{kind=link}

Shares of Union Pacific Corp. (UNP) are basically flat for the year, down about 0.4%. That said, they’re up about 53% since the market cratered in late March. In spite of the fact that shares have rallied nicely, I think they still represent good value at current levels. The company has a strong history of generating earnings growth, and also of rewarding shareholders with growing dividends. In this article, I will outline my bullish argument by looking at the most relevant fundamental and technical aspects of the stock.

The Past

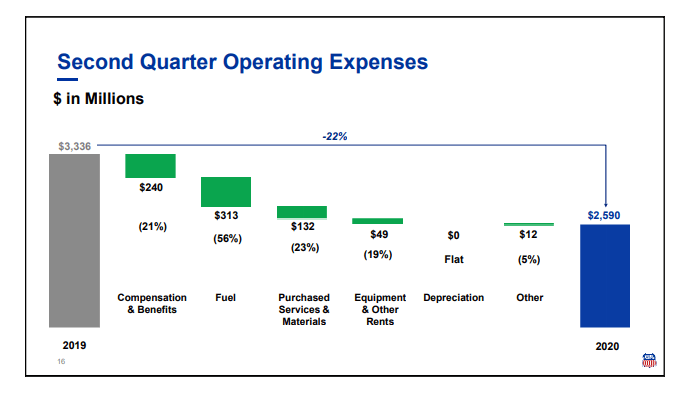

Revenue is down just under 14% compared to this time last year, but net income is down “only” 12% which suggests that the company has been able to dynamically reduce expenses somewhat. From the latest earnings deck, we see the breakdown of how the company was able to dynamically react to the slowdown in demand.

In spite of this slowdown in demand, management has maintained the dividend, which has grown by 10.25% since this time last year. The fact that the payout ratio is only about 51% indicates to me that the dividend is still safe, in spite of the slowdown in demand. Also, I think the dividend offers some support for the shares, so as long as it’s not imperiled, I think the shares will remain well bid.

It’s important to put the recent softness in a broader historical context. When the company has hit soft patches in the past, the shares would falter for a time, but would always come back as the business returned to growth. For example, in spite of the 17% drop in revenue between 2014 and 2016, the shares are up about 67% since January of 2017. If history is any guide here, it suggests that softness represents a buying opportunity.

The Future

The past is important to remember because it offers evidence of management’s ability (or not) to grow earnings and reward shareholders. Obviously investors are more concerned about the future than the past, though, so I should spend some time talking about what the likely future will be here.

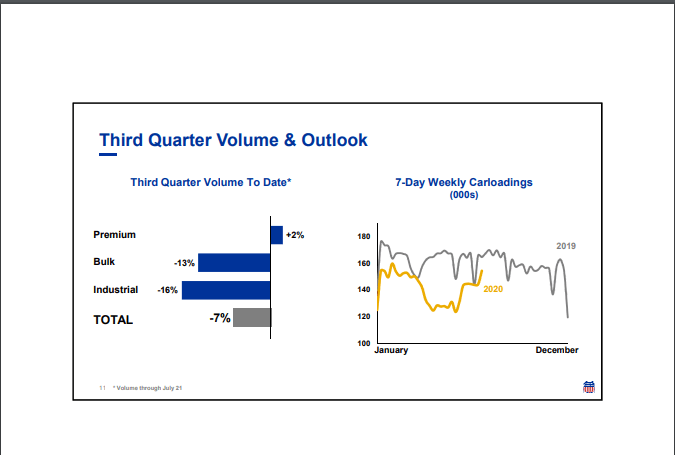

For the next quarter, Union Pacific is forecasting a volume decline of about 7% per the following page from their latest earnings call.

I think investors react negatively to surprises, and at least softness later in the year won’t come as a surprise to the market.

When trying to anticipate the future, I prefer to use the Forward P/E Ratio (current stock’s price over its “expected” earnings per share) rather than historical P/E to gauge a company’s expected future earnings power. The forward PE is just that: forward looking, as opposed to the trailing PE. A high forward P/E ratio means that investors are anticipating higher growth in the future and are willing to pay more for future earnings – momentum investing is all about following the trend (perceived or real). At the moment, in spite of the earnings softness, the market is forecasting a forward PE of just under 24 (Union Pacific Forward PE Ratio). In comparison, the forward PE for the SP500 currently stands at 21.94. The forward P/E for UNP is higher than that of the index, suggesting that the markets are expecting an earnings growth rate for the company that is higher than that of the broader markets.

The risk to using this method to forecast the future is obvious enough. It depends on the company’s ability to grow earnings at the rate forecast by the market. If the market’s forecast is too sanguine, the stock will probably drop in price. That said, we consider the risk of this to be acceptable given the potential reward here.

Relative Strength

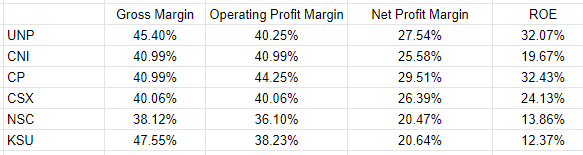

I think it makes sense to invest in companies that have outperformed their peers in the same industry. In particular, I want to invest in leaders who have a track record of outperforming peers when it comes to profitability, efficiency, and generating returns for shareholders. The following table shows that Union Pacific is either at the top of the heap or quite near it.

Source: Gurufocus

It could be said that Canadian Pacific gives Union Pacific a run for its money here, but I prefer the latter because it has far less “cold weather” track, and is thus less impacted by snowfall. Also, Union Pacific, unlike Canadian Pacific has direct access to both Mexico and the Gulf Coast.

Techncial Snapshot

As per my ChartMasterPro Daily Trading Model, there’s a high probability of a rally to the $195.00 level from here over the next two months for UNP, which would equate to a gain of around 6% for the shares.

- The shares drifted lower after the company released earnings on July 23, but found support at the $168.00 level and have since climbed to $182.00.

- Shares are currently right up against the Median Price Line, which often acts a resistance level – shares will most likely retrace from this level.

- Since timing is critical in options trading, I will wait for the next pullback to enter a LONG trade in the stock – ideally a pullback to the $172.00 would be a great entry point.

For investors who wish to buy the shares, I believe that waiting for a pullback to the $172.00 level would increase the profit on the trade over the next twelve months. For longer-term investors, I believe UNP is a solid addition to any dividend growth portfolio over the next 12 months.

Conclusion

Every time Union Pacific has stumbled in regards to earnings, the shares have dropped in price, but have quickly recovered. We’ve seen that dynamic play out yet again, and I think the shares will be heading higher from here. This is a standout relative to peers, and I think the dividend is well covered. That coverage should continue to offer support for the shares.

To view the option details (strike price, expiry date, and leverage), you can sign up for a Free Trial for The Options Trader. Only Members receive detailed trade alerts.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in UNP over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.