothing special to achieve profitability after cutting costs substantially, and the only turnarounds worth banking on are those with revenue growth present. Let’s take a look below and see if the technical picture is any better:

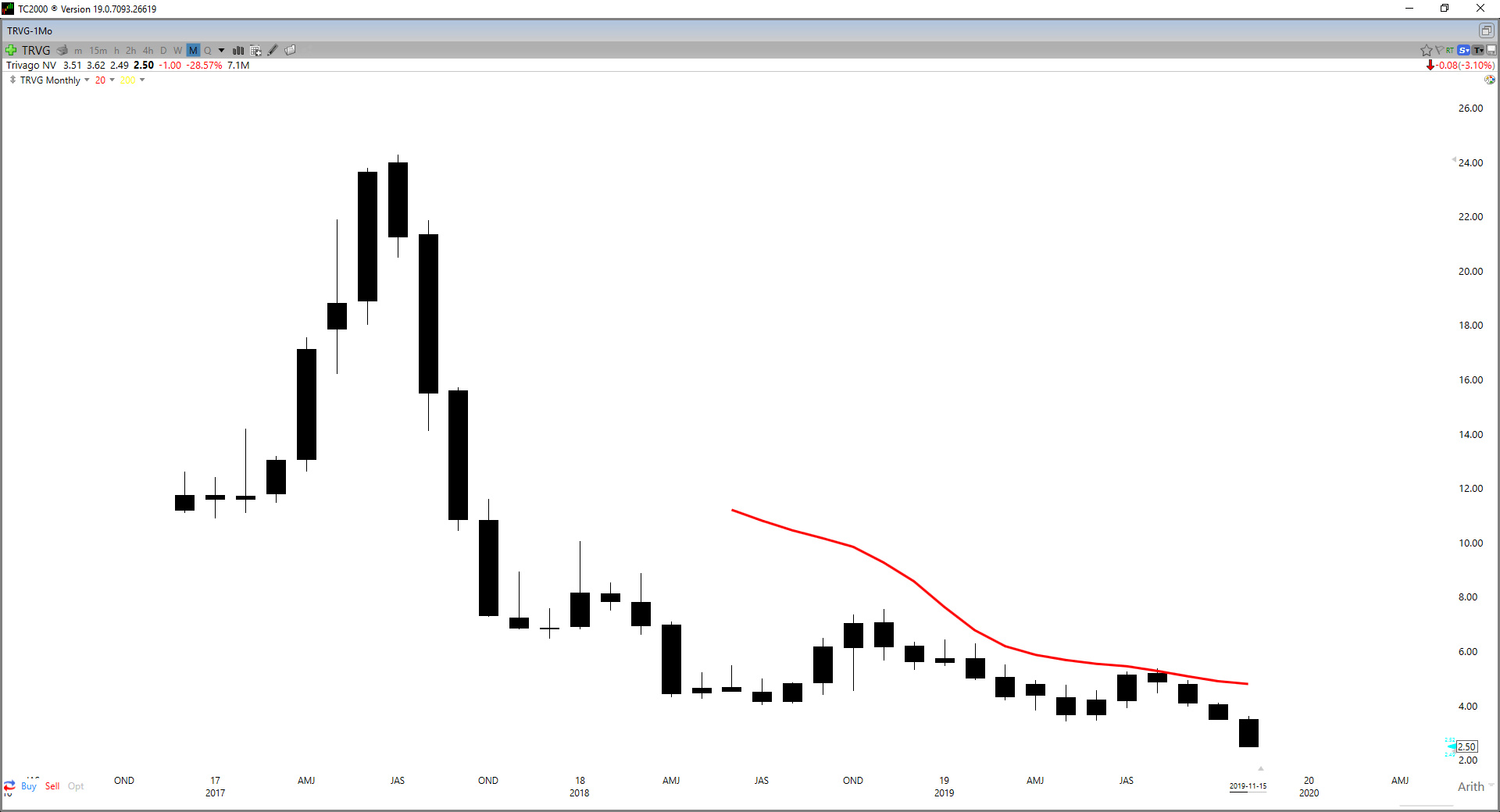

As the below monthly chart shows, an investment in Trivago has made no sense at any point in the past two years. Trivago has continued to trade below its 20-month moving average, and this is my leading barometer for the long-term trend. There are zero reasons to get involved in a stock below its 20-month moving average (red line), and this simple rule would have kept investors away from Trivago stock. As of Q3, Trivago has now headed to yet another new all-time monthly low. Generally, stocks making new all-time lows are not good long candidates.

