Even prior to the pandemic, effective rent growth was waning in San Francisco. In the immediate future, additional rent decreases are likely.

In economics, the sensitivity of aggregate demand for a product or service to changes in price is defined as its “elasticity.” The elasticity of demand for nonessential goods or goods with a number of ready substitutes is high. Even a small increase in price will produce a large decrease in demand. Conversely, a relatively large price change in the cost of an essential or prized luxury good for which few substitutes exist may have little effect on demand for it.

San Francisco real estate is a highly inelastic good. The Bay Area’s potent combination of natural beauty, sublime climate and unique culture make it one of the most coveted destinations in the world. By the same token, its compact size, high population density, seismic risks and antipathy to development constrain supply. For all practical purposes, housing prices are limited by the income that residents can expect to earn rather than the normal interplay of producers and consumers.

The innovation and wealth creation generated by the high tech industry added a complex new variable to the equation. More wealth was created during the last 10 years in the 40 miles that lie between the Golden Gate and San Jose than in any location in human history. Ambitious, talented people from across the globe come to compete in the digital gold rush for reasons entirely divorced from Northern California’s renowned charms. The price of real estate and apartment rents soared accordingly.

What happens to the price of an inelastic good when viable substitutes become available and consumer incomes plunge? The San Francisco market is in the process of revealing an answer.

The work-from-home phenomenon makes participation in San Francisco’s lucrative marketplace feasible without paying the real estate toll. At the same time, the viral pandemic has diminished the appeal of urban living, even here, and upended the livelihoods of tenants working in the city’s tourism and leisure sectors, rendering this luxury good at least temporarily beyond their means.

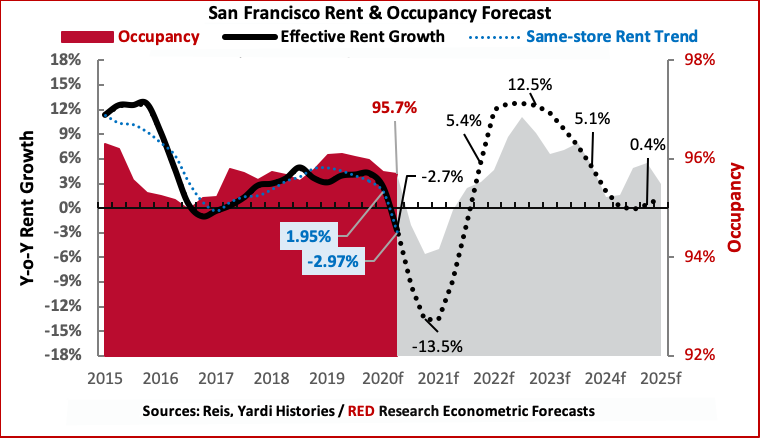

So far, the impact on apartment occupancy has been surprisingly small, at least in the professionally managed segment of the market. Yes, metro occupancy is down from its recent 96.17 percent (Reis) peak set in May 2019; but most of the losses were incurred before March, when economic lockdowns were first imposed. Indeed, occupied stock decreased by only 80 units (or 0.07 percent) between February and June.

Rents are another matter. Even before the pandemic, owner pricing power appeared to erode. Average rent among a same-store sample consisting of 71,341 units surveyed by Yardi peaked in September and declined sequentially every month thereafter through July. Defensive discounting accelerated in April and reached a crescendo in June, when average unit rent fell 1.41 percent from May and 4.94 percent from June 2019. Prices declined another 0.53 percent (5.66 percent year on year) in July.

Property owners are experiencing the downside of selling a scarce product that commands a premium price due to demand inelasticity. Prices can tumble quickly and materially when viable substitutes arise, even when consumers benefit from substantial government subsidies. A small dip in demand may give rise to a significant decrease in price.

Further rent decreases are likely. Forecasting the magnitude of the decline using standard linear regression techniques when the pricing function is radically nonlinear is a dicey proposition, especially when the macroeconomic environment is uncertain. Although RED Capital Research’s San Francisco rent model is relatively robust (adjusted R2 = 94.6 percent), the model’s standard error (1.66 percent) is the highest of any of the 50 markets we model. With this caveat, rents appear likely to drop another 10 percent (±5 percent) from June levels before stabilizing in early 2021, even under an optimistic V-shaped recovery scenario.

Completing sales transactions in this environment will be challenging. Purchase cap rates for institutional quality properties haven’t budged from the high-3 percent to low-4 percent range observed since 2019. Smaller assets favored by family offices and owner/managers trade at considerably lower yields, in some instances below 3 percent. Generating adequate returns over an intermediate-term holding period under these circumstances will be difficult. The downside risk to income performance and to rising financing costs and cap rates cannot be ignored when the wages of monetary stimulus are paid.

Owning an asset in a market with inelastic pricing characteristics has distinct advantages, as dozens of new real estate moguls in the Bay Area can attest. Entrée into the market isn’t easy or inexpensive; however, timing is critical. Buyers waiting for distressed assets to become available are likely to be disappointed. On the other hand, those who buy in haste may repent at their leisure. Few buyers and sellers are likely to find mutually agreeable prices in the second half of this year, but 2021 promises to be very interesting indeed. Pass the popcorn.

— By Daniel J. Hogan, ORIX Real Estate Capital’s Managing Director for Research. RED Mortgage Capital, a division of ORIX Real Estate Capital LLC, is a content partner of REBusinessOnline. The views expressed herein are those of the author and do not necessarily reflect the views for RED Capital Group or of the author’s colleagues at RED. For further analysis from RED Capital Group, click here![]() .

.

For Hogan’s insight into other markets, click here.

{kind=link}