This article was coproduced with Williams Equity Research.

It’s rare to watch dominoes fall in real time. Typically, it’s only after a series of events that we’re able to ascertain the collapse of a system.

For movie theater companies and their property owners, the delay of the new James Bond movie release, No Time to Die, appears to have been the straw that broke the camel’s back.

I’m kind of bummed, because I’m a huge “007” fan. (I even used my all-time favorite movie, Live and Let Die, for the title.)

As for Williams Equity Research (WER), he’s visited his local Regal theatre twice since they reopened. And he has some things to share on the subject…

Here at iREIT on Alpha, we’ve covered EPR Properties (EPR) several times in the past – usually by subscriber request. Plus, we’ve discussed the status of retail and movie theaters several times in the interim.

With recent news being what it’s been though, it’s time to address the latter again. Because there’s been yet another fissure in the struggling, retail-sensitive operators.

Given that EPR isn’t part of our model portfolio – and with now obvious good reason – this will be more succinct. It isn’t designed to be a complete firm overview.

(Source)

Movie Theater Apocalypse

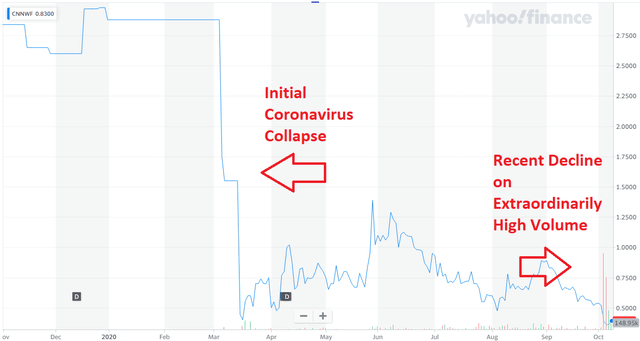

On October 5, Cineworld Group – which owns several movie theater brands, including Regal – announced the closure of hundreds of theaters worldwide on Oct. 5.

The OTC stock fell nearly 60% after the announcement, which is enormous. But it appears less dramatic on a one-year chart.

(Source: Yahoo Finance & WER)

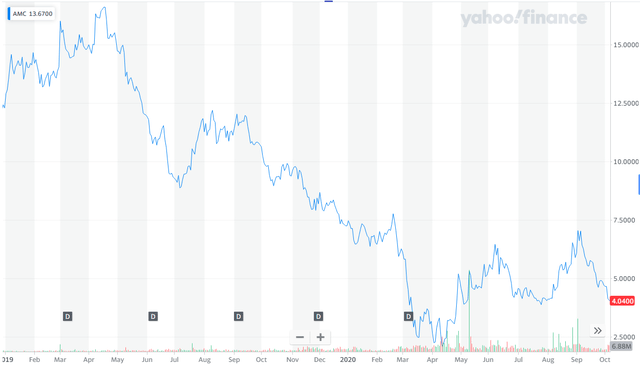

AMC Entertainment Holdings (AMC), for its part, has held up better but is still down significantly in the past 12 months.

(Source: Yahoo Finance)

Its market capitalization is now under $500 million, and Moody’s just reviewed its credit standing:

“AMC’s Caa3 corporate family rating (CFR) reflects the company’s materially weakened operating and financial performance, and the possibility of another near-term default following the July 2020 distressed debt exchange, which Moody’s viewed as a deemed default. AMC has suffered from significant revenue losses during the five-month forced closure of its global theatre circuit from mid-March to mid-August 2020 due to the coronavirus pandemic.”

S&P, meanwhile, downgraded it to CCC- on Oct. 5. Fourth quarter ticket sales estimates are expected to be down 85% year-over-year. And, honestly? It’s hard to see AMC lasting more than six months without a dramatic change.

Yet its position is somehow stronger than that of Cineworld, which announced this week that it’s:

“… close to hiring PJT Partners Inc. for advice as the theater company prepares to negotiate an overhaul of its debts with creditors.”

As such, 45,000 jobs are on the line.

Cineworld’s $2.7 billion term loan fell over 10% to $0.57 on the dollar, leaving it – and AMC alike – on the precipice of a total collapse. If they did go completely bankrupt, their better-performing locations would be scooped up by a distressed buyer and likely remain operational.