(Source: TC2000.com)

(Source: TC2000.com)

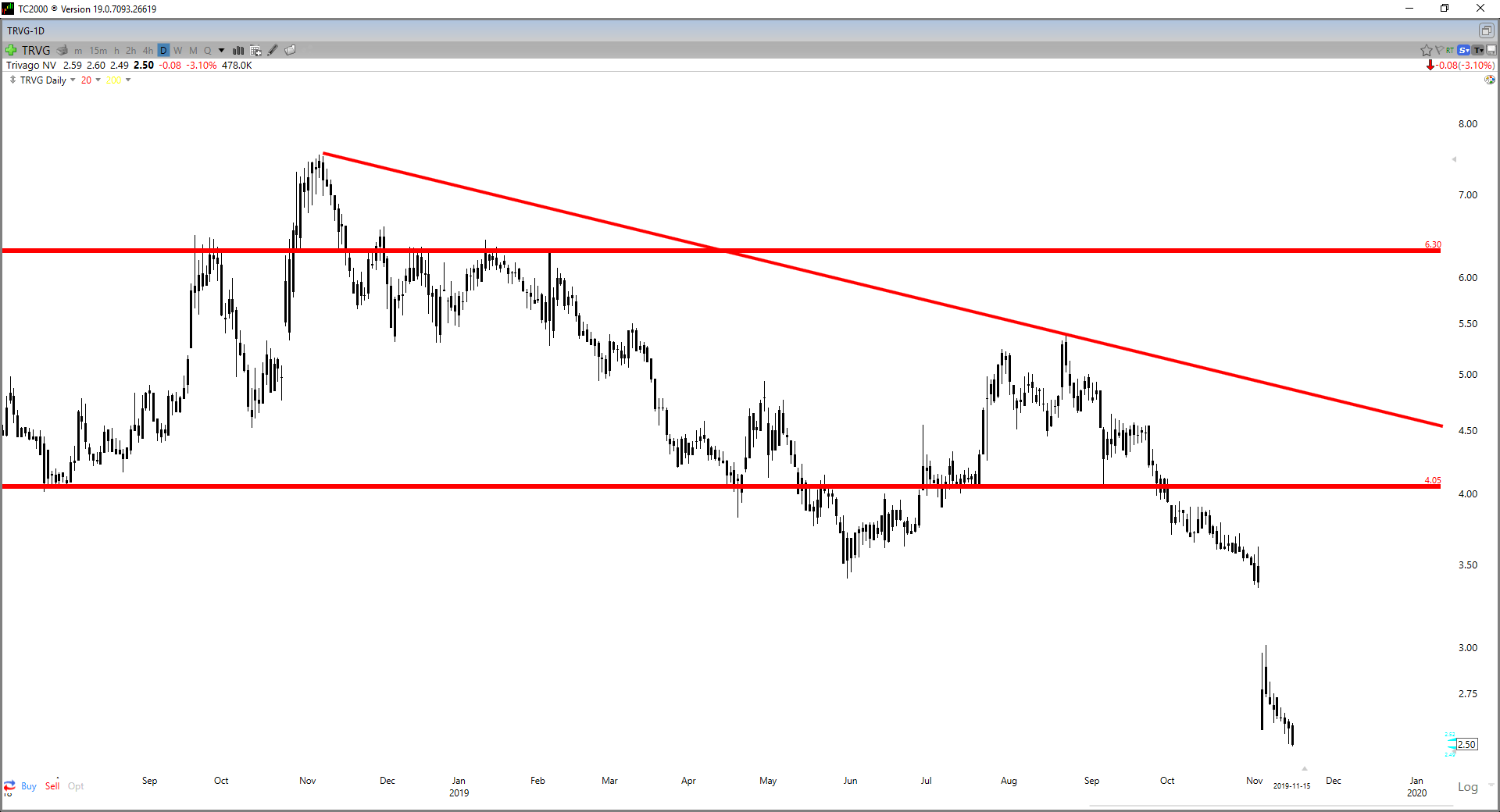

If we zoom into the daily chart, we can see resistance levels stacked overhead for the stock. Lower resistance sits at $4.05, with strong resistance at $6.30. While a bounce in Trivago stock is possible after a waterfall decline of 50% since August, I would view this as a selling opportunity. Even if Trivago were to bounce 30% or more, it would do absolutely nothing to fix this technical picture. This is because this would still mark a trend of lower highs and lower lows. If the stock were to head back to the $4.00 level, this would be a gift for investors looking to exit their positions.

(Source: TC2000.com)

(Source: TC2000.com)

To summarize, I see no reason to go bottom-fishing on Trivago here, and I would use sharp rallies to exit my position if I was holding in the stock. The company’s efforts to move towards profitability have worked but have come at the cost of lower spending. This has left revenue growth rates in the negative on a year-over-year basis. The stock may end up getting bid up in Q4 and Q1 after posting narrower declines year-over-year in revenues, but I would view this as an opportunity to sell the stock. Sustainable turnarounds are not built on cost-cutting, and I see no signs of a turnaround here yet in Trivago. Sharp rallies are possible, but they are selling opportunities.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}