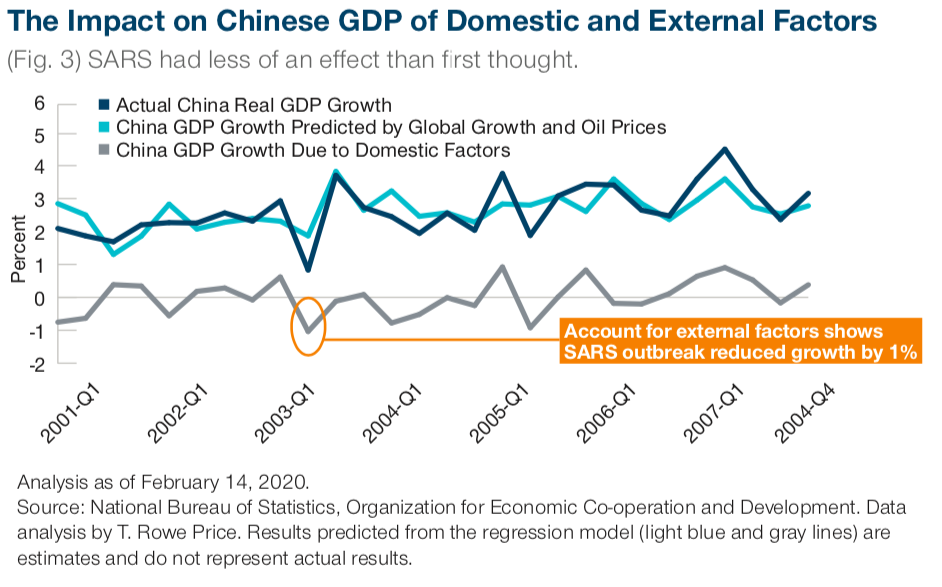

Overall, the coincidental global slowdown and rise in real oil prices mean that the effect of SARS was likely greatly exaggerated in Chinese GDP data. In our view, SARS is, therefore, not a good case study for understanding the potential economic consequences of COVID‐19 on Chinese real GDP growth.

If SARS is not a good case study to assess the economic impact of COVID‐19, what should investors look at instead? We believe that the most useful approach is to quantify the effect of lost working days on overall production. We estimate that the current measures imposed by the Chinese government through early February have led to eight lost working days for the country as whole. A reduction in one working day in Q1 leads to roughly a 0.4% loss in output, meaning that the eight lost working days so far translate into a quarterly growth reduction of 3.2%. This number is 50% larger than 2.1% growth impact measured during the SARS outbreak, and three times as large as the estimated 1% impact adjusted for external factors. Although this number could rise further, it is significantly smaller than extrapolating the economic impact based on virus cases in China, which, with 78,000 cases to date, is 15 times larger than the 5,237 cases that China experienced during SARS.

We believe that by looking at the sensitivity of growth to each working day lost (0.4% of GDP), we can get a much better sense of the economic impact of COVID‐19 than can be obtained from arbitrarily scaling up the consequences of SARS. The same method can be applied to the impact of COVID‐19 on growth in other countries that have been badly hit by the virus, including Italy.

{kind=link}