Who knows about the rest.

A Poor Showing

With the delay of No Time to Die – now set to debut in April 2021 – optimistic assumptions regarding the movie theater industry going into the holiday season have evaporated.

It goes without saying that this impacts EPR.

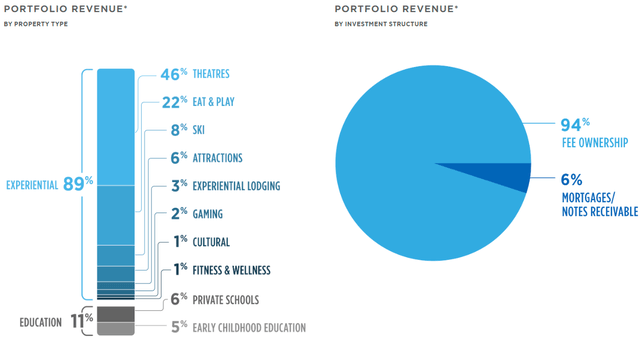

Portfolio and Cash Flow

(Source: EPR)

Forty-six percent of EPR’s annual revenue have traditionally come from theaters. So it was semi-good news (or at least not catastrophic) that 71% of those were open as of Sept. 11.

We don’t know what that figure will decline to now, but we do have clues.

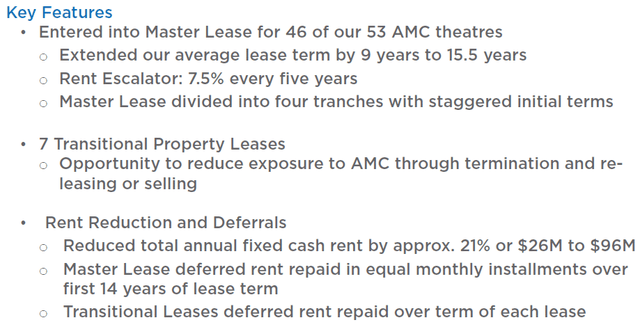

For instance, AMC’s lease agreement baked in permanent rent redactions prior to the recent negative news. That reduction represented 5%-7% of pre COVID-19 cash rent per EPR’s management.

(Source: September 2020 Investor Presentation)

EPR’s management took the steps above to combat this weakness, though it’s difficult to see the agreement holding if theaters close completely through the end of the year.

The primary short-term risk is further reduction in rents, of course. And the initial figure of 21% means there’s a lot of downside still on the table.

Long term, it’s a question of what to do with any vacant buildings that aren’t quickly filled by other operators – hardly an easy task.

Unlike Realty Income (O), which has only slight exposure to theaters, a rock-solid financial position, and an A3 rated balance sheet, EPR’s balance sheet and credit rating doesn’t allow for tons of capital and time spent on trying to redevelop even a meaningful fraction of its 180 theaters.

Quarterly funds from operations (FFO) peaked at $1.49 in Q3-19, fell to $0.97 in Q1-20, and came in at $0.41 in Q2-20. And consider that, Q1’s figure includes rent that was recognized but not actually received.

The real cash flow per share in Q2 was approximately $0.35 based on our independent calculations.

It’s difficult to balance the reopening of many of EPR’s other segments against the theater closures. Best-case-scenario, EPR manages to collect the same rents in Q3 and Q4 as it did in Q2.

And while things could improve significantly in 2021, that needs to be viewed through a realistic lens.

EPR’s Box-Office Balance Sheet

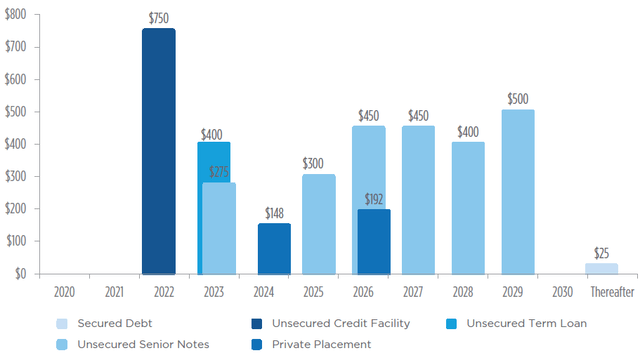

EPR wisely borrowed $750 million on its revolving credit facility going into the crisis. It also suspended both its dividend and stock-repurchase program as rent collections and cash flow crashed in late Q1.

