While so-called growth companies such as Microsoft (NASDAQ:MSFT) and Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL) have been clear winners in the current environment, it is easy to overlook under-the-radar value companies that have faced recent challenges exacerbated by the virus problem but can be long-term winners as they emerge stronger from those challenges.

I believe Greenbrier will be one of those:

Greenbrier

Greenbrier Companies (GBX) is one of the world’s largest freight rail carmakers with production facilities in Europe and South America as well as the US. With roads in much of Europe and the US overloaded well above their original design capacity and the jams adding to pollution, more and more freight will go onto trains. In Europe, inefficient rail systems in the past drove freight onto the road. Now, the reverse is happening – truck trailers are leaving the road to get from Germany to Latvia and elsewhere by rail.

Photo: railwaygazette.com

Additionally, many rail freight cars are decades old and are very slow and noisy. Greenbrier makes good money servicing those, and more will be made replacing them because that noise is becoming a political issue as new communities of voters grow near railways.

Slow rail traffic means less trains per hour can use existing railway lines, so that means faster freight cars will be needed. The monopoly railroad companies in the US – where 80% of trains using the rail are currently freight trains – are hindering change, but market opportunities and potential antitrust measures may stimulate them into providing space for more freight and passenger trains.

Passenger trains attract population growth, and many new apartment blocks are being built alongside railway lines.

And man being man, he knows before he moves in that there will be rail noise but then complains afterwards about… rail noise. Old freight trains are noisy, and many run at night.

We constantly talk about air and water pollution but not enough is made of noise pollution. Quieter rail freight cars are coming, and Greenbrier Europe makes those.

Photo: Greenbrier

Greenbrier also makes money:

Financial results

Greenbrier just announced this for its 3rd fiscal quarter ended May 31;

~ Operating cash flow exceeding $220 million ~

~ $1 billion liquidity target achieved ~

~ $2.7 billion backlog provides forward visibility ~

William A. Furman, Chairman & CEO commented on July 10, 2020:

“Greenbrier delivered strong operational results in the quarter while maintaining a constant focus on the safety and health of our employees through the pandemic and its related economic shocks. Third quarter performance reflects our near-term priorities of keeping our factories operating under essential industry status, significantly increasing liquidity and adjusting our capacity to align with our evolving demand expectations. Entering the fiscal fourth quarter Greenbrier’s cash position was $735.3 million. As we increased cash, our net debt decreased by over $190 million, the lowest level in four quarters. We have taken difficult measures required to achieve our liquidity and cost reduction targets. Greenbrier is exceptionally well-positioned to compete and succeed during this weaker period in the economy and our core markets.”

He has been a big buyer of shares according to this SEC filing.

Detailed financial information is here.

Dividend investors might also like the 4% dividend. That looks safe to me, given the healthy state of Greenbrier’s finances and payment history:

Next Dividend: 8/19/2020

Annual Dividend: $1.08

Dividend Yield: 4.00%

Dividend Growth: 21.95% (3 Year Average)

Payout Ratio(s): 37.63% (Trailing 12 Months of Earnings)

Track Record: 5 Years of Consecutive Dividend Growth

Most Recent Increase: $0.02 increase on 1/8/2020

Trinity (NYSE:TRN) is going in the other direction. Explaining the latest round of losses in the second quarter 2020 results release on July 22, 2020 – just 12 days after that positive Greenbrier statement – the CEO of Trinity, Jean Savage, said,

“Our businesses are facing challenging market dynamics resulting from the historic decline in railcar loadings and the resulting underutilized railcars in North America. Commercially, our primary focus is to maintain the utilization of our lease fleet, then to meet customer demand for newly manufactured railcars as appropriate. Our lease fleet utilization is holding around 95%, albeit with pricing pressure on lease rates, and our production capacity for 2020 railcar deliveries is essentially sold. The timeline for a recovery in the rail sector remains unclear as increasing COVID-19 cases in the U.S. potentially threaten the recent improvement in economic and rail market activity.”