(Source: September 2020 Investor Presentation)

EPR is at serious risk of a downgrade into junk territory. We’d be seriously surprised if it’s still rated investment-grade next year.

(Source: September 2020 Investor Presentation)

That won’t make refinancing the $750 million in debt coming due in 2022 any easier. And 2023 isn’t materially better, with $275 million and $400 million in secured debt and unsecured senior notes maturing.

Unlike several more solid retail-oriented REITs – such as Realty Income, Federal Realty (FRT), and Simon Property Group (SPG) – EPR’s financial position is a major concern.

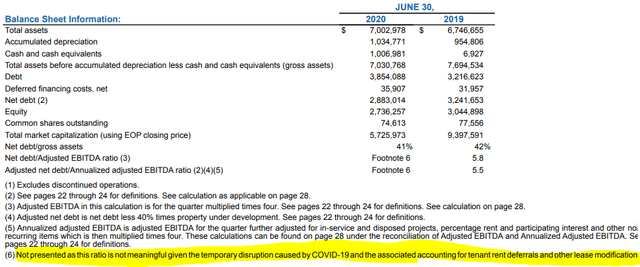

Net debt to gross assets was 41% as of the end of Q2, which is manageable, if the ship is steered just right. However, its earnings before interest, taxes, depreciation, and amortization (EBITDA)-related debt ratios are literally off the charts.

(Source: EPR Q2 Supplemental)

Management says “this ratio is not meaningful given the temporary disruption caused by COVID-19.” But we doubt the rating agencies will agree.

Keen analysts will still be doing the math, and net debt/EBITDA will be >10x in the second half of 2020.

Personal Experience

As previously mentioned, WER’s lead portfolio manager visited two Regal theaters in recent weeks as they reopened in his area. He’s a long-term big brother in the Big Brothers Big Sisters program, and the child he mentors enjoys the movies.

In their first trip about five weeks ago, there were a total of four other people in the theater for the duration of the movie. And while walking around the facility, he spotted one couple.

Just last weekend, when they returned, they were the only people in the entire theater.

You can easily imagine then that concession sales – which are a critical part of overall sales – also are down in general, not to mention in proportion to ticket sales, though this isn’t completely due to customer concerns.

In both visits, WER’s portfolio manager found that product availability was less than 50% the norm. His “little brother” wanted food items that normally would have been available but weren’t.

For those familiar with elementary school-aged children, it should come as no surprise that the child promptly decided he was no longer hungry and ordered nothing at all. As for WER, he usually gets a low calorie/healthier drink option… which weren’t available either.

In the end, total expenditures were less than half of what he’d typically spend.

In Conclusion…

(Source: September 2020 Investor Presentation)

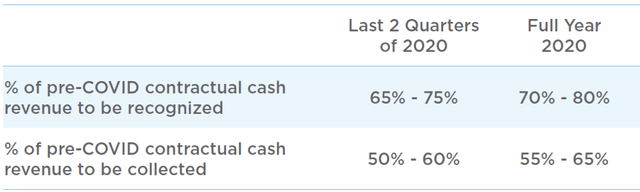

EPR was already looking at 50%-60% of cash rent collected before two of the largest movie theater operators voluntarily closed their doors. As mentioned in the cash flow section, this equates to about $1.40 annually in cash flow before a potential recovery in 2021 toward $2.

That assumes we don’t see a total collapse here, which seems more and more likely.

As of Oct. 8’s close, we’re looking at an 18.1x cash flow multiple. Put bluntly, an investment in EPR at today’s levels doesn’t make sense to us.

It’s a distressed or near-distressed company trading at higher multiples than many investment-grade REITs with lower re-leasing risk, better financials, and higher rent collections.