That glosses over the fact that Trinity has an important customer base in the US frac sand sector that is in long-term decline, reflected in financially vulnerable customers and the bankruptcies of four of those.

The relative profitabilities show the story in numbers:

Greenbrier:

| Gross margin | 13.67% |

|---|---|

| Net profit margin | 4.16% |

| Operating margin | 7.28% |

| Return on assets | 4.41% |

|---|---|

| Return on equity | 6.59% |

| Return on investment | 5.76% |

Trinity:

| Gross margin | 21.02% |

|---|---|

| Net profit margin | -1.97% |

| Operating margin | -0.60% |

| Return on assets | -0.64% |

|---|---|

| Return on equity | 1.28% |

| Return on investment | -0.71% |

Number source: Financial Times

GBX outperforms on all except gross margins, and if it can gradually improve those without losing market share, it will continue to outperform because…

Greenbrier is the clear market leader.

I particularly like Greenbrier’s growing market share.

Greenbrier’s most recent presentation shows that product diversification and geographic expansion have grown Greenbrier’s new railcar manufacturing market by approximately 420%. The growth has been at the expense of Trinity and shows in the market share of backlog orders:

– In September 2006, GBX had 13% of those, others had 51%, and TRN had 36%

– In March 2020, GBX had 50%, others had 24%, and TRN had 26%

Market share gains are not easy to achieve and nor are losses easily regained!

It is also expanding in Europe where many moves to change freight from road to rail for pollution reasons are being supported by recession recovery infrastructure money from governments and the EU.

Greenbrier Europe offers high-end freight railcar manufacturing, innovative engineering, repairs and refurbishments and customer service. Greenbrier Europe also performs projects and customer needs from outside Europe, such as in the Gulf Cooperation Council nations or the Eurasia region.

Future growth opportunities

Modern industrial farming meant commodity crops needed long-distance flights to get them to markets while reasonably fresh. That also meant non-nutritious crops rather than those needed for a healthy diet that might help build immunity against diseases like COVID-19. Such airfreight adds more pollution. So, the trend today is back to small local farms close to consumers using old fashioned crop rotation techniques plus new age vertical farms such as this one.

Photo: aerofarms.com/Ten of those on a smaller scale will be built in and around Jersey City. Crops from vertical farms will travel from farm to our forks by road or short-haul rail.

– Reshoring and localisation of manufacturing is becoming the norm in Europe and the US, and new forms of old businesses will do more in close proximity with suppliers because it is more efficient in today’s digital and automated age. Much related freight will go from planes onto cleaner trains.

– Up to 2 million TEU could be moving by rail across the Eurasian land-bridge corridors by 2030, according to a study commissioned by the International Union of Railways. The study reports that market players are seeking to identify a range of ‘niche’ products that are particularly well suited to rail transport. This could include fresh fruit and vegetables as well as expensive bulk products that are sensitive to humidity.

– The U.S. Senate on March 26 passed H.R. 748, its version of a $2 trillion stimulus package to address the devastating economic and societal impacts of the COVID-19 pandemic. Called the “Coronavirus Aid, Relief and Economic Security (CARES) Act,” it includes many rail-related funding measures of direct benefit to the railway industry-all modes, freight and passenger.

– The EU Green Deal will prioritise trains generally with policy actions to be geared towards rail to ensure that low-emission transport options are supported over less environmentally-friendly modes.

– Other EU investments will put Euros 1.6 billion ($1.85 billion) into building more rail infrastructure around the EU. Photo: PKP PLK

– US House Democrats recently rolled out a nearly $500 billion green transportation infrastructure bill aimed at updating America’s ageing transportation system.

– A dislike of pipelines means more oil will be carried by rail in the US and US farmers will need more rail roads to be built to carry their crops as well

– Rail freight services between China and Europe are gaining a new head of steam and was up 48% YOY in May. That takes 18 days instead of 32 or more by sea and is 50% cheaper than air freight.