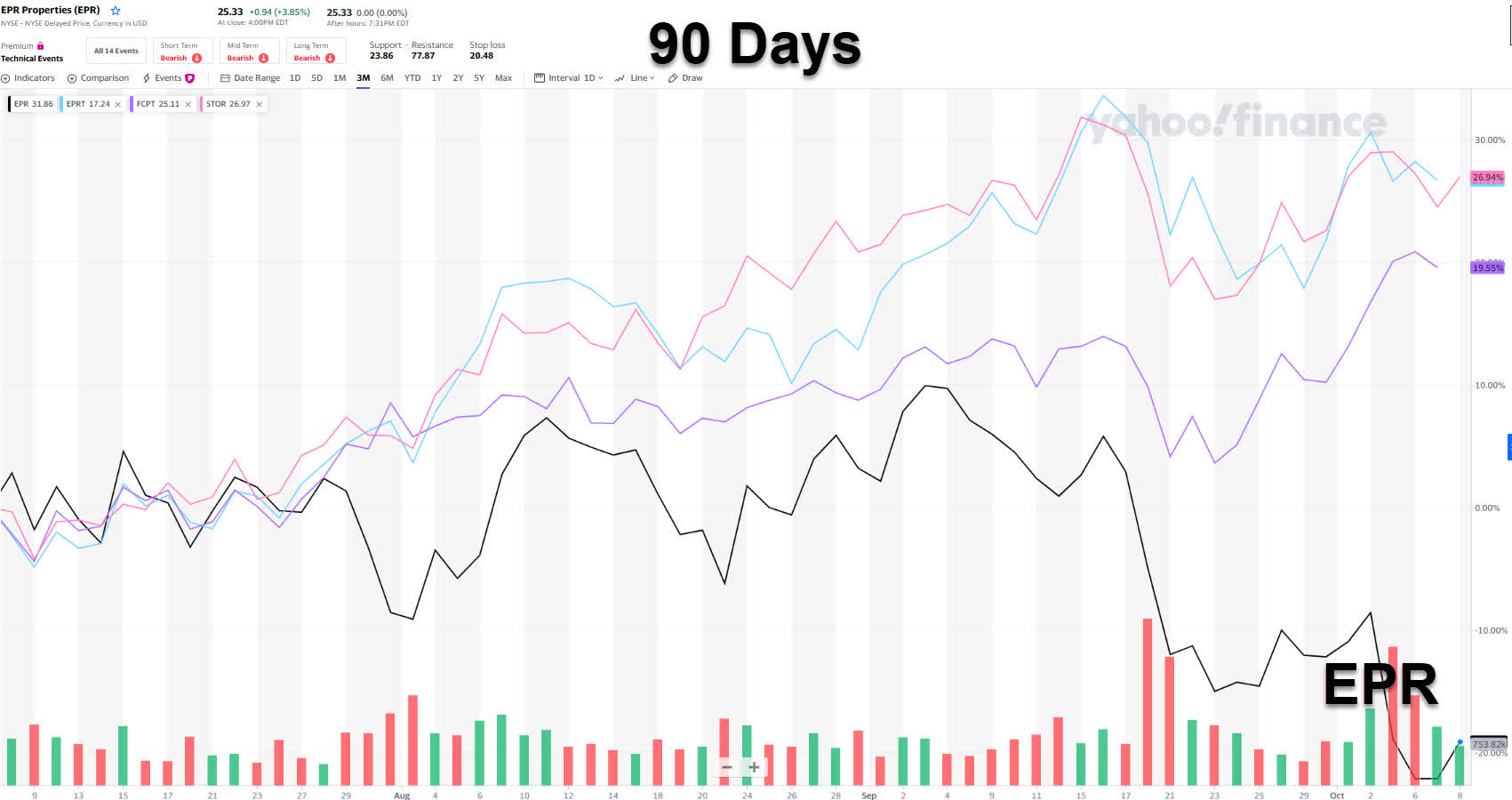

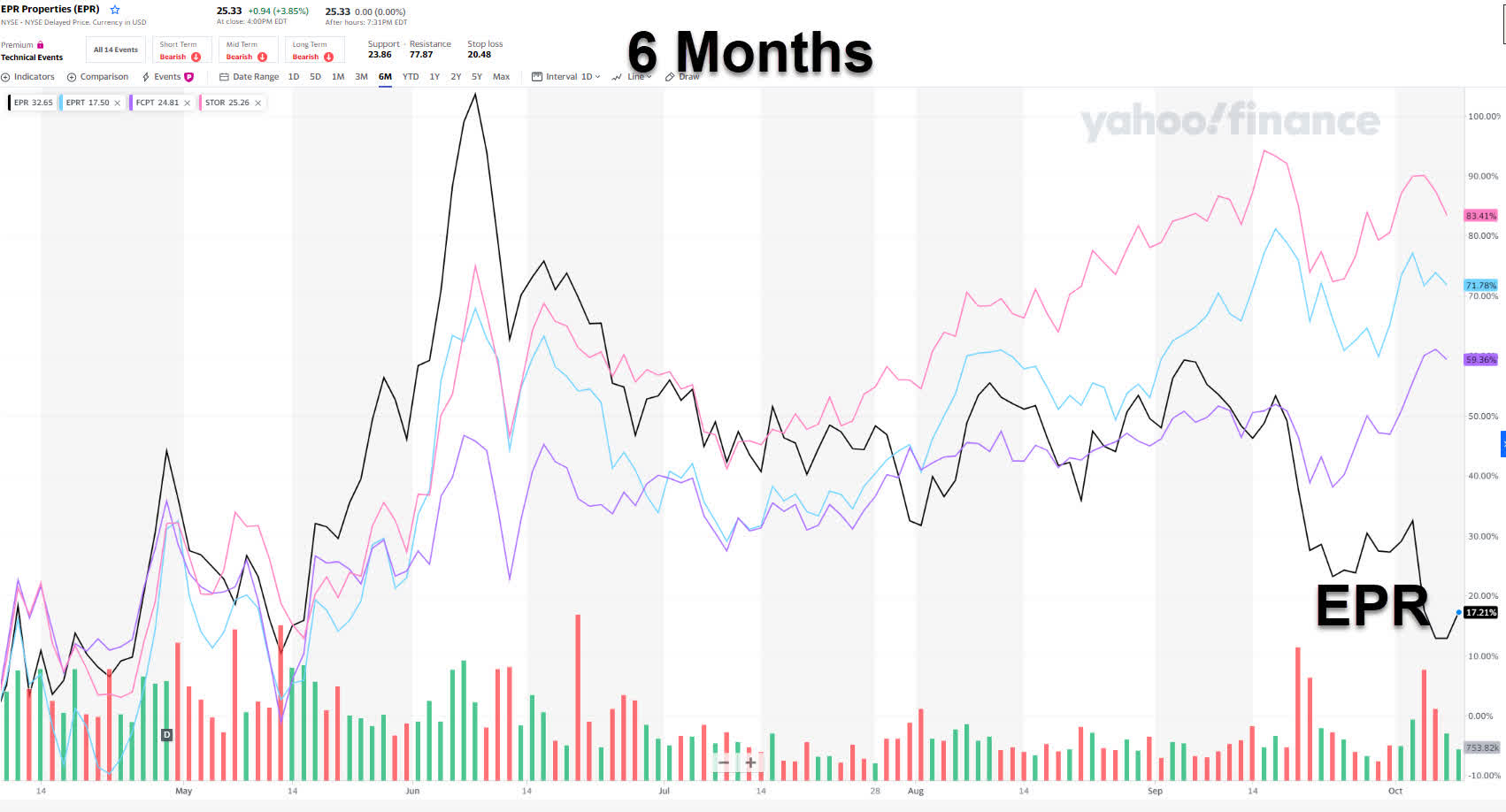

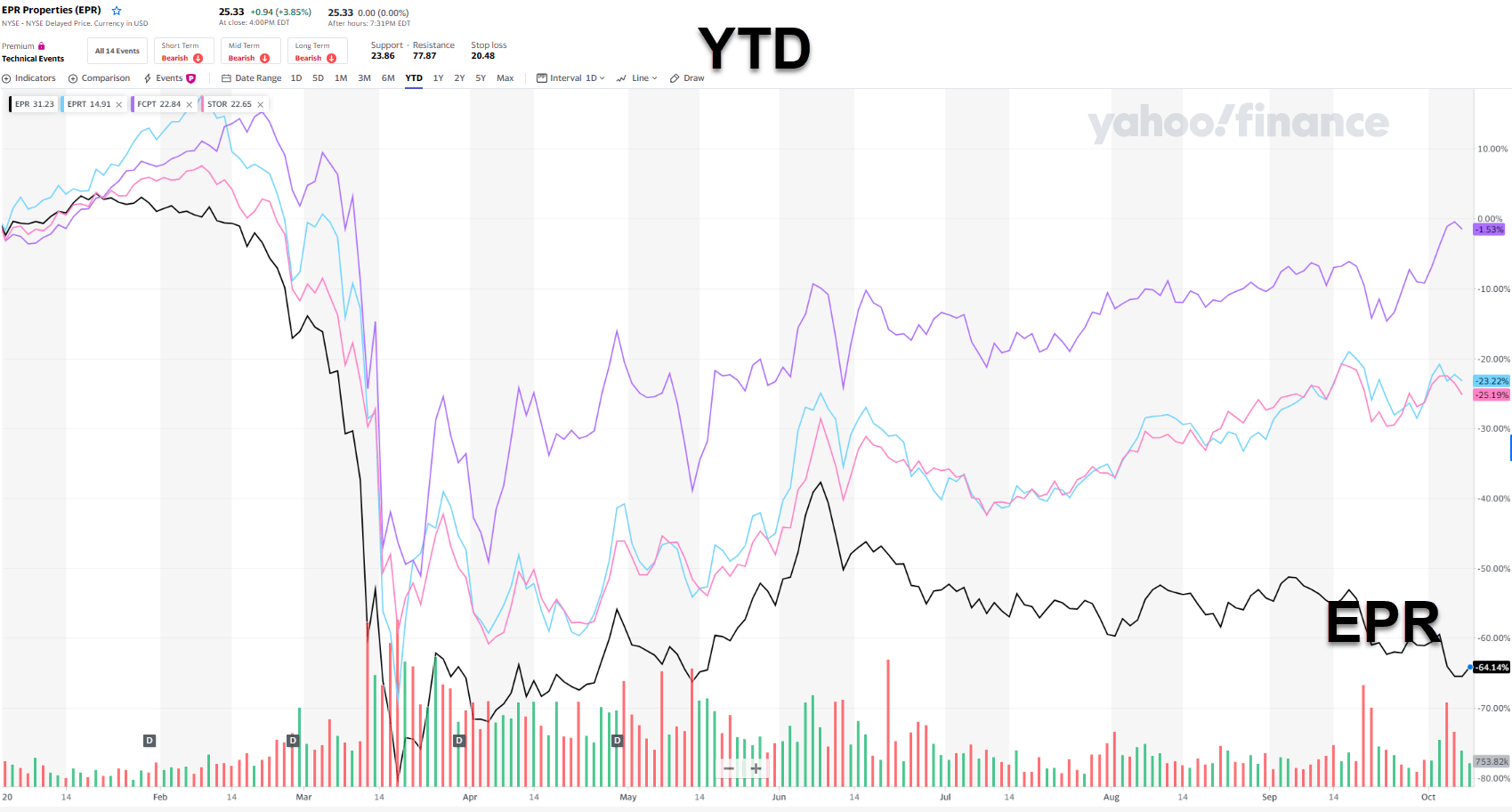

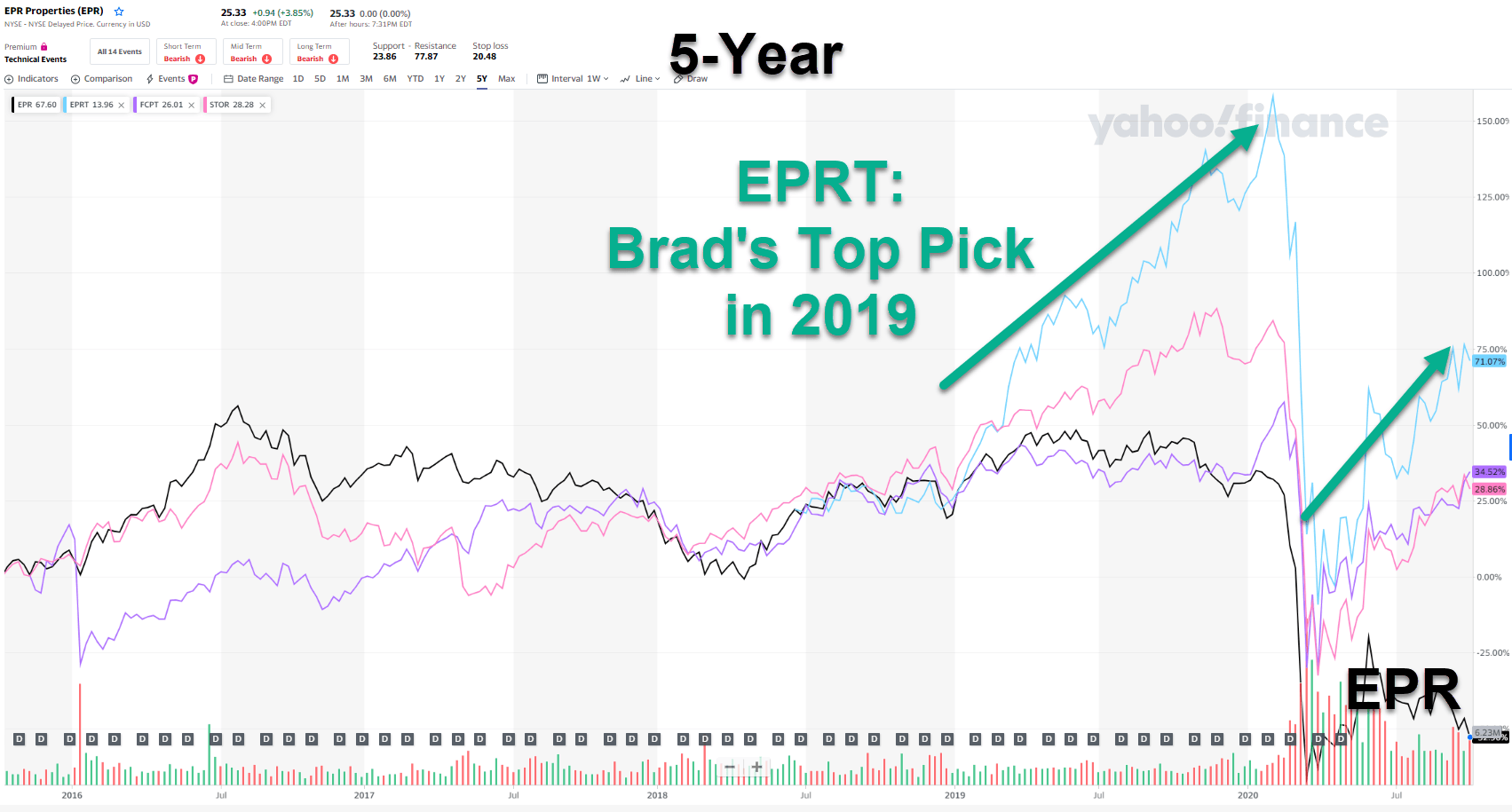

We maintain a Sell on EPR shares, much preferring our Cash Is King Portfolio picks – which have “smoked” EPR by a wide margin:

- Four Corners Property (FCPT), up 87.6%

- Essential Properties (EPRT), up 85%

- Store Capital (STOR), up 48.9%.

(Source: Yahoo Finance)

(Source: Yahoo Finance)

(Source: Yahoo Finance)

(Source: Yahoo Finance)

In closing…

I truly wish you the very best…be safe…and…

“…if this ever changing world in which we’re living… Makes you give in and cry…

… Say live and let die!

Author’s note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Join the iREIT Revolution! (2-Week FREE Trial)

At iREIT, we’re committed to assisting investors navigate the REIT sector. As part of this commitment, we recently launched our newest quality scoring tool called iREIT IQ. This automated model can be used for comparing the “moats” for over 150 equity REITs and screening based upon all traditional valuation metrics.

Join iREIT NOW and get 10% off and get Brad’s book for FREE!

* Listen to our Ground Up Podcast * 2-week free trial * free REIT book *

Disclosure: I am/we are long O, FCPT, EPRT, STOR, SRC, NTST, PINE. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}