– As part of its strategic investments to support growing demand and enable supply chains, Canadian National Railway (CNI +1.0%) plans to invest ~C$445M across British Columbia in 2020. The company’s investments will create greater capacity, which supports reductions in its customer’s transportation supply chain GHG emissions, by encouraging the use of rail for long haul needs.

– In Nigeria, building the Lagos to Kano line is nearing completion to take freight off overcrowded roads and allow expansion of exports. Many African countries are rich in natural resources but poor in access to seaports to export those from.

Greenbrier Europe is well placed to compete for the orders for freight trains to operate on those emerging market rail lines

Opportunities such as those are being added to almost daily in most parts of the world. Greenbrier is active in many of those, and thus;

Greenbrier is a value and growth stock

I have used Trinity to show that Greenbrier is head and shoulders above the best of the rest. There is more that makes no sense to me:

– Trinity’s market capitalisation is $2.3 billion, and the PE was around 150 before it finally headed into losses in the past quarter following several years of decline. That is even higher than Amazon’s (NASDAQ:AMZN) PE of 146!

– Greenbrier’s market cap is only $872 million with a PE of 10.8. A true value stock!

– I mentioned growth stocks Alphabet and Microsoft in my opening paragraph; Alphabet has a PE of 31. Microsoft’s PE is 35.

I doubt that Greenbrier will ever get the profile or achieve the size of those tech giants, but its market-leading position in its sector and the growth of that sector – that has started to happen and will continue for years due to huge investments in environmental and recession recovery – means that its current stock price is far too low.

Trinity is responding to its problems with organisational change, but that is no substitute for proper leadership. It has a mountain of debt, giving it a debt to equity ratio of 2.55 compared with Greenbrier’s 0.9475. Trinity’s CEO recently said,

“it has already reduced its manufacturing workforce by 35% since the start of the year, resulting in almost $40 million in overhead cost savings. Other workforce rationalisations among Trinity’s higher-cost footprint could also occur”.

Now, in cost cutting survival mode, Trinity will not be investing in product and market development, meaning its market share will shrink further, and Greenbrier’s could grow more. Trinity’s problems are Greenbrier’s opportunities; the strong get stronger, the weak weaker! Recessions are the easiest time to grow market share and that increased share stays when economies are back in growth mode.

That means stock price growth for investors if they…

Buy GBX now

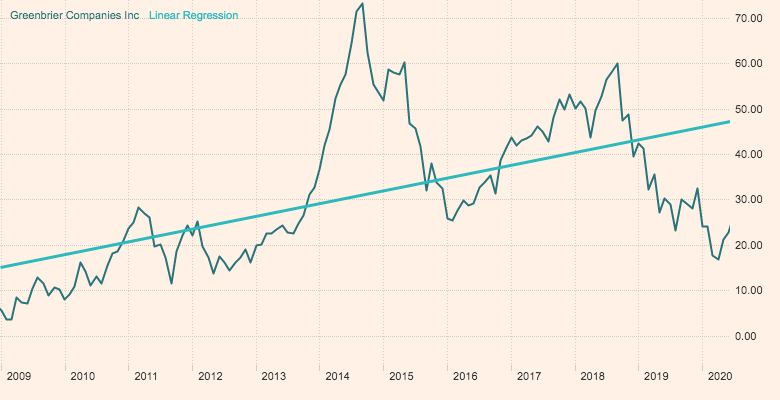

On Sept. 1, 2014, the stock price of GBX hit an all-time high of $78. On Sept. 18, 2018, it was $60.75. Currently, it is around $27. This Financial Times Linear Regression chart suggests it should be at $48 now.

I see no reason why it should not get back to that 2018 price soon, and 7-year cycles could put it back to $78 by September 2021. Exploitation of the many opportunities could put it much higher longer term.

Disclosure: I am/we are long GBX. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}